Search the Community

Showing results for tags 'straddle'.

Found 16 results

-

Well, every trade should be put in context. Before evaluating a trade (or an options strategy), the following questions should be asked and answered: What is the holding period of the strategy? What is the maximum risk? What is the profit potential? What is the average return? What is the winning ratio? Why holding period is important? Well, making 5% in one week is not the same as making 5% in six months. In the first case we are talking about 250% annualized return. In the second case, 10%. See the difference. Maximum risk is important because it doesn't make sense to aim for 5% gain if your strategy can lose 50-100%. For example, when you are trading a directional strategy, and the stock gaps against you, the losses can be catastrophic. Since the risk is high, you should aim for higher return to compensate for the risk. However, if your maximum risk is limited, you can aim for lower return and still get excellent overall performance. Lets examine our pre-earnings straddles as an example. As a reminder, a long straddle option strategy is vega positive, gamma positive and theta negative trade. It works based on the premise that both call and put options have unlimited profit potential but limited loss. Straddles are a good strategy to pursue if you believe that a stock's price will move significantly, but unsure as to which direction. Another case is if you believe that Implied Volatility of the options will increase - for example, before a significant event like earnings. I explained the latter strategy in my Seeking Alpha article Exploiting Earnings Associated Rising Volatility. IV usually increases sharply a few days before earnings, and the increase should compensate for the negative theta. If the stock moves before earnings, the position can be sold for a profit or rolled to new strikes. This is one of my favorite strategies that we use in our SteadyOptions model portfolio. This is how the P/L chart looks like: How We Trade Straddle Option Strategy provides a full explanation of the strategy. Lets take a look at 2022 statistics for this strategy: Number of trades: 148 Number of winners: 103 Number of losers: 40 Winning ratio: 72.5% Average return per trade: 4.9% Average return per winning trade: 8.7% Average return per losing trade: -10.2% Average holding period: 7.2 days Lets do a quick math. If you can do 10 trades per month, each trade producing 5% gain on average and 10% allocation per trade, your monthly return is 5% on the whole portfolio. That's 60% non compounded annual return, with minimal risk. To answer the original question: for a strategy that has 70%+ winning ratio and loses on average 10% on losing trades, with average holding period of one week, 5% is an EXCELLENT return. In fact, I would consider it as Close to the Holy Grail as You Can Get. Related Articles: How We Trade Straddle Option Strategy Buying Premium Prior to Earnings Can We Profit From Volatility Expansion into Earnings Long Straddle: A Guaranteed Win? Why We Sell Our Straddles Before Earnings

Well, every trade should be put in context. Before evaluating a trade (or an options strategy), the following questions should be asked and answered: What is the holding period of the strategy? What is the maximum risk? What is the profit potential? What is the average return? What is the winning ratio? Why holding period is important? Well, making 5% in one week is not the same as making 5% in six months. In the first case we are talking about 250% annualized return. In the second case, 10%. See the difference. Maximum risk is important because it doesn't make sense to aim for 5% gain if your strategy can lose 50-100%. For example, when you are trading a directional strategy, and the stock gaps against you, the losses can be catastrophic. Since the risk is high, you should aim for higher return to compensate for the risk. However, if your maximum risk is limited, you can aim for lower return and still get excellent overall performance. Lets examine our pre-earnings straddles as an example. As a reminder, a long straddle option strategy is vega positive, gamma positive and theta negative trade. It works based on the premise that both call and put options have unlimited profit potential but limited loss. Straddles are a good strategy to pursue if you believe that a stock's price will move significantly, but unsure as to which direction. Another case is if you believe that Implied Volatility of the options will increase - for example, before a significant event like earnings. I explained the latter strategy in my Seeking Alpha article Exploiting Earnings Associated Rising Volatility. IV usually increases sharply a few days before earnings, and the increase should compensate for the negative theta. If the stock moves before earnings, the position can be sold for a profit or rolled to new strikes. This is one of my favorite strategies that we use in our SteadyOptions model portfolio. This is how the P/L chart looks like: How We Trade Straddle Option Strategy provides a full explanation of the strategy. Lets take a look at 2022 statistics for this strategy: Number of trades: 148 Number of winners: 103 Number of losers: 40 Winning ratio: 72.5% Average return per trade: 4.9% Average return per winning trade: 8.7% Average return per losing trade: -10.2% Average holding period: 7.2 days Lets do a quick math. If you can do 10 trades per month, each trade producing 5% gain on average and 10% allocation per trade, your monthly return is 5% on the whole portfolio. That's 60% non compounded annual return, with minimal risk. To answer the original question: for a strategy that has 70%+ winning ratio and loses on average 10% on losing trades, with average holding period of one week, 5% is an EXCELLENT return. In fact, I would consider it as Close to the Holy Grail as You Can Get. Related Articles: How We Trade Straddle Option Strategy Buying Premium Prior to Earnings Can We Profit From Volatility Expansion into Earnings Long Straddle: A Guaranteed Win? Why We Sell Our Straddles Before Earnings -

Earnings Straddles: the Ultimate Protection Our followers already know that buying pre-earnings straddlesis one of our key strategies. I described it here. The idea is to buy a straddle (or a strangle) few days before earnings and sell just before the event. IV (Implied Volatility) usually increases sharply a few days before earnings, and the increase should compensate for the negative theta. If the stock moves before earnings, the position can be sold for a profit or rolled to new strikes. While we use this strategy on a regular basis, it is not among our most profitable strategies. During periods of low volatility, it usually produces 3-5% return per trade (including the losers). To put things in perspective, even 3% return is not that bad. The average holding period of those trades is around 5 days, so 3% return translates to 219% annual return. If you traded 40 straddles per year and allocated 10% per trade, those trades alone would contribute 12% to your account. Considering the low risk (the straddles rarely lose more than 7-10%), this is a pretty good return. But this is where it really gets interesting: I consider those trades a cheap black swan protection. If IV goes up sharply followed by the stock movement, this is where the strategy really shines. It can provide a really good protection to your options portfolio in case of sharp moves. Examples Lets take a look on few real life examples of trades that benefited from market volatility. Entered HPQ strangle on August 3, 2011, exited on August 8, 2011 for 109.7% gain. Entered DIS strangle on August 3, 2011, exited on August 8, 2011 for 107.1% gain. Entered CRM strangle on August 3, 2011, exited on August 8, 2011 for 101.7% gain. Entered AKAM straddle on July 23, 2012, exited on July 26, 2012 for 38.9% gain. Entered FNSR straddle on March 6, 2013, exited on March 7, 2013 for 24.2% gain. Entered MSFT straddle on June 24, 2014, exited on July 17, 2012 for 35.4% gain. Entered QIHU straddle on August 19, 2015, exited on August 19, 2015 for 22.9% gain. To be clear, the returns from 2011 can probably happen once in a few years when the markets really crash. But if you happen to hold few straddles or strangles during those periods, you will be very happy you did. Summary To be successful with this strategy, you need to know what you are doing. Not every stock works equally well. There are many moving parts to this strategy: When to enter? Which stocks to use? How to manage the position? When to take profits? If used properly, the pre-earnings straddles can provide decent gains during periods of low to medium volatility. But at the same time, they can provide excellent black swan protection. Are you familiar with another way to get black swan protection that costs you nothing - in fact, it even produces some gains? I'm not. Related Articles: How We Trade Straddle Option Strategy Buying Premium Prior to Earnings Can We Profit From Volatility Expansion into Earnings Want to learn more? Join SteadyOptions Now!

