The problem is that many stocks spend more time in consolidation than in either bullish or bearish trends. At these times, a strategy designed to generate cash with minimal market risk would be ideal. This is where the covered straddle is valuable.

Short straddles are associated with high exercise risk because both sides are short. This means that the likelihood of one side being in the money is just about unavoidable. For this reason, many traders avoid short straddles, and for good reason. The risk is obvious: Premium income must be greater than the loss upon exercise, and this often is so marginal that net losses can and do occur.

The whole situation changes drastically when the short call is covered. The covered straddle consists of owning 100 shares, writing one covered call, and writing one uncovered put. The market risk of the uncovered put is the same as the market risk of the covered call. As a result, market risk on both sides is drastically reduced simply by converting a naked call to a covered call.

This doesn’t mean losses cannot occur. If the stock declines suddenly, well below the level of net premium received, the loss will result. As a result, traders should be prudent about which stock they choose for covered straddles and should be willing to close out positions once one side or the other becomes profitable. The most likely timing for a successful covered straddle is when the stock is range-bound and in consolidation.

Keeping on eye on price moving toward breakout from consolidation is a smart way to avoid unpleasant surprises. All trends end, including consolidation. Being aware of the potential for breakout, and especially for a sudden and rapid breakout, requires diligence and the need to act quickly. The plan for a covered straddle is to exploit time decay, and profits can be taken as long as the price remains within the existing boundaries of the trading range.

With this tactic in mind, it makes sense to open covered straddles that expire within one to two weeks. Premium income would be greater for longer-term expirations, but that also means accepting much greater risks. In most cases, you will see more profits from time decay in a series of one-week and two-week covered straddles, than from longer-term positions.

The covered straddle, like the more traditional short straddle without cover, consists of equal numbers of calls and puts, opened with the same strike and expiration. However, by also owning 100 shares for each set of contracts, the call side’s risk is drastically reduced. Because the market risk of each side is identical, a covered straddle contains the same market risk as writing two covered calls. The difference is that you do not need to double the number of shares held at the time the position is opened.

Maximum profit will take place at expiration when the underlying is trading at the strike. This will rarely happen so on practical basis, assume maximum profit will be equal to the underlying trading at or above the strike, adjusted by the underlying price and by net premium earned:

( P – F ) + S – Ub = M

P = premium received

F = trading fees

S = strike

Ub = basis in underlying

M = maximum profit

A breakeven point occurs at underlying price plus strike, minus net premium earned:

( Ub + S – ( P – F )) ÷ 2 = B

Ub = basis is underlying

S = strike

P = premium received

F = trading fees

B = breakeven

The problem with a covered straddle is that net losses are unlimited. Although the uncovered put has the same market risk as the covered call the underlying price could decline a good distance (but is not truly unlimited, because price will not decline beyond zero). Maximum loss is calculated as:

( Ub – Uc ) + ( Pc – Pb ) = M

Ub = underlying basis price

Uc = underlying current price

Pc = put, current premium

Pb = put, net sale premium

M = maximum loss

This overall net loss has three components. First is the loss on stock; second is loss on the put; and third is an adjustment for the net premium earned. However, this worst case outcome is not always earned; in fact, it can be avoided in most instances. The stock loss is unrealized unless stock is disposed of at a net loss. The paper loss on the short put can be deferred or avoided by rolling forward to avoid the loss resulting from exercise.

In other words, the structure of this strategy enables you to exert control and to manage losses to minimize or avoid them altogether.

An example of the strategy:

- 100 shares purchased @ $102, $10,200 plus trading fees = $10,209

- Sell 105 call, bod 3.20, less trading fees = $311

- Sell 105 put, bid 2.90, less trading fees = $281

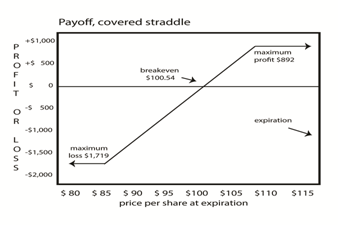

Outcomes for this trade, assuming the stock price ends up at either $105 (at the top) or $92 (at the bottom) are:

- Maximum profit: 5.92 + ( 105 – 103 ) = 8.92 ($892)

- Breakeven: ( 102 + 105 – 5.92 ) ÷ 2 = 100.54 ($100.54)

- Maximum loss: ( 102 – 92 ) + 10 – 2.81 ) = 17.19 ($1,719)

Actual outcomes rely, of course, on where the stock price ends up. The result above is summarized in the illustration below.

The worst case analysis is just that, the outcome if a trader does not act to close positions once stock price movement begins. Whether prices move up or down, one side or the other can be closed and profits taken. This advantage is maximized if the consolidation trend continues in effect.

The covered straddle is often overlooked with the point of view that options trades only work when a bullish or bearish trend is underway. This strategy is an exception, and it can lead to profits while you wait for a new dynamic trend to begin.

Michael C. Thomsett is a widely published author with over 80 business and investing books, including the best-selling Getting Started in Options, coming out in its 10th edition later this year. He also wrote the recently released The Mathematics of Options. Thomsett is a frequent speaker at trade shows and blogs on his websiteat Thomsett Guide as well as on Seeking Alpha, LinkedIn, Twitter and Facebook.

Related articles:

- How We Trade Straddle Option Strategy

- Long Straddle: A Guaranteed Win?

- Selling Strangles Prior To Earnings

- Straddle Option Overview

- Straddles - Risks Determine When They Are Best Used

There are no comments to display.

Join the conversation

You can post now and register later. If you have an account, sign in now to post with your account.

Note: Your post will require moderator approval before it will be visible.