This cycle was no exception.

It is a well known fact that Implied Volatility of options increases before earnings. We usually take advantage of this phenomenon by buying a straddle option few days before the earnings date.

However, Oracle case was slightly different. As I mentioned, they follow a similar pattern of earnings dates in the last few years (third week of the month), but for some reason, the options market tends to be "surprised" after the earnings date is actually confirmed.

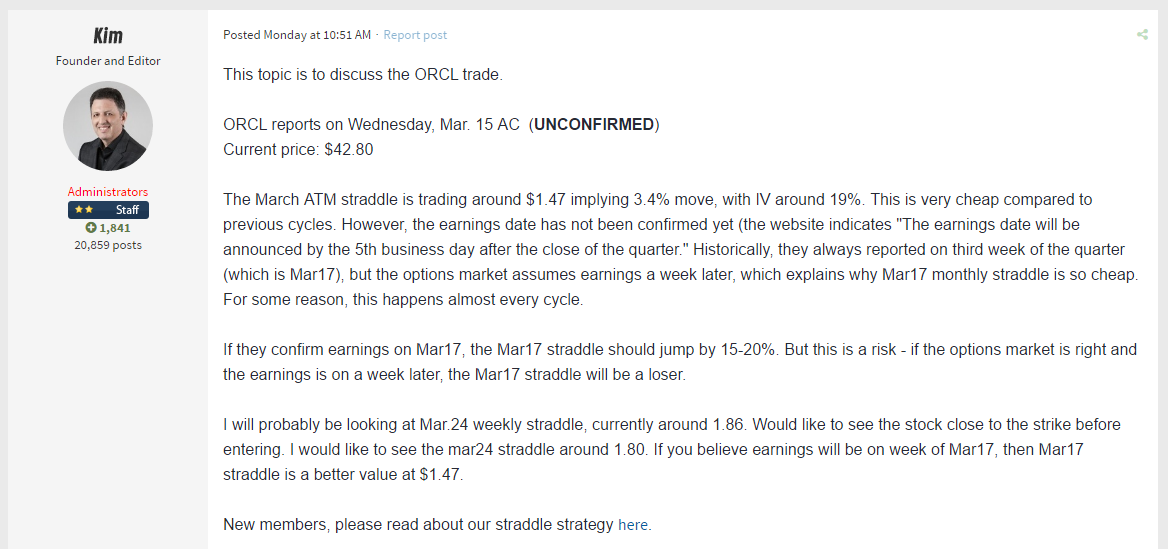

On February 27 I opened ORCL trade discussion topic and posted the following information:

My initial intention was to trade the Mar.24 straddle, which would be a safer bet.

However, after checking again the previous cycles and seeing the Mar.17 straddle dipping below $1.45, I decided to take the risk and execute the Mar.17 straddle. The trade has been posted on the forum on Mar.01:

I posted the rationale for selecting the Mar.17 expiration, with all supporting information, including the risks:

