The VIX, also known as the fear index, has skyrocketed from around 12 in late 2019 to a high of 85 in early March. At the time of writing, the VIX has reduced to about 60, which shows stress coming out of the market as governments scramble to introduce stimulus packages to support economies and their citizens.

Of course, our priority is health, safety, and solidarity in our communities to support each other, not to take advantage of the markets. But, as traders, I am also sure that many of you are spending extra energy to survive and maybe even profit off these exceptional times and exceptional market conditions.

In this article, I will introduce one spread for “Discount Stock Shopping” in extremely turbulent markets. I will also share two live trades that I am engaged in as examples to highlight the pros and cons of this strategy.

This article assumes you are at least an intermediate options trader. I've emphasized the analysis of two live examples rather than investing time in reviewing the basics.

The "Talking Heads" Typical Responses to Extreme Volatility

During such extreme times, traders/investors tend to herd into the following approaches, advocated by the talking heads on cable TV:

- Increasing cash holdings,

- Short the general market / hard hit securities,

- or Buy up ‘discounted’ quality companies.

These are natural responses to extreme volatility, but a bit unimaginative for us options traders. Don’t get me wrong, each has some validity in the current market, but each comes with some substantial trade-offs as well.

Heard Option 1: Increase Cash

Increasing cash holdings provides the most safety and certainly helps weather the storm. Still, unless executed early, bullish investors have likely already given up profits (at best) or are already sitting on massive drawdowns (at worst). Going to cash certainly provides safety in times of uncertainty. Still, we must recognize that going into cash is tough at times and doesn’t allow the trader to participate in any recovery without a delicately timed re-entry. At worst, it solidifies drawdowns to real losses.

Heard Option 2: Shorting the Market / Impacted Companies

Shorting the markets is a step further of the "going from long to cash." Of course, we can profit as markets fall, but this exposes the trader to short squeezes, government interventions, and unlimited theoretical losses when the market recovers. I don’t mean to open a debate on the direction of the market, but experienced traders know that going short is coupled with strong headwinds as the governments' interest is to mitigate damage to markets. We’ve seen $2 trillion already.

Sophisticated traders, like you, may think that long puts and put spreads may be the answer to minimize these risks when expressing a bearish view. However, the high volatility and the high VIX the cost of these long puts are at levels that are very difficult to profit.

Heard Option 3: Buying Up Discounted Quality Companies

The perpetual-bulls and long-term investors look at previous crashes and realize that significant gains can eventually be realized by purchasing quality companies on the cheap. Remember that a 50% drop is a 100% return if the company can appreciate back to previous levels.

History tells us that this is a great strategy, but again, very hard to time entries and also requires an iron stomach if we experience additional turbulence.

A Hybrid Response Using Options

As introduced, this article will present one of my favorite options trading strategies that I believe is well suited for this market environment and begs your consideration.

It is essentially a hybrid response of Option 2 (shorting) and Option 3 (buying up discounted stocks).

You might ask yourself how it’s possible to simultaneously ‘short’ and ‘go long’?

I’ll explain, but before I introduce the strategy, let me highlight the key benefits of this setup.

Key Benefits:

-

Profits if the underlying stock/ETF continues to sell-off

-

Allows the trader to set a planned, lower cost basis on the underlying before going long.

-

Takes advantage of high volatility as we'll sell more options than we purchase.

-

The spread will profit when volatility returns to previous averages.

-

The spread expresses a short-term bearish view without the risk of short-squeezes or big up days.

-

A simple spread that's very easy to adjust

Remember, as I say in all my articles, there is no free lunch in trading. If you think you’ve found it, please do yourself a favor by taking a cold shower and re-assessing where the inevitable risks are. You’ve missed something or the person teaching you the strategy is misleading you.

Key Risks / Downsides:

-

A sell-off is required by the underlying to acquire the stock. It’s possible to "miss" getting long and, therefore, presents an opportunity cost on any near-term "big" up days.

-

Exposes the account to drawdown if volatility increases.

-

Assignment of stock at lower prices, although we only use this strategy as a replacement for buying the stock outright.

-

Easy to get ‘carried away’ and break the discipline required for such a strategy. Never increase your net-short position size larger than the shares you’d like to purchase. Bankruptcy risk must be kept in mind.

OK, enough of the introduction, let’s get to the spread itself.

The Put Front Ratio Spread

Perhaps you guessed from the introduction that I was referring to a Put Front Ratio Spread.

