First of all, as a general comment, there is no such thing as guaranteed returns in the stock market. If there was, everyone who is trading the stock market would be a millionaire.

The proposed trade is called a long straddle option.

A long straddle option strategy is vega positive, gamma positive and theta negative trade. That means that all other factors equal, the option straddle will lose money every day due to the time decay, and the loss will accelerate as we get closer to expiration. For the straddle to make money, one of the two things (or both) has to happen:

1. The stock has to move (no matter which direction).

2. The IV (Implied Volatility) has to increase.

In simple terms, Implied Volatility is the amount of stock price fluctuations. Being on the right side of implied volatility changes can enhance the chances of success.

The problem with the proposed setup is that you are not the only one who knows about the event - it’s a public knowledge, so market participants bid the options prices in anticipation of the event, driving IV to higher than usual levels. After the event the IV usually collapses. If the stock moves more than “implied” by the straddle price, then the straddle will be a winner. BUT more often than not, the options prices overprice the potential move, and when the stock moves less than expected, collapsed IV will make the straddle a loser.

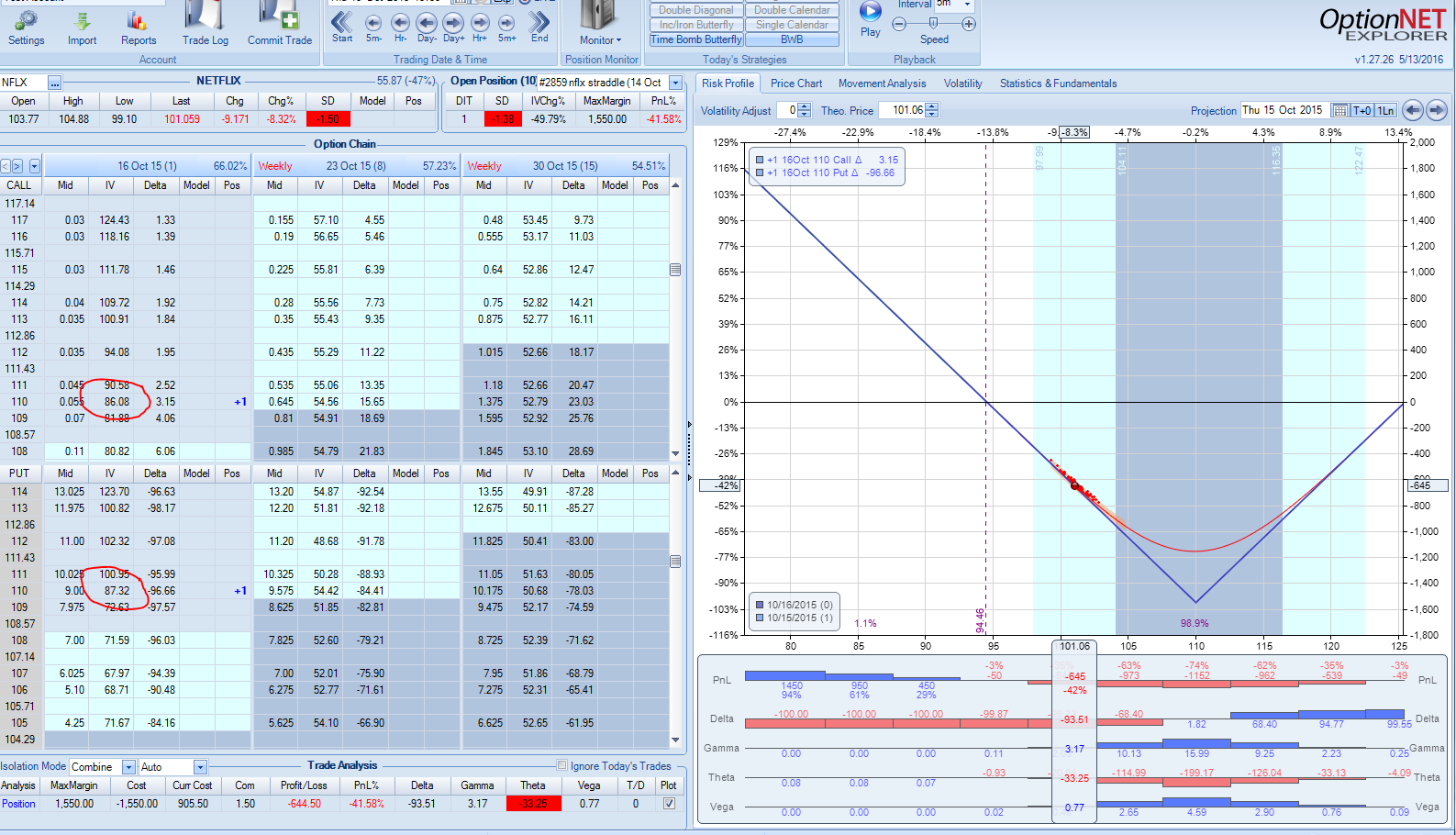

Example:

NFLX was scheduled to report earnings on October 15, 2015. The stock was trading around $110, and 110 straddle around 15.50. This price "implied" $15.50 move. The following image presents the P/L chart of the trade:

As we can see, the IV is around 240% for those options, reflecting the upcoming event.

Fast forward 24 hours: the stock moved $9 which is a substantial move, but less than "implied" by the options prices. This is the P/L chart:

As we can see, IV collapsed to ~85%, and the trade has lost 42%.

At SteadyOptions, we trade straddles in a different way. We usually buy a straddle around 7-10 days before the event and sell it 1-2 days before the event when IV peaks. This setup can benefit from the stock moving and/or IV increase.

Related articles:

How We Trade Straddle Option Strategy

Buying Premium Prior to Earnings

Can We Profit From Volatility Expansion into Earnings

Understanding Implied Volatility

How We Made 23% On $QIHU Straddle In 4 Hours

Want to learn more?

There are no comments to display.

Join the conversation

You can post now and register later. If you have an account, sign in now to post with your account.

Note: Your post will require moderator approval before it will be visible.