Leaderboard

Popular Content

Showing content with the highest reputation on 08/03/18 in all areas

-

Congrats on almost one year! @Djtux is a valuable member here and provides a great service which only continues to improve. Well worth it for SteadyOptions style trades. Not a paid endorsement, but I like to support good work .2 points

-

It's almost the 1 year anniversary of the launch of the website. For anyone on the fence, i would encourage you to subscribe now to lock in the current price as i'm considering increasing it. I have some backend work to do on the payment system to be able to do that, but it's coming at some point. For existing subscribers, as long as you keep your subscription, nothing will change and thank you for the support.2 points

-

The main benefit of this chart is to show potential calendar spread gains over time - if the stock price stays near our strike. We KNOW that the front leg (expiring prior to earnings) is going to decline steadily which means the calendar RV chart will slope upward - so its not like our pre-earnings calendars where we compare RV, the important thing here is seeing the slope of the increase (unless, of course, something is way off from the average). That being the case, for the pre-pre-earnings analysis, its not a big deal if the monthly spreads have some 5 week and some 4 week calendars. I've been thinking about some general guideline for a trade like this: Open 6-8 weeks prior to short leg expiration. Look for stocks that show a tendency not to move too much between earnings periods (look at charts or do backtests). Look to close about 4 weeks prior to short expiration (no less than 3). From our hedged straddle experience we know that gamma can really accelerate on the short leg the closer you get to expiration so for a trade like this we want to be out before that happens - this is a bit counter-intuitive because the last 4 weeks is when the RV really starts to shoot upwards, but its also the timeframe where the spread becomes more sensitive to stock price movement and the profit tent narrows. Given these entry/exit timeframes use the pre-pre-earnings RV charts to show likely gain percentages if the stock price cooperates.2 points

