Leaderboard

Popular Content

Showing content with the highest reputation on 09/14/18 in all areas

-

It's like finding a $50 bill on the ground.. Exciting, yet terrifying. Should I pick it up? Should I keep it? Is it a trap?4 points

-

I just closed at 10.60. I prefer to get out. I don't understand what risks i'm actually taking and don't want to find out. Good luck if you are still in it.3 points

-

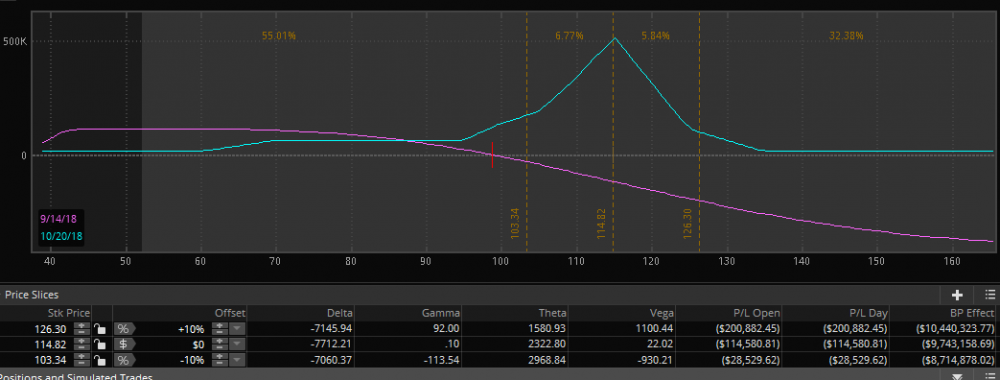

My position is below. Not sure thinkorswin is calculating correctly. I have like 14K guaranteed profit in this riskless butterfly trade. I'm getting really nervous. Sold almost 1000 butterflies at various stikes. I have to hold this til expiration.