Let’s briefly review the setup:

-

Buy 1 Put ATM or ITM (Strike A)

-

Sell 2 Puts further OTM (Strike B)

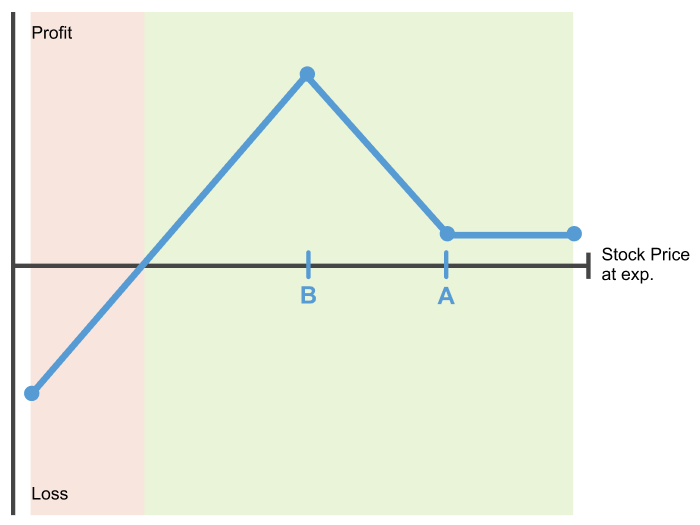

Let’s take a look at the Risk Plot to understand the structure.

A few observations from the P/L diagram above:

-

The current stock price should be at or above Strike A. Staying ATM or ITM gives you the best price (i.e., lowest implied volatility) on your put purchase.

-

Strike B (further OTM) should be out of the money (higher implied volatility) but balanced between down-side protection (DSP) and the overall credit received.

-

The structure is essentially a long Put Vertical (A-B) with an extra Short Put B to finance the long Vertical Put Spread.

-

We only put it on for a credit, that way we still profit if the stock appreciates although we miss the opportunity of holding the stock outright. Remember, we only use this strategy when we want to be assigned the stock.

-

You are obligated to buy shares at Strike B at expiration, so size the position for how much of the stock you want to buy at expiration (as if you were planning to go long). If you’re more bearish in the short term, consider half of the position size (more on this later).

-

Because this is a ratio spread, you will see multiples of 1/-2, but you are only short (cash-secured) the ‘extra’ short put. For example, if you put on 10 long puts / 20 short puts, you are only exposed to the 10 extra short puts or 1000 long shares if assigned.

Real Examples from Active Front-Put Ratio Trades

An example speaks a thousand words and will hopefully highlight the thinking and use of this strategy for “discount stock shopping” in very turbulent markets.

A few disclaimers:

-

I am actively in these positions, although I haven't given my actual position sizing. I gave the trades as examples, not as recommendations, nor am I trying to influence you to enter the same position. Markets have already moved, so it would be silly to enter the same trades.

-

I placed these trades on the 19th of March, which means I have the benefit/bias of hindsight when discussing their entry. I've made the best efforts to be transparent, but time can affect your memory.

-

I am one of the co-founders of OptionAutomator. While I usually leverage our options screener for advanced analysis/trade ranking, Front-Ratios are currently in active development and not yet available, so I relied solely on my judgment and readily available options analysis. I.e., no special tools or analysis required.

-

The trades are an expression of my personal market views, not an endorsement, recommendation, nor invitation for debate on the underlyings.

Exxon Mobil (XOM) Put Front Ratio, Entered Mar 19th, 2020

Underlying Considerations:

COVID-19 decreasing transportation demand coupled with a pricing war between Russia and Saudi Arabia has hit the energy industry hard. I like XOM long-term for a sector recovery and wanted to get long the stock but expected more downside.

XOM also pays a dividend, which has increased for 37 consecutive years, that’s through multiple oil crashes and macro market crashes, including 2008/2009.

Important to note that all individual company dividends are at risk, but I was comfortable with that risk considering past performance. XOM pays out $3.48 per year, and at Mar 19th pricing (c.a. $34/share), that equated to a yield of approximately 10%.

Entry:

I want the shares on XOM, so I was more bullish in my setup and went further ITM.

@ Underlying Price c.a. $34/share

-

Bought 1x APR 17 40 Put @ $7.76

-

Sold 2x APR 17 35 Put @ $4.68

----------------------------------------------

-

Net Credit: $1.60

-

Max Return: $6.60

-

Max Loss (bankruptcy): $28.40

-

Current Price: March 30th, I could exit for $0.44, or $1.16 net profit.

Short Assignment Risk: @$35/share

I was happy with the assignment risk in this position as I wanted the shares (have I stressed that enough in this article??!). This heavily influenced my strike selection for this trade and in stark contrast to the next example. I wanted the short contracts close to the current trading price to maximize the chance of assignment while adhering to advantages of in/out of the money implied volatilities (IV).

Break-Even: $28.40/share

The break-even in this trade offers 16.5% downside protection (DSP) on high-quality stock. In fact, at a cost basis equal to my break-even is equivalent to 12.25% yield on the shares assigned.

Adjustment Strategy: None.

I want the shares and looking to be assigned. I also took a more significant credit on this one vs. expanding out the width of the spread (by selling a lower strike) as I wanted small participation on any immediate upside.

Adjustment to Take Risk Off: Possible; However, not in the trading plan.

One benefit of ratios is the ease in adjusting them. If you see a quick run-up in the stock as we have over the past weeks, you can look to convert the ratio into a butterfly spread. You do that by submitting a Good-unTil-Cancelled (GTC) buy on another put equal width from the short contracts. In this example, that would be purchasing the 30 put.