Earnings Straddles: the Ultimate Protection Our followers already know that buying pre-earnings straddlesis one of our key strategies. I described it here. The idea is to buy a straddle (or a strangle) few days before earnings and sell just before the event. IV (Implied Volatility) usually increases sharply a few days before earnings, and the increase should compensate for the negative theta. If the stock moves before earnings, the position can be sold for a profit or rolled to new strikes. While we use this strategy on a regular basis, it is not among our most profitable strategies. During periods of low volatility, it usually produces 3-5% return per trade (including the losers). To put things in perspective, even 3% return is not that bad. The average holding period of those trades is around 5 days, so 3% return translates to 219% annual return. If you traded 40 straddles per year and allocated 10% per trade, those trades alone would contribute 12% to your account. Considering the low risk (the straddles rarely lose more than 7-10%), this is a pretty good return. But this is where it really gets interesting: I consider those trades a cheap black swan protection. If IV goes up sharply followed by the stock movement, this is where the strategy really shines. It can provide a really good protection to your options portfolio in case of sharp moves. Examples Lets take a look on few real life examples of trades that benefited from market volatility. Entered HPQ strangle on August 3, 2011, exited on August 8, 2011 for 109.7% gain. Entered DIS strangle on August 3, 2011, exited on August 8, 2011 for 107.1% gain. Entered CRM strangle on August 3, 2011, exited on August 8, 2011 for 101.7% gain. Entered AKAM straddle on July 23, 2012, exited on July 26, 2012 for 38.9% gain. Entered FNSR straddle on March 6, 2013, exited on March 7, 2013 for 24.2% gain. Entered MSFT straddle on June 24, 2014, exited on July 17, 2012 for 35.4% gain. Entered QIHU straddle on August 19, 2015, exited on August 19, 2015 for 22.9% gain. To be clear, the returns from 2011 can probably happen once in a few years when the markets really crash. But if you happen to hold few straddles or strangles during those periods, you will be very happy you did. Summary To be successful with this strategy, you need to know what you are doing. Not every stock works equally well. There are many moving parts to this strategy: When to enter? Which stocks to use? How to manage the position? When to take profits? If used properly, the pre-earnings straddles can provide decent gains during periods of low to medium volatility. But at the same time, they can provide excellent black swan protection. Are you familiar with another way to get black swan protection that costs you nothing - in fact, it even produces some gains? I'm not. Related Articles: How We Trade Straddle Option Strategy Buying Premium Prior to Earnings Can We Profit From Volatility Expansion into Earnings Want to learn more? Join SteadyOptions Now! -

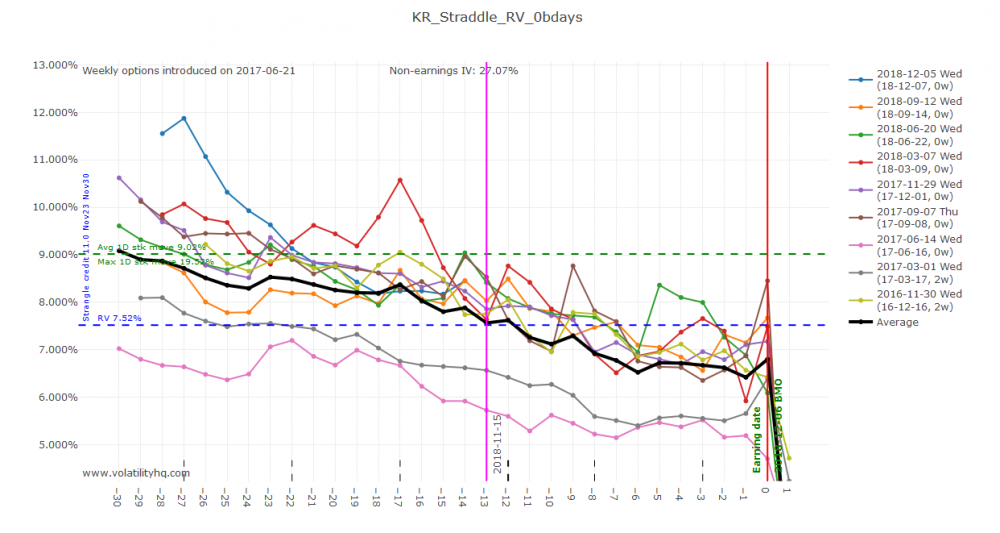

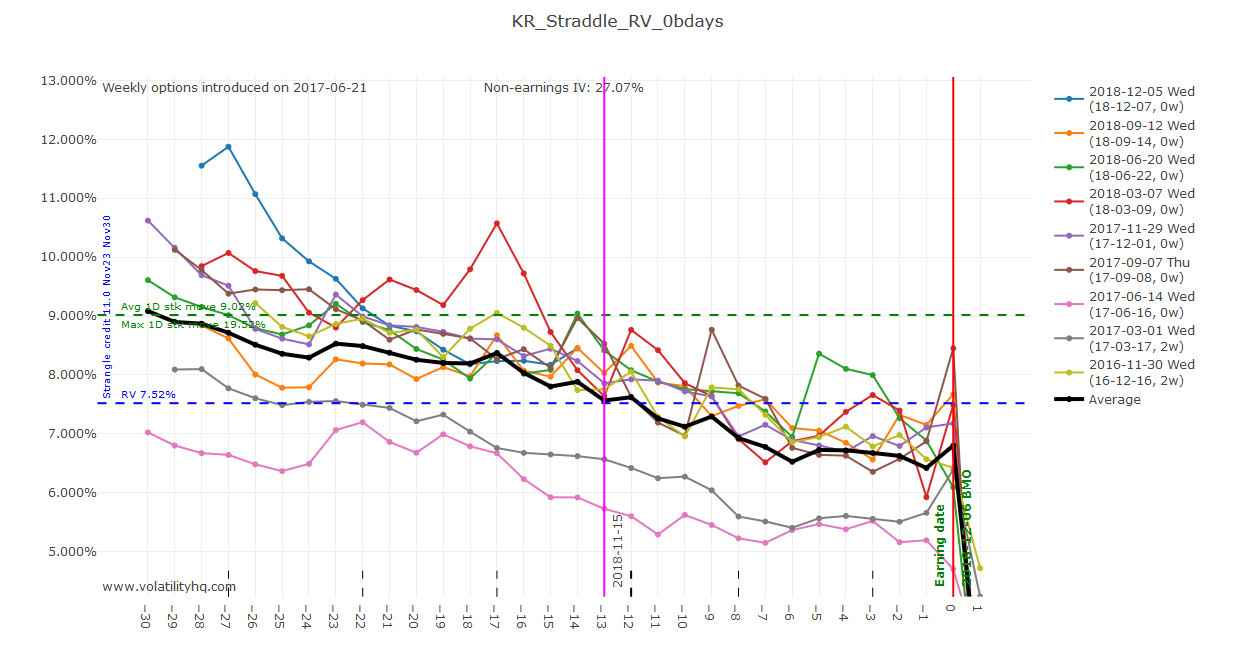

.jpg.222373e1d6ea0229244884bdd821d779.jpg) About six months ago, I came across an excellent book by Jeff Augen, “The Volatility Edge in Options Trading”. One of the strategies described in the book is called “Exploiting Earnings - Associated Rising Volatility”. Here is how it works: Find a stock with a history of big post-earnings moves. Buy a strangle for this stock about 7-14 days before earnings. Sell just before the earnings are announced. For those not familiar with the strangle strategy, it involves buying calls and puts on the same stock with different strikes. If you want the trade to be neutral and not directional, you structure the trade in a way that calls and puts are the same distance from the underlying price. For example, with Amazon (NASDAQ:AMZN) trading at $190, you could buy $200 calls and $180 puts. IV (Implied Volatility) usually increases sharply a few days before earnings, and the increase should compensate for the negative theta. If the stock moves before earnings, the position can be sold for a profit or rolled to new strikes. Like every strategy, the devil is in details. The following questions need to be answered: Which stocks should be used? I tend to trade stocks with post-earnings moves of at least 5-7% in the last four earnings cycles; the larger the move the better. When to buy? IV starts to rise as early as three weeks before earnings for some stocks and just a few days before earnings for others. Buy too early and negative theta will kill the trade. Buy too late and you might miss the big portion of the IV increase. I found that 5-7 days usually works the best. Which strikes to buy? If you go far OTM (Out of The Money), you get big gains if the stock moves before earnings. But if the stock doesn’t move, closer to the money strikes might be a better choice. Since I don’t know in advance if the stock will move, I found deltas in the 20-30 range to be a good compromise. The selection of the stocks is very important to the success of the strategy. The following simple steps will help with the selection: Click here. Filter stocks with movement greater than 5% in the last 3 earnings. For each stock in the list, check if the options are liquid enough. Using those simple steps, I compiled a list of almost 100 stocks which fit the criteria. Apple (NASDAQ:AAPL), Google (NASDAQ:GOOG), Netflix (NASDAQ:NFLX), F5 Networks (NASDAQ:FFIV), Priceline (PCLN), Amazon (AMZN), First Solar (NASDAQ:FSLR), Green Mountain Coffee Roasters (NASDAQ:GMCR), Akamai Technologies (NASDAQ:AKAM), Intuitive Surgical (NASDAQ:ISRG), Saleforce (NYSE:CRM), Wynn Resorts (NASDAQ:WYNN), Baidu (NASDAQ:BIDU) are among the best candidates for this strategy. Those stocks usually experience the largest pre-earnings IV spikes. So I started using this strategy in July. The results so far are promising. Average gains have been around 10-12% per trade, with an average holding period of 5-7 days. That might not sound like much, but consider this: you can make about 20 such trades per month. If you allocate just 5% per trade, you earn 20*10%*0.05=10% return per month on the whole account while risking only 25-30% (5-6 trades open at any given time). Does it look better now? Under normal conditions, a strangle trade requires a big and quick move in the underlying. If the move doesn’t happen, the negative theta will kill the trade. In case of the pre-earnings strangle, the negative theta is neutralized, at least partially, by increasing IV. In some cases, the theta is larger than the IV increase and the trade is a loser. However, the losses in most cases are relatively small. Typical loss is around 10-15%, in some rare cases it might reach 25-30%. But the winners far outpace the losers and the strategy is overall profitable. Market environment also plays a role in the strategy performance. The strategy performs the best in a volatile environment when stocks move a lot. If none of the stocks move, most of the trades would be around breakeven or small losers. Fortunately, over time, stocks do move. In fact, big chunk of the gains come from stock movement and not IV increases. The IV increase just helps the trade not to lose in case the stock doesn’t move. In the next article I will explain why, in my opinion, it usually doesn’t pay to hold through earnings. We always close those trade before earnings to avoid IV crush. The original article was published here.