2 points

2 points -

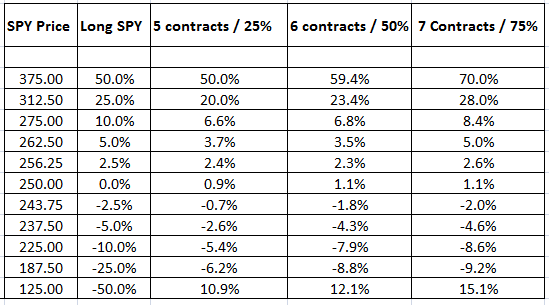

Important: the first part of this post describes the general concept of the Anchor strategy. In January 2019 the implementation has been changed and Leveraged Anchor was born. The Leveraged Anchor implementation is described in the second part of the post The strategy description has been provided by Chris Welsh. Welcome to Anchor Trades! I would like to personally welcome all our members, those who have come from SteadyOptions, Seeking Alpha, and those which have come from elsewhere. I would encourage everyone to read the Anchor Frequently Asked Questions and the Anchor Trade Strategy topics. Those two topics should provide answers to the majority of your questions, as well a detailed discussion on what the Anchor Strategy is all about. You can see the Anchor Trades performance here. So What is an Anchor Trade? To put it simply, an Anchor Trade should be one that forms the keystone of any investment portfolio -- that reliable corner that you know you can depend on, regardless of market conditions. The one that lets you sleep at night, knowing your money is at work, but not subject to large risks. An Anchor trade's goal is to prevent loss of capital while still generating a positive net return in all market conditions. This strategy began with the premise that it must be possible to virtually fully hedge against market losses, without sacrificing all upside potential. Anchor trades are concerned for full year, full portfolio, protection, regardless of market conditions. Many investors try to insure against losses after those losses have already been incurred, or as they are occurring in real time – this is a mistake. It’s easy to be an investor during a prolong bull market, but what happens when a severe, or even mild, market correction occurs? At that point many investors find themselves trapped in falling positions, have stop losses kicking in, and are at a loss as what to do – other than to watch their principle dissipate. In the modern era of flash crashes, swift market volatility changes, and world risk it simply makes no sense to be invested in anything without portfolio protection. It is impossible to routinely predict the next negative major market event, therefore 365 days of protection is a necessity. I have given up trying to predict the day to day movements of the market -- therefore I Anchor my portfolio with this strategy (which can easily then be paired with other strategies). In the current market environment, such precautions are particularly warranted. It is my opinion that much of the recent market gains have been artificially propped up by low interest rates, the Federal Reserve, and the lack of alternative investment choices which can provide income to investors. At some point in the future the market is due, at the very least, for a correction, if not a significant down turn. With increasing turmoil in Syria, North Korea, and elsewhere in the Middle East, who knows what could tip the markets. Will this occur within two weeks, six months, one year, or even longer is something I've given up trying to predict. Rather I seek to protect against such events – whenever they may occur. Some strategies try to partially hedge against market risk through long short strategies, through the straight purchase of puts (typically out of the money at a substantial cost to the portfolio), through default swaps, or through numerous other instruments. However, each of these strategies only offers partial portfolio protection which either comes at a cost or which just assumes a set loss in the portfolio (such as ten or fifteen percent) is acceptable. I refuse to accept that philosophy and have developed a strategy around annual portfolio protection. Performance targets The impact of not experiencing losses in down market years, while only slightly lagging (if lagging at all) in positive and neutral years, is astronomical over any extended period of time. Utilizing the Anchor strategy over a number of years, particularly if any of those years are bear markets, should lead to the strategy significantly outperforming the markets as a whole, as back-testing has demonstrated. Even in prolonged bull markets, the returns should still be positive and lag negligibly behind. The peace of mind which comes with being fully hedged more than compensates for the potential of slightly underperforming the market as a whole in prolonged bull scenarios. Special thanks to Reel Ken, Kim Klaiman, and others who helped me evolve this strategy to its current form through their articles and discussions. Anchor Trade objective The Anchor strategy's s primary objective is to have positive returns in all market conditions on an annual basis. Anchor Trades will be divided into two separate forums: 1. The Anchor Trades forum will post my actual trades from my individual account, including weekly rolls, and any adjustments I make, as well as the price I received when filled. It will also include a thread for "model" trades that will be launched monthly. Model trades will be for those members who join after the initial actual trades are established, so any member can set up their own Anchor Portfolio. This way any member, regardless of when they join, will have a thread to follow applicable from their initial membership date. If you want to get notifications about the trades, you should follow this forum (by clicking "Follow this forum" button). If you follow this forum, you will receive an email when a new topic (trade) is posted. 2. The Anchor Trades Discussions forum will discuss each trade that has been made, detail the calculations behind the decision, and provide a Q&A forum for members to ask about any one trade. The thread will also have columns about the theory behind the Anchor strategy, implementation discussions, and be open to members to ask general questions. The Anchor objective is to produce equity like returns over a full market cycle, with reduced volatility and bear market drawdowns. If you have any questions about the threads, where information can be found, or just general questions, please feel free to send a message to either Kim or myself. I look forward to helping all member learn about this strategy and hopefully implement it themselves. January 2019 update - Leveraged Anchor In January 2019 we started tracking the leverage version of the Anchor for performance purposes. The leveraged version has been extensively backtested to fine tune the system for optimal results. Here are the highlights of the new implementation: We now use deep in the money calls, as opposed to long stock positions, and we are able to gain leverage without having to utilize margin interest. Given the rising interest rate environment we are in, and the high cost of margin interest rates generally, this can lead to significant savings; When we enter the trade, we look for a long call that has a delta of around 90. As the market falls, delta will shrink. For instance, if SPY were to decline ten percent, our long calls would have declined by less than nine percent. The closer we get to our long strike, the slower this decline; In the event of very large crashes, we can actually make money. See How Anchor Survived The 2020 Crash. Losses are capped. In the below example, the maximum loss is 9.5%. This can increase if we keep rolling the short puts throughout the downturn, but in any one “crash,” losses are limited to the ten percentage point mark (in Traditional Anchor this 9.5% max loss in one period is better, coming in at 8.5%). If we apply a momentum filter as well, then the risk of continuingly losing on the short puts declines; Please read The Downside Of Anchor for more details. In larger bull markets, the Leveraged Anchor outperforms both Traditional Anchor and simply being long stock as there is actual leverage being used. Some of this will depend on just how fast the market is rising and how often the long hedge is rolled, but in large bull markets, it should still regularly outperform. In fact, in any one period where the market grows more than 3.5% to 4.0%, the Leveraged Anchor will outperform simply being long SPY. The Leveraged version of Anchor will always outperform Traditional Anchor in any up markets. One question that must be addressed is just how much leverage to use? Luckily this is very easy to model on a thirty day period, with SPY at 250: Above is a table showing the performance of SPY, then using 25% leverage, 50%, and 75% leverage after certain market moves over a thirty day period. After reviewing the above, and similar tables over longer periods of time, we made a decision that utilizing 50% leverage was optimal. You of course can adjust, taking on more leverage, or less, as you see fit. Note the above table does not include any gains from BIL dividends. That should add around 10 to 20 basis points more performance per month on the leveraged versions. Overall, we should expect the leveraged to slightly outperform the market in strong bull markets, significantly outperform in strong bear markets, and slightly underperform in sideways or slightly up/down markets (+-10%). You can read more about the strategy here. Since inception, the leveraged Anchor is up 296.0%, compared to S&P 500 return of 173.1% (as of 12/31/2025). We also recommend reading How Anchor Survived the 2020 Crash. On March 19 2020, SPY at 234 (down 30%), Anchor UP $5k (~3%). Click here for a full analysis of 2022 performance.