So long as you purchase the put for less money than the credit received, you still participate for a big payout if prices run to the short put's strike price but have no additional risk in the spread. Your margin required should also decrease to $0.

E.g., using today’s pre-market prices: Use $0.60 of the $1.60 received at trade entry to put in a standing order for 1x APR 30 Put. If filled, you then have a 40/35/30 Put Butterfly with a minimum profit of $1 and a maximum profit of $6. There is no risk left in the trade at this point.

I’m not looking to do this in this particular position, but it’s an option if you want to take off risk/free up margin.

Delta Airlines (DAL) Put Front Ratio, Entered Mar 19th, 2020

Underlying Considerations:

COVID-19 has put the airline stocks in the spotlight. In March, U.S. President Trump was speaking on potential bailouts/stimulus to support the U.S. airline industry, among others. My opinion was that a safety net was necessary and inevitable, but realized this underlying was riskier than others and could be very painful to get long at current prices. The options markets were certainly pricing in the bankruptcy risk.

Entry:

I want to trade around DAL and am generally less interested in owning it long-term, as I think the dividend is likely to be canceled, but still happy to hold in the short-term.

That said, you might be thinking that I’m breaking my own rule. Well, yes and no. Yes, that I’m not necessarily stock shopping on Delta as I mostly hold dividend stocks. No, in that I would be happy to take shares at the break-even below, but would most likely keep it in an options position with active management.

@ Underlying Price c.a. $21.50/share

-

Bought 1x Apr 17 22 Put @ $6.25

-

Sold 2x Apr 17 15 Put @ $3.33

----------------------------------------------

-

Net Credit: $0.41

-

Max Return: $7.41

-

Max Loss (bankruptcy): $7.59

-

Current Price: March 30th the position could be closed for $0.44

Short Assignment Risk: @$15/share

The short assignment risk on Delta is at $15/share, but I have additional protection due to the long Put Vertical embedded in the setup. I will highlight the meager break-even price in the next section.

I will have a choice if the underlying breaks the $15/share barrier. Either take the shares and sell them right away or hold them or just roll out the put (simultaneously purchase the 15 Put and sell the 15 put or lower in the following month until it expires worthless). Note that rolling out the put is similar to being long the shares from a risk perspective.

Break-Even: $7.59/share

Wow. Let’s just think about that for a second. That’s 65% downside protection.

Such a break-even just shows how much fear was priced into the DAL options market when entering that trade. Could you imagine in Dec 2019 when Delta was around $60/share that the market would provide an opportunity to make significant money on Delta so long as the price remains above $7.60 per share?

I’m not discounting the bankruptcy risk, as I addressed in the qualitative analysis of the underlying, but if the market is willing to pay these types of premiums, then I’m ready to sell them.

Adjustment Strategy: Roll Down and Out

I entered this position at about 50% of the size I wanted to trade. My position sizing was necessary, as I planned to double the original position size in the event of future blood on the streets, but I remain true to my conviction on a safety net. Going in at 50% size also has the benefit of being able to walk away with only half the losses if my conviction changes due to updates on the policy.

If the 15 strike puts were tested or blown past, I planned to roll down and out, i.e.:

-

buy 1x APR 15 put and

-

sell 1x MAY put at the lowest strike possible for even money – likely around 14/13 strike, while

-

simultaneous entering another front ratio spread in May at one strike below short put in #2.

It’s hard to estimate pricing in May. Still, if we reached such low prices, DAL volatility would likely explode, which I would use to significantly increase my downside protection in the following month by executing the additional ratio.

I saw this with Citigroup in 2009; the options on C were so inefficient that I remember looking at ratio spreads that had break-evens in cents/share vs. dollars/share.

Conclusion and Parting Words

Thank you for reading, and I hope this gives you a tool to consider for your trading quiver in these turbulent times.

Besides welcoming your comments/questions, which I will respond to, I would like to part with a few final takeaways on the risk of this approach.

-

This position has less risk than going long stock outright, but only if you have the complete discipline to manage your trade sizing to a maximum of the buy-and-hold position, you would alternatively enter.

-

Adjustment techniques described require even more discipline. Never adjust or double the risk in the strategy unless you entered at half size to leave open this alternative.

-

Do be careful in this environment and mind overall portfolio management, don’t go too big and be sure to leave cash aside, so you don’t run out of levers.

Drew Hilleshiem is the Co-Founder and CEO of OptionAutomator, an options trading technology startup offering a free options screener that leverages Multi-Criteria Decision Making (MCDM) algorithms to force-rank relevancy of daily options opportunities against user’s individual trading criteria. He is passionate to help close the gap between Wall Street and Main Street with both technology and blogging. You can follow Drew via @OptionAutomator on Twitter.

There are no comments to display.

Join the conversation

You can post now and register later. If you have an account, sign in now to post with your account.

Note: Your post will require moderator approval before it will be visible.