About six months ago, I came across an excellent book by Jeff Augen, “The Volatility Edge in Options Trading”. One of the strategies described in the book is called “Exploiting Earnings - Associated Rising Volatility”. Here is how it works: Find a stock with a history of big post-earnings moves. Buy a strangle for this stock about 7-14 days before earnings. Sell just before the earnings are announced. For those not familiar with the strangle strategy, it involves buying calls and puts on the same stock with different strikes. If you want the trade to be neutral and not directional, you structure the trade in a way that calls and puts are the same distance from the underlying price. For example, with Amazon (NASDAQ:AMZN) trading at $190, you could buy $200 calls and $180 puts. IV (Implied Volatility) usually increases sharply a few days before earnings, and the increase should compensate for the negative theta. If the stock moves before earnings, the position can be sold for a profit or rolled to new strikes. Like every strategy, the devil is in details. The following questions need to be answered: Which stocks should be used? I tend to trade stocks with post-earnings moves of at least 5-7% in the last four earnings cycles; the larger the move the better. When to buy? IV starts to rise as early as three weeks before earnings for some stocks and just a few days before earnings for others. Buy too early and negative theta will kill the trade. Buy too late and you might miss the big portion of the IV increase. I found that 5-7 days usually works the best. Which strikes to buy? If you go far OTM (Out of The Money), you get big gains if the stock moves before earnings. But if the stock doesn’t move, closer to the money strikes might be a better choice. Since I don’t know in advance if the stock will move, I found deltas in the 20-30 range to be a good compromise. The selection of the stocks is very important to the success of the strategy. The following simple steps will help with the selection: Click here. Filter stocks with movement greater than 5% in the last 3 earnings. For each stock in the list, check if the options are liquid enough. Using those simple steps, I compiled a list of almost 100 stocks which fit the criteria. Apple (NASDAQ:AAPL), Google (NASDAQ:GOOG), Netflix (NASDAQ:NFLX), F5 Networks (NASDAQ:FFIV), Priceline (PCLN), Amazon (AMZN), First Solar (NASDAQ:FSLR), Green Mountain Coffee Roasters (NASDAQ:GMCR), Akamai Technologies (NASDAQ:AKAM), Intuitive Surgical (NASDAQ:ISRG), Saleforce (NYSE:CRM), Wynn Resorts (NASDAQ:WYNN), Baidu (NASDAQ:BIDU) are among the best candidates for this strategy. Those stocks usually experience the largest pre-earnings IV spikes. So I started using this strategy in July. The results so far are promising. Average gains have been around 10-12% per trade, with an average holding period of 5-7 days. That might not sound like much, but consider this: you can make about 20 such trades per month. If you allocate just 5% per trade, you earn 20*10%*0.05=10% return per month on the whole account while risking only 25-30% (5-6 trades open at any given time). Does it look better now? Under normal conditions, a strangle trade requires a big and quick move in the underlying. If the move doesn’t happen, the negative theta will kill the trade. In case of the pre-earnings strangle, the negative theta is neutralized, at least partially, by increasing IV. In some cases, the theta is larger than the IV increase and the trade is a loser. However, the losses in most cases are relatively small. Typical loss is around 10-15%, in some rare cases it might reach 25-30%. But the winners far outpace the losers and the strategy is overall profitable. Market environment also plays a role in the strategy performance. The strategy performs the best in a volatile environment when stocks move a lot. If none of the stocks move, most of the trades would be around breakeven or small losers. Fortunately, over time, stocks do move. In fact, big chunk of the gains come from stock movement and not IV increases. The IV increase just helps the trade not to lose in case the stock doesn’t move. In the next article I will explain why, in my opinion, it usually doesn’t pay to hold through earnings. We always close those trade before earnings to avoid IV crush. The original article was published here. -

Here is how their methodology works: In theory, if you knew exactly what price a stock would be immediately before earnings, you could purchase the corresponding straddle a number of days beforehand. To test this, we looked at the past 4 earnings cycles in 5 different stocks. We recorded the closing price of each stock immediately before the earnings announcement. We then went back 14 days and purchased the straddle using the strikes recorded on the close prior to earnings. We closed those positions immediately before earnings were to be reported. Study Parameters: TSLA, LNKD, NFLX, AAPL, GOOG Past 4 earnings cycles 14 days prior to earnings - purchased future ATM straddle Sold positions on the close before earnings The results: Future ATM straddle produced average ROC of -19%. As an example: In the previous cycle, TSLA was trading around $219 two weeks before earnings. The stock closed around $201 a day before earnings. According to tastytrade methodology, they would buy the 200 straddle 2 weeks before earnings. They claim that this is the best case scenario for buying pre-earnings straddles. My Rebuttal Wait a minute.. This is a straddle, not a calendar. For a calendar, the stock has to trade as close to the strike as possible to realize the maximum gain. For a straddle, it's exactly the opposite: When you buy a straddle, you want the stock to move away from your strike, not towards the strike. You LOSE the maximum amount of money if the stock moves to the strike. In case of TSLA, if you wanted to trade pre-earnings straddle 2 weeks before earnings when the stock was at $219, you would purchase the 220 straddle, not 200 straddle. If you do that, you start delta neutral and have some gamma gains when the stock moves to $200. But if you start with 200 straddle, your initial setup is delta positive, while you know that the stock will move against you. It still does not guarantee that the straddle will be profitable. You need to select the best timing (usually 5-7 days, not 14 days) and select the stocks carefully (some stocks are better candidates than others). But using tastytrade methodology would GUARANTEE that the strategy will lose money 90% of the time. It almost feels like they deliberately used those parameters to reach the conclusion they wanted. As a side note, the five stocks they selected for the study are among the worst possible candidates for this strategy. It almost feels like they selected the worst possible parameters in terms of strike, timing and stocks, in order to reach the conclusion they wanted to reach. At SteadyOptions, buying pre-earnings straddles is one of our key strategies. It works very well for us. Check out our performance page for full results. As you can see from our results, "Buying Premium Prior To Earnings" is still alive and kicking. Not exactly "Nail In The Coffin". Comment: the segment has been removed from tastytrade website, which shows that they realized how absurd it was. We linked to the YouTube video which is still there. Of course the devil is in the details. There are many moving parts to this strategy: When to enter? Which stocks to use? How to manage the position? When to take profits? And much more. But overall, this strategy has been working very well for us. If you want to learn more how to use it (and many other profitable strategies): Subscribe to SteadyOptions now and experience the full power of options trading at your fingertips. Click the button below to get started! Join SteadyOptions Now! Related Articles: How We Trade Straddle Option Strategy Can We Profit From Volatility Expansion into Earnings Long Straddle: A Guaranteed Win? Why We Sell Our Straddles Before Earnings Long Straddle: A Guaranteed Win? How We Made 23% On QIHU Straddle In 4 Hours