1 point

1 point -

The options, by themselves, are not dangerous tools. I mention that because one of the long-lasting misconceptions about options is that they are dangerous to use. It is possible to use options to speculate (gamble), but options were created as hedging, or risk-reducing, investment tools. An alarming number of financial professionals, including stockbrokers, financial planners and journalists are in position to educate the public about the many advantages to be gained from adopting naked put writing (and other option strategies), but fail to do so. Many public investors never bother to make the effort to learn about options once they hear negative statements from professional advisors. Except for extremely bearish prognosticators, no one ever suggests that owning stock is anything but the most prudent of investment strategies. Yet, writing naked puts is a significantly more conservative strategy and definitely less risky than simply buying and owning stocks. As such it deserves to be considered as an attractive investment alternative by millions of investors. Who should consider writing naked (uncovered) puts? 1. Investors Who are bullish on the market Who are bullish on specific stocks Who want to buy a specific stock at a lower price Who adopt a buy and hold strategy Who want additional income from their holdings 2. Traders Who want a higher percentage of winning trades Willing to consider holding a position for a month or two Who want to begin a spread position with a bullish leg Strategy Objective Why would you want to write naked puts? What is there to be gained? Writing naked puts is a bullish strategy. When selling naked put options, you are attempting to achieve one of two investment goals Profit. You are bullish on the stock and expect the put option to lose value, and perhaps expire worthless as time passes. If the latter happens, the option premium (cash from selling the put option) becomes the profit. Buy stock at a discount. If the put option is in the money when expiration arrives, you will be assigned an exercise notice and be obligated to buy the stock you want to own at a discount to today’s price. This is an intelligent method for an investor to gradually add positions to a long-term portfolio. NOTE: When you are eventually assigned that exercise notice, the stock may be below your target purchase price. However, if you had entered an order to buy stock at that target price, you would be in worse shape than the put seller (who cushioned any loss by the amount of the premium). Another alternative is combining put selling with call selling, a strategy known as the Wheel strategy This post was presented by Mark Wolfinger and is an extract from his latest book Writing Naked Puts (The Best Option Strategies). You can buy the book at Amazon or sign up for our free trial and get it for free. Mark Wolfinger has been in the options business since 1977, when he began his career as a floor trader at the Chicago Board Options Exchange (CBOE). Mark has published four books about options. His Options For Rookies book is a classic primer and a must read for every options trader. Mark holds a BS from Brooklyn College and a PhD in chemistry from Northwestern University.1 point