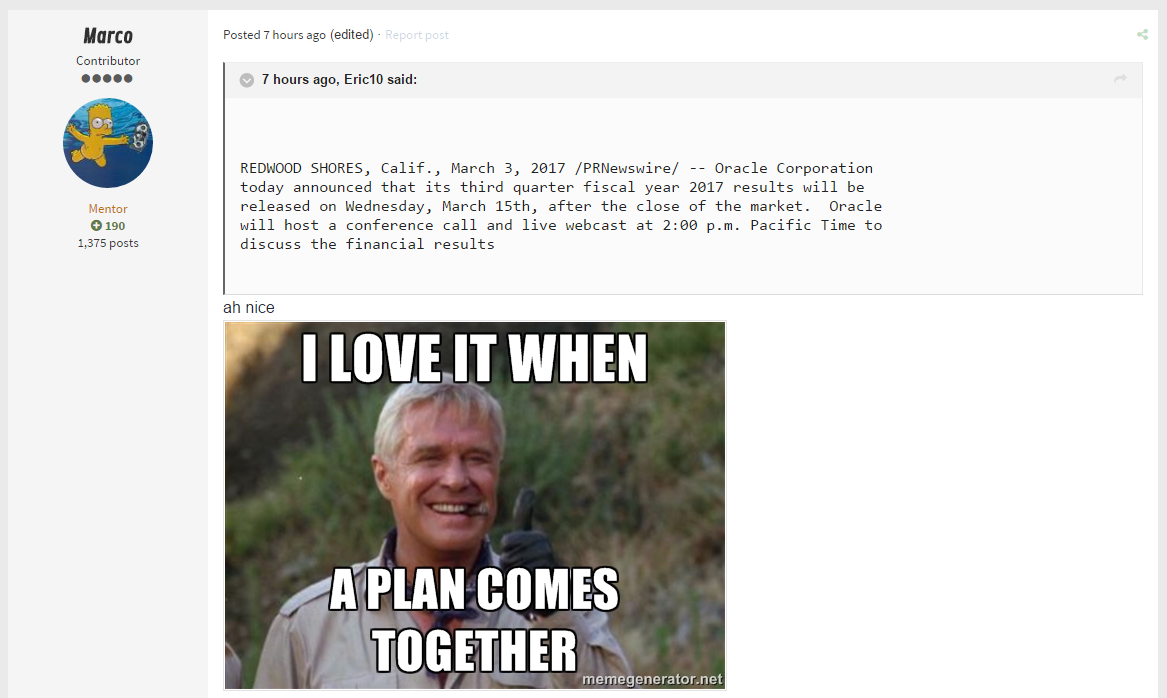

Two days later, Oracle confirmed earnings on Mar.15, as expected.

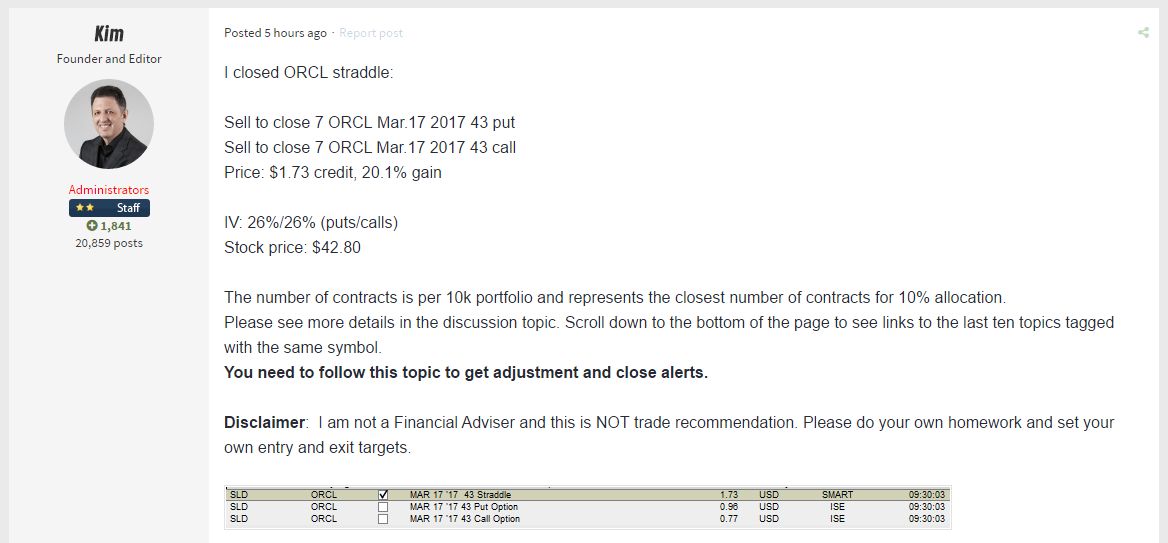

IV of Mar.17 options jumped 4 points after the date has been confirmed, and we closed the trade for 20.1% gain.

This is a great example how we make Implied Volatility to work for us. We implement few strategies that take advantage of Implied Volatility changes around the earnings event.

Of course, this trade was not without risks. If earnings were confirmed on week of Mar.24, the Mar.17 straddle could easily lose ~40%. But options trading is a game of probabilities. Based on previous cycles, I estimated that there was ~90% chance that earnings will be on week of Mar.17. Making 20% 9 out of 10 times and losing 40% in one trade still puts you far ahead, with 140% cumulative gain. I also provided members all the necessary information so everyone could make an educated decision.

At SteadyOptions, the learning never stops. If you think education is expensive, try ignorance.

Related Articles:

How We Trade Straddle Option Strategy

Buying Premium Prior to Earnings

Can We Profit From Volatility Expansion into Earnings

Long Straddle: A Guaranteed Win?

Why We Sell Our Straddles Before Earnings

Options Trading Greeks: Vega For Volatility

Want to learn more? We discuss all our trades on our forum.

Join the conversation

You can post now and register later. If you have an account, sign in now to post with your account.

Note: Your post will require moderator approval before it will be visible.