Here is how their methodology works: In theory, if you knew exactly what price a stock would be immediately before earnings, you could purchase the corresponding straddle a number of days beforehand. To test this, we looked at the past 4 earnings cycles in 5 different stocks. We recorded the closing price of each stock immediately before the earnings announcement. We then went back 14 days and purchased the straddle using the strikes recorded on the close prior to earnings. We closed those positions immediately before earnings were to be reported. Study Parameters: TSLA, LNKD, NFLX, AAPL, GOOG Past 4 earnings cycles 14 days prior to earnings - purchased future ATM straddle Sold positions on the close before earnings The results: Future ATM straddle produced average ROC of -19%. As an example: In the previous cycle, TSLA was trading around $219 two weeks before earnings. The stock closed around $201 a day before earnings. According to tastytrade methodology, they would buy the 200 straddle 2 weeks before earnings. They claim that this is the best case scenario for buying pre-earnings straddles. My Rebuttal Wait a minute.. This is a straddle, not a calendar. For a calendar, the stock has to trade as close to the strike as possible to realize the maximum gain. For a straddle, it's exactly the opposite: When you buy a straddle, you want the stock to move away from your strike, not towards the strike. You LOSE the maximum amount of money if the stock moves to the strike. In case of TSLA, if you wanted to trade pre-earnings straddle 2 weeks before earnings when the stock was at $219, you would purchase the 220 straddle, not 200 straddle. If you do that, you start delta neutral and have some gamma gains when the stock moves to $200. But if you start with 200 straddle, your initial setup is delta positive, while you know that the stock will move against you. It still does not guarantee that the straddle will be profitable. You need to select the best timing (usually 5-7 days, not 14 days) and select the stocks carefully (some stocks are better candidates than others). But using tastytrade methodology would GUARANTEE that the strategy will lose money 90% of the time. It almost feels like they deliberately used those parameters to reach the conclusion they wanted. As a side note, the five stocks they selected for the study are among the worst possible candidates for this strategy. It almost feels like they selected the worst possible parameters in terms of strike, timing and stocks, in order to reach the conclusion they wanted to reach. At SteadyOptions, buying pre-earnings straddles is one of our key strategies. It works very well for us. Check out our performance page for full results. As you can see from our results, "Buying Premium Prior To Earnings" is still alive and kicking. Not exactly "Nail In The Coffin". Comment: the segment has been removed from tastytrade website, which shows that they realized how absurd it was. We linked to the YouTube video which is still there. Of course the devil is in the details. There are many moving parts to this strategy: When to enter? Which stocks to use? How to manage the position? When to take profits? And much more. But overall, this strategy has been working very well for us. If you want to learn more how to use it (and many other profitable strategies): Subscribe to SteadyOptions now and experience the full power of options trading at your fingertips. Click the button below to get started! Join SteadyOptions Now! Related Articles: How We Trade Straddle Option Strategy Can We Profit From Volatility Expansion into Earnings Long Straddle: A Guaranteed Win? Why We Sell Our Straddles Before Earnings Long Straddle: A Guaranteed Win? How We Made 23% On QIHU Straddle In 4 Hours -

This dynamic nature of options allows you to craft a position to fit your exact market view. Perhaps there’s a big Federal Reserve meeting coming up and you expect the market to overreact, but you don’t have a specific view as to which direction. In this case, you can use a market-neutral option spread like a straddle or strangle. In the same vein, if the financial media and traders are making a big stink about something you deem a nothingburger, you can use strangles or straddles to take the view that the market will underreact to the news compared to what the market pricing expects. Strangles and straddles are market-neutral options spreads which are apathetic to the direction that price moves. They instead allow a trader to express a view on the magnitude of the price move, regardless if the price moves up or down. Let’s paint a quick hypothetical for demonstration. There’s a Federal Reserve meeting in a week. There’s tons of talk about the possibility of a Fed pivot and the dramatic implications that’d have for the global economy. Looking at the S&P 500 options for that expiration, you see that the implied volatility is very high compared to past Fed meetings. Traders are expecting the Fed to drop a surprise in some sense. Based on your own macro view, you’re unconvinced. You believe the Fed will continue their campaign of modest hikes of rates through the first half the year. In other words, you expect business as usual while the market expects radical change. As an options trader, you’re fully aware that change equals volatility and the lack of change leads volatility to contract, making most options expire worthless. You decide to sell a straddle, which involves selling an at-the-money put and an at-the-money call simultaneously. Should your view pan out, you’ll be able to pocket a good portion of the premium you collected when you opened the trade. What Is a Strangle? A strangle is market-neutral options spread that involves the simultaneous purchase or sale of an out-of-the-money call and an out-of-the-money put. So if the underlying is trading at $20.00, you might buy the $18 strike put and the $22 strike call. In this case, you’re hoping for a large price move in either direction, as your break-even price is often pretty far from the current underlying price. Let’s look at a brief example of a long strangle in $SPY using a .30 delta put and call with 27 days to expiration. Here’s the options we’re buying: ● SPY (underlying) price: 396.00 ● 1 386 FEB 27 PUT @ 4.31 (-0.30 delta) ● 1 407 FEB 27 CALL @ 3.54 (0.30 delta) ● Cost of Position: 7.85 Here’s the payoff diagram of this position: Once the position gets outside of the shaded gray area, the position is in-the-money. To provide some context to this position, SPY must move up or down roughly 4.5% for your position to be in-the-money. Let’s look at the same trade but from the short side: The details of this trade are a mirror opposite of the previous example. You’d collect a $7.85 credit, and your break-even levels are outside of the shaded gray area. You’d make this trade if you expect SPY to remain within that range through expiration (27 days). Strangle Strike Selection Strike selection is a significant factor here and there’s no correct answer really. The lower delta options you choose, the cheaper the spread and the lower the probability of profit will be. Perhaps you have a very specific market view, making strike selection obvious. But in most cases, novice option traders choose arbitrary strikes, which is a mistake. Strike selection is one of the most important aspects of trade structuring. An easy way to start being more thoughtful about selecting strikes is to view an option’s delta as a rough approximation of the probability of expiring in-the-money. This simple trick provides a lot of context to option pricing. You’ll see at-the-money options often hover around .50 delta, because the market basically has a 50/50 chance of going up or down over any time period not measured in years. As you get further from the money, deltas go down, which also makes intuitive sense. Using this framework, you can look at a .20 delta strangle and think “the market thinks there’s a 20% chance of either of these options expiring in-the-money. Is my probability forecast higher or lower than that? If you can answer this question, your strike selection becomes not only easier, but far more thoughtful. What is a Straddle? A straddle is a market-neutral options spread involving the simultaneous purchase (or sale) of a call and put at the same strike price and expiration. The goal of the trade is to make a bet on volatility in a market-neutral fashion. While any trade trade involving buying or selling a put and a call at the same strike price and expiration is technically a straddle, the majority of the time when we talk about straddles, we’re talking about an at-the-money straddle, meaning you buy a put and call at the ATM strike. In other words, if implied volatility is 20%, but you expect future realized volatility to be much higher than that, buying a straddle would provide a profit regardless of which direction the market goes, or how it arrives there. Along similar lines, if you expect realized volatility to be far less than 20%, you can short a straddle to profit from the market’s overestimation of volatility. In a word, you want to buy a long straddle when you think options are too cheap, and short straddles or short strangles when options seem too expensive. Here’s an example of a long straddle in SPY with 27 days to expiration. With SPY trading at 396 at the time of writing, we’d want to buy the 396 call and puts. Here’s how that’d look: ● SPY (underlying) at 396.00 ● 1 396 FEB 27 CALL @ 8.59 ● 1 396 FEB 27 CALL @ 7.69 ● Total cost of trade: $16.28 As you can see, this ATM straddle costs more than double what our 0.30 delta strangle costs us. Being wrong on straddles is far more painful. But this payoff diagram shows us the upside to this trade-off: What is most interesting here is that our 0.30 delta strangle from the previous example has nearly identical break-even points to this ATM straddle: around 379 and 414. However, looking at the shape of the P&L, you can see that you only experience your max P&L loss if the market goes absolutely nowhere and is still at 396 at expiration. If the market moves even modestly in either direction, your trade begins to move in your favor. This is in stark contrast to our strangle, in which we experience maximum loss at a far wider range of prices. So while you do have to shell out more premium to establish a straddle, it’s quite unlikely you’ll actually lose all of your premium. The Similarities Between a Strangle and a Straddle Both are Defined-Risk Options Spreads Both the straddle and strangle involve buying two different options without selling any options to offset the premium paid. So the most you can lose in either a straddle or strangle is the premium you paid. A defining trait of many defined-risk, long options strategies is the convexity afforded to you; you know the maximum you can lose is X, but your upside is theoretically unlimited. This can of course lead to occasional massive wins where the market basically trends in your direction until expiration. Both Are Market-Neutral Options allow you to express a more diverse array of market views than simply long or short. One of those is the ability to profit without having to predict the direction of price. While market-neutral is an easy term to use because most understand it off the bat, that’s not entirely correct. You can more accurately call straddles or strangles delta neutral strategy because while you’re neutral on the direction of price, you’re still ultimately taking some sort of market view. In the case of straddles and strangles, you’re taking a view on whether volatility will expand or contract. Or in other words, do you have conviction on whether the market will move more or less than the option market thinks? If so, you can profit from this view. Put simply, if you expect the underlying to get more volatile before expiration, you want to be long volatility. Taking a long volatility view assumes that the options market’s implied volatility forecast is too low, making options too cheap. Expressing a long volatility view in the context of a straddle or strangle means taking the long side of the trade (buying the options instead of shorting them). Just as we described in the intro of this article, if you hold the view that the market is overhyping the significance of a catalyst, you make the same trade in reverse; you can short an at-the-money put and an ATM call, which is a short straddle. If realized volatility is lower than implied volatility, then you’ll end up pocketing a good portion of premium when you close the trade. The Differences Between a Strangle and a Straddle Straddles and strangles express very similar views; traders using them are either expressing a long or short volatility while remaining agnostic on price direction. Where they differ is the magnitude of their view, or how wrong they think the market pricing of implied volatility is. From the long-volatility perspective, it’s cheaper to buy a strangle because you’re buying OTM options but the dilemma is that with cheaper OTM options, you have a lower probability of profiting from the trade. The market needs to move more to put you in the money. If you flip this dilemma to the short side, you have the same problem. When shorting strangles, you have a high probability of collecting the entire premium at the conclusion of the trade, but when the market does make a big move, you experience a huge loss. So you can rack up several wins in a row only to see one loss knock out all of these gains. ATM Straddles Have More Premium Than Strangles At-the-money options have more premium than OTM options. So it follows that the straddle, a spread with two ATM options, would have far more premium than one with two OTM options, the strangle. For this reason, systematic sellers of premium, what you might call the “Tastytrade crowd,” really like straddles for their high premium properties. This property of higher premium doesn’t make the straddle superior for premium sellers, as there’s no free lunch--premium sellers are paying for this higher level of premium with a lower win rate on their trades. Straddles Have a Higher Probability of Profit As it might’ve become clear throughout this article, constructing options spreads is all about tradeoffs. Want to put out a small amount of capital with the possibility of a huge win? You can do that, but you’ll hit on those trades a small portion of the time. Likewise, if you want to profit on most of your trades, you’re essentially paying for that in the sense that your frequent winners will be small profits and your infrequent losers will be much bigger. This dynamic applies equally to the choice between straddles and strangles. A straddle requires more premium outlay with a higher possibility of profiting the trade, while strangles enable you to risk less overall on the trade, but you have to be “more right” on your market view to make a profit. Your choice between these spreads when you want to make a market-neutral bet on volatility ultimately comes down to your own trading temperament, as well as which spread makes more sense given your market view. Bottom Line: Straddles and Strangles Are About Volatility For most traders, their introduction to options is related to an attraction to the leverage and convexity for their directional market bets. But as they peel the layers away and learn about the true nature of options, they learn that they’re far more than tools to get leveraged exposure to a stock or index. The first and easiest lesson is the time aspect. The longer-dated the option, the more it costs. Optionality costs money. This is very easy to grasp. One-year options should cost more than one-day options. The next step is understanding how market volatility relates to option pricing. It’s far less intuitive. But, consider this hypothetical… You’re offered the choice between paying the same price for a one-month at-the-money option on two different stocks. One is highly volatile and frequently swings 10% daily. Tesla (TSLA) is a good example. The second stock is a stable blue chip stock that doesn’t move around that much. Think something like Walmart (WMT) for instance. Most would correctly choose the volatile stock. It’s common sense, right? After all, a stock like Tesla can move up or down 30% in a month, while a stock like Walmart often swings less than 10% in a month. So like time, volatility has a price. But because future volatility is uncertain, that price is dynamic and subject to the opinion of the market. Like any market price, there are always opportunistic traders who profit from the inefficiencies of market pricing. This is where volatility trading comes in. Think of strangles and straddles as the hammer and drill of volatility trading. They’re classic tools you reach for over and over again. Remember, whenever you buy or sell an option, you’re making an implicit bet on volatility, whether you like it or not. If you buy an option, you’re taking the stance that volatility is too cheap. Related articles How We Trade Straddle Option Strategy Exploiting Earnings Associated Rising Volatility Buying Premium Prior To Earnings - Does It Work? Can We Profit From Volatility Expansion Into Earnings? Long Straddle: A Guaranteed Win? Straddle, Strangle Or Reverse Iron Condor (RIC)? Selling Strangles Prior To Earnings Straddle Option Overview Long Straddle Through Earnings Backtest Straddles - Risks Determine When They Are Best Used Long And Short Straddles: Opposite Structures