The options, by themselves, are not dangerous tools. I mention that because one of the long-lasting misconceptions about options is that they are dangerous to use. It is possible to use options to speculate (gamble), but options were created as hedging, or risk-reducing, investment tools. An alarming number of financial professionals, including stockbrokers, financial planners and journalists are in position to educate the public about the many advantages to be gained from adopting naked put writing (and other option strategies), but fail to do so. Many public investors never bother to make the effort to learn about options once they hear negative statements from professional advisors. Except for extremely bearish prognosticators, no one ever suggests that owning stock is anything but the most prudent of investment strategies. Yet, writing naked puts is a significantly more conservative strategy and definitely less risky than simply buying and owning stocks. As such it deserves to be considered as an attractive investment alternative by millions of investors. Who should consider writing naked (uncovered) puts? 1. Investors Who are bullish on the market Who are bullish on specific stocks Who want to buy a specific stock at a lower price Who adopt a buy and hold strategy Who want additional income from their holdings 2. Traders Who want a higher percentage of winning trades Willing to consider holding a position for a month or two Who want to begin a spread position with a bullish leg Strategy Objective Why would you want to write naked puts? What is there to be gained? Writing naked puts is a bullish strategy. When selling naked put options, you are attempting to achieve one of two investment goals Profit. You are bullish on the stock and expect the put option to lose value, and perhaps expire worthless as time passes. If the latter happens, the option premium (cash from selling the put option) becomes the profit. Buy stock at a discount. If the put option is in the money when expiration arrives, you will be assigned an exercise notice and be obligated to buy the stock you want to own at a discount to today’s price. This is an intelligent method for an investor to gradually add positions to a long-term portfolio. NOTE: When you are eventually assigned that exercise notice, the stock may be below your target purchase price. However, if you had entered an order to buy stock at that target price, you would be in worse shape than the put seller (who cushioned any loss by the amount of the premium). Another alternative is combining put selling with call selling, a strategy known as the Wheel strategy This post was presented by Mark Wolfinger and is an extract from his latest book Writing Naked Puts (The Best Option Strategies). You can buy the book at Amazon or sign up for our free trial and get it for free. Mark Wolfinger has been in the options business since 1977, when he began his career as a floor trader at the Chicago Board Options Exchange (CBOE). Mark has published four books about options. His Options For Rookies book is a classic primer and a must read for every options trader. Mark holds a BS from Brooklyn College and a PhD in chemistry from Northwestern University.1 point -

Very short of 27M. I feel I'm getting over my head. I need a walk.1 point

-

Smart choice. If you are able to sell something for greater than it's maximum value it dosn't mean that you will be able to buy it back at maximum value and lock in that profit. Hence, selling a $10 spread for $11 is no guaranty that you just made a risk free profit because the market is not there to allow you to close it out. And, if you are dealing with options that are expiring today, there is automatic exercise unless the holder of the long option notifies the broker by 4:30 pm EST not to exercise that option. It opens up a floodgate of unknown possibilities that can take place in after hours trading leaving you uncertain of where you stand.1 point

-

It definitely could be a good strategy, but the key is position sizing. In other words, don't write more puts than the amount of stock you are willing to own. More reading: Selling Naked Put Options The Naked Put, A Low-Risk Strategy1 point

-

a lot filled at a lot lower.1 point

-

I would take a look at the daily volume of the options you are considering to verify liquidity.1 point

-

It depends on the stock, but usually few dozens of contracts shouldn't be an issue.1 point

-

Uncovered put Covered call Dividends are not earned. Dividends are earned as long as shares are held. The uncovered put can be exercised, but this can be avoided easily, by closing the position, rolling it forward, or waiting for worthless expiration. Covered calls can be exercised, and 100 shares of stock must be delivered at the strike. Exercise can be avoided by closing or rolling the in-the-money covered call. Time is an advantage. The closer to expiration, the more rapidly time value declines. The uncovered put can be closed at a profit or allowed to expire worthless. Time is an advantage. The closer to expiration, the more rapidly time value declines. The covered call can be closed at a profit or allowed to expire worthless. Moneyness determines whether to close or roll the uncovered put. An out-of-the-money put will expire worthless; an in-the-money put is at risk of exercise. Moneyness determines whether to close or roll the covered call. An out-of-the-money call will expire worthless and can be replaced; an in-the-money call is at risk of exercise, in which case shares will be given up at the strike. Collateral is required equal to 20 percent of the strike value, minus premium received for selling the put. This is advantageous leverage when compared to the covered call. No collateral is required for a covered call. However, to buy 100 shares of the underlying, 50 percent must be paid, and the remaining 50 percent is bought on margin. The timing for opening a naked put is essential to reduce exposure to unwanted exercise. The best position for a naked put is when the underlying price moves through support and you expect price to retrace back into range. For example, the chart for Amazon.com (AMZN) shows examples of when this occurred. The highlighted price moves both fell below the trendline shown on the chart. Given the long-term bullish trend for AMZN, it was reasonable to expect the price to reverse to the upside. This is what occurred in both instances. A second consideration is creation of a buffer zone between current price per share and the selected strike for the short put. Because AMZN is a high-priced stock, the opportunities for buffer zones are significant. For example, after the huge decline in February from nearly $1,500 per share down to 21,350 by February 6, anticipating a rebound would be well-timed. During the trading day of February 8 and about 30 minutes into the session,AMZN was trading at $1,416.36 per share. A couple of naked put trades to consider at that moment: The 1,410 put expiring in one day (Feb. 9) was at a bid of 10.05. This is incredibly rich considering the one-day expiration. The strike was six points below current price. That, plus the net $1,000 for selling the put, sets up a buffer zone of 16 points. The 1,362.50 put expiring in eight days (Feb. 16) showed a bid price of 13.05. This is 54 points below current price. Adding the 13 points received for selling the put, this creates a 67-point buffer zone over an exposure period of eight days. Time decay will be rapid. Typically, options expiring in one week lose 34% of their remaining time value between Friday and Monday. In this example, that spans February 9 to 12 – three calendar days but only one trading day. The timing and buffer zone are the two keys to a successful short put strategy. Whether you select extremely short-term (one day) or a little longer (eight days), the profit potential is attractive, in large part due to the recent volatility in the market and in AMZN, which fell 150 points in two days. The extreme move in price makes the point that timing is everything with this strategy. The likely bargain hunting at such a low price makes an upward move likely. By February 8, price had always moved from the low of $1,350 to $1,416, recovery of 66 points out of the 150 points previously lost. As with all options strategies, especially those involving a short position, this one has to be monitored every day. Because things change rapidly in volatile markets, you need to get out when you can to maximize profits or, in worst case situations, to mitigate losses. The need for a buffer zone and attractive premium levels makes the naked put a potentially profitable strategy, even for the conservative trader. Michael C. Thomsett is a widely published author with over 80 business and investing books, including the best-selling Getting Started in Options, coming out in its 10th edition later this year. He also wrote the recently released The Mathematics of Options. Thomsett is a frequent speaker at trade shows and blogs on his website at Thomsett Publishing as well as on Seeking Alpha, LinkedIn, Twitter and Facebook.1 point