This dynamic nature of options allows you to craft a position to fit your exact market view. Perhaps there’s a big Federal Reserve meeting coming up and you expect the market to overreact, but you don’t have a specific view as to which direction. In this case, you can use a market-neutral option spread like a straddle or strangle. In the same vein, if the financial media and traders are making a big stink about something you deem a nothingburger, you can use strangles or straddles to take the view that the market will underreact to the news compared to what the market pricing expects. Strangles and straddles are market-neutral options spreads which are apathetic to the direction that price moves. They instead allow a trader to express a view on the magnitude of the price move, regardless if the price moves up or down. Let’s paint a quick hypothetical for demonstration. There’s a Federal Reserve meeting in a week. There’s tons of talk about the possibility of a Fed pivot and the dramatic implications that’d have for the global economy. Looking at the S&P 500 options for that expiration, you see that the implied volatility is very high compared to past Fed meetings. Traders are expecting the Fed to drop a surprise in some sense. Based on your own macro view, you’re unconvinced. You believe the Fed will continue their campaign of modest hikes of rates through the first half the year. In other words, you expect business as usual while the market expects radical change. As an options trader, you’re fully aware that change equals volatility and the lack of change leads volatility to contract, making most options expire worthless. You decide to sell a straddle, which involves selling an at-the-money put and an at-the-money call simultaneously. Should your view pan out, you’ll be able to pocket a good portion of the premium you collected when you opened the trade. What Is a Strangle? A strangle is market-neutral options spread that involves the simultaneous purchase or sale of an out-of-the-money call and an out-of-the-money put. So if the underlying is trading at $20.00, you might buy the $18 strike put and the $22 strike call. In this case, you’re hoping for a large price move in either direction, as your break-even price is often pretty far from the current underlying price. Let’s look at a brief example of a long strangle in $SPY using a .30 delta put and call with 27 days to expiration. Here’s the options we’re buying: ● SPY (underlying) price: 396.00 ● 1 386 FEB 27 PUT @ 4.31 (-0.30 delta) ● 1 407 FEB 27 CALL @ 3.54 (0.30 delta) ● Cost of Position: 7.85 Here’s the payoff diagram of this position: Once the position gets outside of the shaded gray area, the position is in-the-money. To provide some context to this position, SPY must move up or down roughly 4.5% for your position to be in-the-money. Let’s look at the same trade but from the short side: The details of this trade are a mirror opposite of the previous example. You’d collect a $7.85 credit, and your break-even levels are outside of the shaded gray area. You’d make this trade if you expect SPY to remain within that range through expiration (27 days). Strangle Strike Selection Strike selection is a significant factor here and there’s no correct answer really. The lower delta options you choose, the cheaper the spread and the lower the probability of profit will be. Perhaps you have a very specific market view, making strike selection obvious. But in most cases, novice option traders choose arbitrary strikes, which is a mistake. Strike selection is one of the most important aspects of trade structuring. An easy way to start being more thoughtful about selecting strikes is to view an option’s delta as a rough approximation of the probability of expiring in-the-money. This simple trick provides a lot of context to option pricing. You’ll see at-the-money options often hover around .50 delta, because the market basically has a 50/50 chance of going up or down over any time period not measured in years. As you get further from the money, deltas go down, which also makes intuitive sense. Using this framework, you can look at a .20 delta strangle and think “the market thinks there’s a 20% chance of either of these options expiring in-the-money. Is my probability forecast higher or lower than that? If you can answer this question, your strike selection becomes not only easier, but far more thoughtful. What is a Straddle? A straddle is a market-neutral options spread involving the simultaneous purchase (or sale) of a call and put at the same strike price and expiration. The goal of the trade is to make a bet on volatility in a market-neutral fashion. While any trade trade involving buying or selling a put and a call at the same strike price and expiration is technically a straddle, the majority of the time when we talk about straddles, we’re talking about an at-the-money straddle, meaning you buy a put and call at the ATM strike. In other words, if implied volatility is 20%, but you expect future realized volatility to be much higher than that, buying a straddle would provide a profit regardless of which direction the market goes, or how it arrives there. Along similar lines, if you expect realized volatility to be far less than 20%, you can short a straddle to profit from the market’s overestimation of volatility. In a word, you want to buy a long straddle when you think options are too cheap, and short straddles or short strangles when options seem too expensive. Here’s an example of a long straddle in SPY with 27 days to expiration. With SPY trading at 396 at the time of writing, we’d want to buy the 396 call and puts. Here’s how that’d look: ● SPY (underlying) at 396.00 ● 1 396 FEB 27 CALL @ 8.59 ● 1 396 FEB 27 CALL @ 7.69 ● Total cost of trade: $16.28 As you can see, this ATM straddle costs more than double what our 0.30 delta strangle costs us. Being wrong on straddles is far more painful. But this payoff diagram shows us the upside to this trade-off: What is most interesting here is that our 0.30 delta strangle from the previous example has nearly identical break-even points to this ATM straddle: around 379 and 414. However, looking at the shape of the P&L, you can see that you only experience your max P&L loss if the market goes absolutely nowhere and is still at 396 at expiration. If the market moves even modestly in either direction, your trade begins to move in your favor. This is in stark contrast to our strangle, in which we experience maximum loss at a far wider range of prices. So while you do have to shell out more premium to establish a straddle, it’s quite unlikely you’ll actually lose all of your premium. The Similarities Between a Strangle and a Straddle Both are Defined-Risk Options Spreads Both the straddle and strangle involve buying two different options without selling any options to offset the premium paid. So the most you can lose in either a straddle or strangle is the premium you paid. A defining trait of many defined-risk, long options strategies is the convexity afforded to you; you know the maximum you can lose is X, but your upside is theoretically unlimited. This can of course lead to occasional massive wins where the market basically trends in your direction until expiration. Both Are Market-Neutral Options allow you to express a more diverse array of market views than simply long or short. One of those is the ability to profit without having to predict the direction of price. While market-neutral is an easy term to use because most understand it off the bat, that’s not entirely correct. You can more accurately call straddles or strangles delta neutral strategy because while you’re neutral on the direction of price, you’re still ultimately taking some sort of market view. In the case of straddles and strangles, you’re taking a view on whether volatility will expand or contract. Or in other words, do you have conviction on whether the market will move more or less than the option market thinks? If so, you can profit from this view. Put simply, if you expect the underlying to get more volatile before expiration, you want to be long volatility. Taking a long volatility view assumes that the options market’s implied volatility forecast is too low, making options too cheap. Expressing a long volatility view in the context of a straddle or strangle means taking the long side of the trade (buying the options instead of shorting them). Just as we described in the intro of this article, if you hold the view that the market is overhyping the significance of a catalyst, you make the same trade in reverse; you can short an at-the-money put and an ATM call, which is a short straddle. If realized volatility is lower than implied volatility, then you’ll end up pocketing a good portion of premium when you close the trade. The Differences Between a Strangle and a Straddle Straddles and strangles express very similar views; traders using them are either expressing a long or short volatility while remaining agnostic on price direction. Where they differ is the magnitude of their view, or how wrong they think the market pricing of implied volatility is. From the long-volatility perspective, it’s cheaper to buy a strangle because you’re buying OTM options but the dilemma is that with cheaper OTM options, you have a lower probability of profiting from the trade. The market needs to move more to put you in the money. If you flip this dilemma to the short side, you have the same problem. When shorting strangles, you have a high probability of collecting the entire premium at the conclusion of the trade, but when the market does make a big move, you experience a huge loss. So you can rack up several wins in a row only to see one loss knock out all of these gains. ATM Straddles Have More Premium Than Strangles At-the-money options have more premium than OTM options. So it follows that the straddle, a spread with two ATM options, would have far more premium than one with two OTM options, the strangle. For this reason, systematic sellers of premium, what you might call the “Tastytrade crowd,” really like straddles for their high premium properties. This property of higher premium doesn’t make the straddle superior for premium sellers, as there’s no free lunch--premium sellers are paying for this higher level of premium with a lower win rate on their trades. Straddles Have a Higher Probability of Profit As it might’ve become clear throughout this article, constructing options spreads is all about tradeoffs. Want to put out a small amount of capital with the possibility of a huge win? You can do that, but you’ll hit on those trades a small portion of the time. Likewise, if you want to profit on most of your trades, you’re essentially paying for that in the sense that your frequent winners will be small profits and your infrequent losers will be much bigger. This dynamic applies equally to the choice between straddles and strangles. A straddle requires more premium outlay with a higher possibility of profiting the trade, while strangles enable you to risk less overall on the trade, but you have to be “more right” on your market view to make a profit. Your choice between these spreads when you want to make a market-neutral bet on volatility ultimately comes down to your own trading temperament, as well as which spread makes more sense given your market view. Bottom Line: Straddles and Strangles Are About Volatility For most traders, their introduction to options is related to an attraction to the leverage and convexity for their directional market bets. But as they peel the layers away and learn about the true nature of options, they learn that they’re far more than tools to get leveraged exposure to a stock or index. The first and easiest lesson is the time aspect. The longer-dated the option, the more it costs. Optionality costs money. This is very easy to grasp. One-year options should cost more than one-day options. The next step is understanding how market volatility relates to option pricing. It’s far less intuitive. But, consider this hypothetical… You’re offered the choice between paying the same price for a one-month at-the-money option on two different stocks. One is highly volatile and frequently swings 10% daily. Tesla (TSLA) is a good example. The second stock is a stable blue chip stock that doesn’t move around that much. Think something like Walmart (WMT) for instance. Most would correctly choose the volatile stock. It’s common sense, right? After all, a stock like Tesla can move up or down 30% in a month, while a stock like Walmart often swings less than 10% in a month. So like time, volatility has a price. But because future volatility is uncertain, that price is dynamic and subject to the opinion of the market. Like any market price, there are always opportunistic traders who profit from the inefficiencies of market pricing. This is where volatility trading comes in. Think of strangles and straddles as the hammer and drill of volatility trading. They’re classic tools you reach for over and over again. Remember, whenever you buy or sell an option, you’re making an implicit bet on volatility, whether you like it or not. If you buy an option, you’re taking the stance that volatility is too cheap. Related articles How We Trade Straddle Option Strategy Exploiting Earnings Associated Rising Volatility Buying Premium Prior To Earnings - Does It Work? Can We Profit From Volatility Expansion Into Earnings? Long Straddle: A Guaranteed Win? Straddle, Strangle Or Reverse Iron Condor (RIC)? Selling Strangles Prior To Earnings Straddle Option Overview Long Straddle Through Earnings Backtest Straddles - Risks Determine When They Are Best Used Long And Short Straddles: Opposite Structures -

The long and short straddle are normally understood only in terms of how money flows. In a long straddle, the trader pays, and risk is mainly one of time versus price movement. In a short straddle, the trader is paid, and risk involves time decay and time to expiration. But does this really explain how these two strategies work? In both forms of the straddle, the key to risk and profit potential is volatility. But the significance is opposite. A long trader tends to realize the greatest possibility of profits when underlying volatility is high; a short trader relies on declining time value and will reduce exercise risks when volatility is low. Long profits The formula for maximum profit in a long straddle is twofold, as maximum profit will be found at the upper price or the lower price: U – S – ( P + F ) = Pu S – U – ( P + F ) = Pl When U = underlying price S = strike P = premium paid F = trading fees Pu = upper profit Pl = lower profit Breakeven point also is found at two price points: S + P + F = Bu S – P + F = Bl When S = strike P = premium paid F = trading fees Bu = upper breakeven Bl = lower breakeven Finally, maximum loss occurs when the underlying price is at strike at expiration. Both sides expire worthless and loss is equal to premium paid: P + F = M When P = premium paid F = fees paid M = maximum loss For example, a long straddle consists of the following positions: Buy one 105 call, ask 3.40 plus trading fees = $349 Buy one 105 put, ask 3.10 plus trading fees = $319 Total debit $668 Possible outcomes, assuming a movement in the underlying of 8 points: Upper profit: 113 – 105 – 6.68 = $132 Lower profit: 105 – 90 – 6.68 = $832 Upper breakeven: 105 + 6.68 = $121.68 Lower breakeven: 105 – 6.68 = $98.32 Maximum loss: 6.50 + 0.18 = $668 These outcomes are diagrammed in the following payoff chart. Short profits The opposite occurs for a short straddle. Traders want underlying prices to remain as close as possible to the strike so profits will result from declining time value and, ultimately, worthless expiration. Although short straddle profits are limited to the net premiums received, the strategy is appealing to those willing to be exposed to the risk. Maximum profit is: P – F = M When P = premium received F = trading fees M = maximum profit Breakeven occurs at two points, upper and lower: S + ( P – F ) = Bu S – ( P – F ) = Bl When S = strike P = premium received Bu = upper breakeven Bl = lower breakeven Maximum loss is unlimited and depends on how far the underlying price moves. It occurs at two points: U > S – ( P – F ) U < S – ( P – F ) When U = underlying price S = strike P = premium received F = trading fees For example, a short straddle is constructed with the following positions: Sell one 105 call, bid 3.20, less trading fees = $311 Sell one 105 put, bid 2.90, less trading fees = $281 Net credit = $592 Outcomes for this trade, assuming a 215-point movement ibn the underlying, are: Maximum profit: $610 - $18 = $592 Upper breakeven: 105 + 5.92 = $110.92 Lower breakeven: 105 – 5.92 = $99.08 Upper loss: 112 – 5 – 5.92 = $108 Lower loss: 105 – 97 – 5.92 = $208 These outcomes are also summarized in the diagram. The complexity of the long and short straddle is clarified by the realization that they operate in opposite directions – limited profit versus unlimited profit, and limited risk versus unlimited risk. The nature of the short straddle must be further modified by the realization that collateral is required. For two positions, a total equal to potential exercise requires deposit of a significant sum. As a result, capital is tied up between position entry and expiration date. A completely accurate analysis should include calculation of the internal rate of return, given the requirement for depositing capital in the margin account. This is a significant variable; the longer the time to expiration, the more expensive it is to open a short straddle. Michael C. Thomsett is a widely published author with over 80 business and investing books, including the best-selling Getting Started in Options, coming out in its 10th edition later this year. He also wrote the recently released The Mathematics of Options. Thomsett is a frequent speaker at trade shows and blogs on his websiteat Thomsett Guide as well as on Seeking Alpha, LinkedIn, Twitter and Facebook. Related articles: How We Trade Straddle Option Strategy Buying Premium Prior To Earnings - Does It Work? Can We Profit From Volatility Expansion Into Earnings? Long Straddle: A Guaranteed Win? Selling Strangles Prior To Earnings Straddle Option Overview Long Straddle Through Earnings Backtest Straddles - Risks Determine When They Are Best Used