Uncovered put Covered call Dividends are not earned. Dividends are earned as long as shares are held. The uncovered put can be exercised, but this can be avoided easily, by closing the position, rolling it forward, or waiting for worthless expiration. Covered calls can be exercised, and 100 shares of stock must be delivered at the strike. Exercise can be avoided by closing or rolling the in-the-money covered call. Time is an advantage. The closer to expiration, the more rapidly time value declines. The uncovered put can be closed at a profit or allowed to expire worthless. Time is an advantage. The closer to expiration, the more rapidly time value declines. The covered call can be closed at a profit or allowed to expire worthless. Moneyness determines whether to close or roll the uncovered put. An out-of-the-money put will expire worthless; an in-the-money put is at risk of exercise. Moneyness determines whether to close or roll the covered call. An out-of-the-money call will expire worthless and can be replaced; an in-the-money call is at risk of exercise, in which case shares will be given up at the strike. Collateral is required equal to 20 percent of the strike value, minus premium received for selling the put. This is advantageous leverage when compared to the covered call. No collateral is required for a covered call. However, to buy 100 shares of the underlying, 50 percent must be paid, and the remaining 50 percent is bought on margin. The timing for opening a naked put is essential to reduce exposure to unwanted exercise. The best position for a naked put is when the underlying price moves through support and you expect price to retrace back into range. For example, the chart for Amazon.com (AMZN) shows examples of when this occurred. The highlighted price moves both fell below the trendline shown on the chart. Given the long-term bullish trend for AMZN, it was reasonable to expect the price to reverse to the upside. This is what occurred in both instances. A second consideration is creation of a buffer zone between current price per share and the selected strike for the short put. Because AMZN is a high-priced stock, the opportunities for buffer zones are significant. For example, after the huge decline in February from nearly $1,500 per share down to 21,350 by February 6, anticipating a rebound would be well-timed. During the trading day of February 8 and about 30 minutes into the session,AMZN was trading at $1,416.36 per share. A couple of naked put trades to consider at that moment: The 1,410 put expiring in one day (Feb. 9) was at a bid of 10.05. This is incredibly rich considering the one-day expiration. The strike was six points below current price. That, plus the net $1,000 for selling the put, sets up a buffer zone of 16 points. The 1,362.50 put expiring in eight days (Feb. 16) showed a bid price of 13.05. This is 54 points below current price. Adding the 13 points received for selling the put, this creates a 67-point buffer zone over an exposure period of eight days. Time decay will be rapid. Typically, options expiring in one week lose 34% of their remaining time value between Friday and Monday. In this example, that spans February 9 to 12 – three calendar days but only one trading day. The timing and buffer zone are the two keys to a successful short put strategy. Whether you select extremely short-term (one day) or a little longer (eight days), the profit potential is attractive, in large part due to the recent volatility in the market and in AMZN, which fell 150 points in two days. The extreme move in price makes the point that timing is everything with this strategy. The likely bargain hunting at such a low price makes an upward move likely. By February 8, price had always moved from the low of $1,350 to $1,416, recovery of 66 points out of the 150 points previously lost. As with all options strategies, especially those involving a short position, this one has to be monitored every day. Because things change rapidly in volatile markets, you need to get out when you can to maximize profits or, in worst case situations, to mitigate losses. The need for a buffer zone and attractive premium levels makes the naked put a potentially profitable strategy, even for the conservative trader. Michael C. Thomsett is a widely published author with over 80 business and investing books, including the best-selling Getting Started in Options, coming out in its 10th edition later this year. He also wrote the recently released The Mathematics of Options. Thomsett is a frequent speaker at trade shows and blogs on his website at Thomsett Publishing as well as on Seeking Alpha, LinkedIn, Twitter and Facebook.1 point -

This infographic has been designed to make it easier for you to understand option trading.1 point

This infographic has been designed to make it easier for you to understand option trading.1 point

This leaderboard is set to New York/GMT-04:00