The long and short straddle are normally understood only in terms of how money flows. In a long straddle, the trader pays, and risk is mainly one of time versus price movement. In a short straddle, the trader is paid, and risk involves time decay and time to expiration. But does this really explain how these two strategies work? In both forms of the straddle, the key to risk and profit potential is volatility. But the significance is opposite. A long trader tends to realize the greatest possibility of profits when underlying volatility is high; a short trader relies on declining time value and will reduce exercise risks when volatility is low. Long profits The formula for maximum profit in a long straddle is twofold, as maximum profit will be found at the upper price or the lower price: U – S – ( P + F ) = Pu S – U – ( P + F ) = Pl When U = underlying price S = strike P = premium paid F = trading fees Pu = upper profit Pl = lower profit Breakeven point also is found at two price points: S + P + F = Bu S – P + F = Bl When S = strike P = premium paid F = trading fees Bu = upper breakeven Bl = lower breakeven Finally, maximum loss occurs when the underlying price is at strike at expiration. Both sides expire worthless and loss is equal to premium paid: P + F = M When P = premium paid F = fees paid M = maximum loss For example, a long straddle consists of the following positions: Buy one 105 call, ask 3.40 plus trading fees = $349 Buy one 105 put, ask 3.10 plus trading fees = $319 Total debit $668 Possible outcomes, assuming a movement in the underlying of 8 points: Upper profit: 113 – 105 – 6.68 = $132 Lower profit: 105 – 90 – 6.68 = $832 Upper breakeven: 105 + 6.68 = $121.68 Lower breakeven: 105 – 6.68 = $98.32 Maximum loss: 6.50 + 0.18 = $668 These outcomes are diagrammed in the following payoff chart. Short profits The opposite occurs for a short straddle. Traders want underlying prices to remain as close as possible to the strike so profits will result from declining time value and, ultimately, worthless expiration. Although short straddle profits are limited to the net premiums received, the strategy is appealing to those willing to be exposed to the risk. Maximum profit is: P – F = M When P = premium received F = trading fees M = maximum profit Breakeven occurs at two points, upper and lower: S + ( P – F ) = Bu S – ( P – F ) = Bl When S = strike P = premium received Bu = upper breakeven Bl = lower breakeven Maximum loss is unlimited and depends on how far the underlying price moves. It occurs at two points: U > S – ( P – F ) U < S – ( P – F ) When U = underlying price S = strike P = premium received F = trading fees For example, a short straddle is constructed with the following positions: Sell one 105 call, bid 3.20, less trading fees = $311 Sell one 105 put, bid 2.90, less trading fees = $281 Net credit = $592 Outcomes for this trade, assuming a 215-point movement ibn the underlying, are: Maximum profit: $610 - $18 = $592 Upper breakeven: 105 + 5.92 = $110.92 Lower breakeven: 105 – 5.92 = $99.08 Upper loss: 112 – 5 – 5.92 = $108 Lower loss: 105 – 97 – 5.92 = $208 These outcomes are also summarized in the diagram. The complexity of the long and short straddle is clarified by the realization that they operate in opposite directions – limited profit versus unlimited profit, and limited risk versus unlimited risk. The nature of the short straddle must be further modified by the realization that collateral is required. For two positions, a total equal to potential exercise requires deposit of a significant sum. As a result, capital is tied up between position entry and expiration date. A completely accurate analysis should include calculation of the internal rate of return, given the requirement for depositing capital in the margin account. This is a significant variable; the longer the time to expiration, the more expensive it is to open a short straddle. Michael C. Thomsett is a widely published author with over 80 business and investing books, including the best-selling Getting Started in Options, coming out in its 10th edition later this year. He also wrote the recently released The Mathematics of Options. Thomsett is a frequent speaker at trade shows and blogs on his websiteat Thomsett Guide as well as on Seeking Alpha, LinkedIn, Twitter and Facebook. Related articles: How We Trade Straddle Option Strategy Buying Premium Prior To Earnings - Does It Work? Can We Profit From Volatility Expansion Into Earnings? Long Straddle: A Guaranteed Win? Selling Strangles Prior To Earnings Straddle Option Overview Long Straddle Through Earnings Backtest Straddles - Risks Determine When They Are Best Used -

The reason is simple: over time the options tend to overprice the potential move. Those options experience huge volatility drop the day after the earnings are announced. In many cases, this drop erases most of the gains, even if the stock had a substantial move. In order to profit from the trade when you hold through earnings, you need the stock not only to move, but to move more than the options "predicted". If they don't, the IV collapse will cause significant losses. Kirk Du Plessis from OptionAlpha seems to agree. He conducted a backtest proving that holding a straddle through earnings is on average a losing proposition. Here are the highlights of his research. Key Points: Often times traders go through cycles where the stock makes incredibly big moves. This encourages traders to buy long straddles heading into earnings; a long call/put at the money assuming that the stock will make a big move so that you can profit from it. However, it is not the case that the stock always consistently moves more than expected in the long term. The market is smart enough to overcorrect and implied volatility always overshoots the expected move, on average. Case Study 1: Apple Did a long straddle every time earnings were present, all the way back to 2007 through now. This is a lot of earnings cycles and a lot of different information for Apple. Since then Apple has had a considerable move, which really challenges the validity of the strategies. We entered a long straddle at the money the day before earnings and took it off the next day. The stock was trading at $90; we bought the 90 put and the 90 call and closed it right after earnings were announced the next morning. Results: A long straddle in Apple for earnings only ended up winning 41.38% of the time. The average return over 10 years was -1.31%. Over the long haul, a long option strategy results in a negative expected return, especially in a stock like Apple. On the opposite end of this trade, if you had done the short straddle instead of buying options, you would have generated at least 60% of the time and expected a positive return. The straddle price before earnings, on average, was $15. The straddle price directly after earnings went down to about $7.95; not a great choice for long-option buyers. Case Study 2: Facebook Entered the same long straddle position, entering right before earnings were announced and exiting again right after earnings were announced. This strategy only won 27% of the time, which is a huge miss for Facebook percentage-wise. These long options strategy simply do not perform as well as we think over time. Results: Had an annual return of 0.70%. Only a couple of months ended up being the determining factor to keep it above board. If you missed a couple of those really big moves or if Facebook moved much higher than expected, then it would have resulted in a much more negative return. On the counter side, if you had traded the short option strategy it would have worked out well, generating a positive expected return. On average, the market priced these straddles at about $5.62 before earnings. After they announced earnings, the straddle pricing went down to $1.78. The key was that the crash in the volatility and the straddle pricing is really why this strategy was a big loser. However, this was a really good winner for option sellers. The average expected move in Facebook was $6.45 and the actual expected move on Facebook was $7.09. Facebook out-performed on average. If you could remove the biggest outlier from 2013, then Facebook under-performs by $6.16. More recently, Facebook has begun to consistently under-perform its expected moves. Case Study 3: Chipotle With Chipotle we used the same strategy as with Apple and Facebook, entering into a long straddle right before earnings and exiting it right after earnings. Results: The overall win rate was 35.48%. The average annual return was -2.59%, losing a significant amount of money in the trade. This again consistently led option sellers to be the beneficiaries of the earnings trade in Chipotle. The average price of the straddle heading into the earnings event was 26.26%. The stock went from the low 60's, all the way up to the 600's and back down to 400 - so the straddles are naturally going to be more pricey. On average the straddle price was 26.26 and after earnings the straddle price was 11.21, collapsing by more than half. There are huge moves in Chipotle, but they do not overshadow what actually happened in the long term. Expected move in Chipotle was 7.01 and the actual move was 5.28 - the market vastly underperformed. Conclusion: After big moves, we start to see expected moves and the stock expands and then smaller moves follow. Generally speaking, when the stock outperforms the expectation the next couple of cycles end up being fairly quiet. If we do find ourselves in a quiet period where the stock has performed really well, we should be careful that it could surprise us shortly. Likewise, if the stock has been really volatile and has outperformed and moved more than expected in the last couple of cycles that means we could potentially be more aggressive as it might underperform heading forward. Generally, there is also a lag time between the market catching up - earnings trades only happen four times a year. The market participants don't get a lot of data throughout the year to make changes to expectations and trading habits. If the stock has a huge move after earnings, more than expected, it might take a cycle or two for the options pricing to catch up and realize the new normal. At the end of the day, realizing how much these numbers gravitate towards what they should be on average, long-term is really powerful. You can listen to the full podcast here. This research confirms what we already knew: It is easy to get excited after a few trades like NFLX, GMCR or AMZN that moved a lot in some cycles. However, chances are this is not going to happen every cycle. There is no reliable way to predict those events. The big question is the long term expectancy of the strategy. It is very important to understand that for the strategy to make money it is not enough for the stock to move. It has to move more than the markets expect. In some cases, even a 15-20% move might not be enough to generate a profit. Thank you Kirk! The next question is of course: if holding a long straddle through earnings is a losing proposition, why not to take the other side and short those straddles? But lets leave something for the next article.. Related articles: How We Trade Straddle Option Strategy Buying Premium Prior To Earnings - Does It Work? Can We Profit From Volatility Expansion Into Earnings? Long Straddle: A Guaranteed Win? Why We Sell Our Straddles Before Earnings Selling Strangles Prior To Earnings Straddle Option Overview

The reason is simple: over time the options tend to overprice the potential move. Those options experience huge volatility drop the day after the earnings are announced. In many cases, this drop erases most of the gains, even if the stock had a substantial move. In order to profit from the trade when you hold through earnings, you need the stock not only to move, but to move more than the options "predicted". If they don't, the IV collapse will cause significant losses. Kirk Du Plessis from OptionAlpha seems to agree. He conducted a backtest proving that holding a straddle through earnings is on average a losing proposition. Here are the highlights of his research. Key Points: Often times traders go through cycles where the stock makes incredibly big moves. This encourages traders to buy long straddles heading into earnings; a long call/put at the money assuming that the stock will make a big move so that you can profit from it. However, it is not the case that the stock always consistently moves more than expected in the long term. The market is smart enough to overcorrect and implied volatility always overshoots the expected move, on average. Case Study 1: Apple Did a long straddle every time earnings were present, all the way back to 2007 through now. This is a lot of earnings cycles and a lot of different information for Apple. Since then Apple has had a considerable move, which really challenges the validity of the strategies. We entered a long straddle at the money the day before earnings and took it off the next day. The stock was trading at $90; we bought the 90 put and the 90 call and closed it right after earnings were announced the next morning. Results: A long straddle in Apple for earnings only ended up winning 41.38% of the time. The average return over 10 years was -1.31%. Over the long haul, a long option strategy results in a negative expected return, especially in a stock like Apple. On the opposite end of this trade, if you had done the short straddle instead of buying options, you would have generated at least 60% of the time and expected a positive return. The straddle price before earnings, on average, was $15. The straddle price directly after earnings went down to about $7.95; not a great choice for long-option buyers. Case Study 2: Facebook Entered the same long straddle position, entering right before earnings were announced and exiting again right after earnings were announced. This strategy only won 27% of the time, which is a huge miss for Facebook percentage-wise. These long options strategy simply do not perform as well as we think over time. Results: Had an annual return of 0.70%. Only a couple of months ended up being the determining factor to keep it above board. If you missed a couple of those really big moves or if Facebook moved much higher than expected, then it would have resulted in a much more negative return. On the counter side, if you had traded the short option strategy it would have worked out well, generating a positive expected return. On average, the market priced these straddles at about $5.62 before earnings. After they announced earnings, the straddle pricing went down to $1.78. The key was that the crash in the volatility and the straddle pricing is really why this strategy was a big loser. However, this was a really good winner for option sellers. The average expected move in Facebook was $6.45 and the actual expected move on Facebook was $7.09. Facebook out-performed on average. If you could remove the biggest outlier from 2013, then Facebook under-performs by $6.16. More recently, Facebook has begun to consistently under-perform its expected moves. Case Study 3: Chipotle With Chipotle we used the same strategy as with Apple and Facebook, entering into a long straddle right before earnings and exiting it right after earnings. Results: The overall win rate was 35.48%. The average annual return was -2.59%, losing a significant amount of money in the trade. This again consistently led option sellers to be the beneficiaries of the earnings trade in Chipotle. The average price of the straddle heading into the earnings event was 26.26%. The stock went from the low 60's, all the way up to the 600's and back down to 400 - so the straddles are naturally going to be more pricey. On average the straddle price was 26.26 and after earnings the straddle price was 11.21, collapsing by more than half. There are huge moves in Chipotle, but they do not overshadow what actually happened in the long term. Expected move in Chipotle was 7.01 and the actual move was 5.28 - the market vastly underperformed. Conclusion: After big moves, we start to see expected moves and the stock expands and then smaller moves follow. Generally speaking, when the stock outperforms the expectation the next couple of cycles end up being fairly quiet. If we do find ourselves in a quiet period where the stock has performed really well, we should be careful that it could surprise us shortly. Likewise, if the stock has been really volatile and has outperformed and moved more than expected in the last couple of cycles that means we could potentially be more aggressive as it might underperform heading forward. Generally, there is also a lag time between the market catching up - earnings trades only happen four times a year. The market participants don't get a lot of data throughout the year to make changes to expectations and trading habits. If the stock has a huge move after earnings, more than expected, it might take a cycle or two for the options pricing to catch up and realize the new normal. At the end of the day, realizing how much these numbers gravitate towards what they should be on average, long-term is really powerful. You can listen to the full podcast here. This research confirms what we already knew: It is easy to get excited after a few trades like NFLX, GMCR or AMZN that moved a lot in some cycles. However, chances are this is not going to happen every cycle. There is no reliable way to predict those events. The big question is the long term expectancy of the strategy. It is very important to understand that for the strategy to make money it is not enough for the stock to move. It has to move more than the markets expect. In some cases, even a 15-20% move might not be enough to generate a profit. Thank you Kirk! The next question is of course: if holding a long straddle through earnings is a losing proposition, why not to take the other side and short those straddles? But lets leave something for the next article.. Related articles: How We Trade Straddle Option Strategy Buying Premium Prior To Earnings - Does It Work? Can We Profit From Volatility Expansion Into Earnings? Long Straddle: A Guaranteed Win? Why We Sell Our Straddles Before Earnings Selling Strangles Prior To Earnings Straddle Option Overview -