-

It immediately became clear this could be used, not only for put selling testing, but to test Anchor over longer periods of time than previously done and try to find other areas to improve the strategy, which has been a core part of SteadyOptions for quite some time. After two weeks of testing, much of what Anchor has evolved to over the past few years was validated, but we also identified some areas for improvement that should increase performance of the strategy. In this article, and a future one next week, I will discuss the conclusions from our expanded optimization, back testing, and review. Later articles will dive into the implications for the leveraged versions of the Anchor Strategy, as well as the benefits of expanding Anchor by diversifying into IWM, QQQ, DIA, and potentially other indexes. I. Selling Calls for Credit Anyone who has been following Anchor recently knows we have been on a quest to find other ways to pay for the hedge. The biggest drag on the strategy is the hedge, and any way we can improve paying for the hedge cost helps. In this decade long bull market, paying for the hedge has been particularly problematic, more so in recent years. For the past few months, we’ve been structuring and testing a variety of call selling strategies in an effort to extract a few more basis points of performance out of Anchor. Initial paper trading had us optimistic, as well as the manual testing done over the previous nine months. Further, the CBOE maintains covered call indexes, which seemed to indicate that the strategy should work. We were optimistic enough to start tracking it on the forums in the leveraged anchor accounts. What a thorough back testing demonstrated was that selling naked calls on indexes, SPY in particular, is a losing strategy, or at best a breakeven one, since 2007. This is true over shorter periods of time as well, such as since 2012. If calls, three weeks and one standard deviation out are used, since 2012, the strategy would have lost a 1.6% per year. If data from 2007 is used, so as to capture 2008 and 2009, the strategy still would have lost 0.20% per year. Trying further out in time over periods such as 28 days, 45 days, or 60 days were all losers. What about putting in stop losses or profit targets – also all losers. In fact, only through extreme curve fitting, was I able to identify any possible profitable naked call selling strategy at all, and only if you use the data set from 2007 to the present – even then performance would only have gone to 0.55% per year. Then if you remove 2008 from the data set, results immediately went back to negative performance. Changing from an at the money position, to a 30 delta position did not help much either. Since 2007, selling a 30 delta one month call, would have netted you only 0.22% per year – essentially flat. Changing the delta to 10 or 60 did not help either. This result was initially puzzling, as the covered call index (BXM) is up over 50% over the last five years and 75% over the last ten – until those results are broken down. BXM is not naked call selling, it is covered call selling. Given over the last five years, the S&P 500 is up about 75%, which means call selling is responsible for 25%, or more, of BXM’s losses. If covered call selling was profitable, there would not be this drag. By eliminating the gains from the long stock positions, the returns go to negative – as indicated by our testing. The conclusion? Simple Anchor will not be selling calls as a way to gain additional income to help cover the cost of the hedge and such strategies will be removed from the leveraged versions of Anchor. II. 14 vs. 21 vs. 28 Days for the Short Puts A few years ago, we switched from selling puts either one or two weeks out to three weeks till expiration. Doing so gives the strategy more time to “be patient” in the event of small market moves down and not realize losses that did not have to be realized simply due to normal market fluctuations. When making the selection on how many days “was optimal” we used the past 18 months of actual Anchor data for back testing purposes. ORATS confirmed that over that 18 month period, 21 days was the optimal time to use. However, with more data at hand, we have been able to confirm that 28 days is a significantly better time period over history than a 21 day period. In testing, we used two data sets on SPY – from January 2012 to present and from January 2007 to present. January 2012 was picked because after that point, SPY weeklies were fully available. January 2007 was picked because that’s the furthest back in time the software’s data went. From January 2012 to the present, selling puts 21 days out, with a profit target of 30%, would have returned, on average, 8.87% per year with a Sharpe Ratio of 1.63. From 2007, a return of 5.32% was realized with a Sharpe Ratio of 0.42. Merely by increasing from 21 days to 28 days, those numbers increase to 11.08% and 2.14 for 2012 to the present and 8.52% and 0.93 for 2007 to the present. This is a massive increase. It was enough of an increase to make us question the results. If this was a more “optimum” period, as theorized, such results should hold across other, similar instruments. For both QQQ and IWM, the results held. 28 days achieved much better returns on a put selling period than 21. We also learned that rolling the short puts on a set day (Friday), anytime you can for a gain, is not close to an optimal roll period. Significant improvements can be gained by ensuring the profits are somewhere between 25%-35% prior to rolling. Interestingly, waiting till profits are in excess of 50% began to have a negative impact on results. (Profits are defined as a percentage of credit received. So if we receive $1.00 for selling a put, a thirty percent gain would occur when the price declined to $0.70) Anchor’s current put selling strategy has us making an adjustment each Friday. If there’s a gain in the position, we roll, and if not, we hold – simple rules. Unfortunately, by adhering to “simpler” rules in an effort to make the strategy easier to manage for everyone, we cost ourselves significant performance. If we rolled when a profit target was reached, regardless of day, as opposed to on a Friday at any profit point, we would have increased our returns to 11.08% and Sharpe Ratio to 2.14 from the 6.87% return and 0.7 Sharpe Ratio we have experienced since 2012 on put selling. Using the same put selling ratio we have, that means by doing Friday roles, instead of a profit target, we’ve cost ourselves between 1.5% to 2.0% per year in total performance. III. Cautionary Notes One thing to be careful with software such as ORATS is over mining and getting confused by the noise. For instance, why not pick 25% or 33% profit target instead of 30%? Once you get that granular, randomness becomes a factor. One year 25% might work significantly better and another 33% and yet another 30%. Given that there are only 12-24 trades per year, which profit target hit on that tight of a range is a bit of “luck.” For instance, if we sold a put for $1.80, a 25% profit would have the price dropping to $1.35 and at 33%, $1.21. Prices move that much intraday frequently, so trying to target the “exact” price to do everything is a fool’s errand. The inability and/or inaccuracy in trying to overly optimize is a concern in getting exact performance numbers. It is not a concern in identifying major trends. If profit targets between 1%-20% all underperform profit targets from 25%-35%, over multiple periods, clearly we should be using 25%-35%. Similarly if all results are worse over 50%, then 50% is too high. Using different instruments (IWN and QQQ) provided further verification for this process, providing a higher degree of confidence. There is also a concern that any back testing is simply “curve fitting,” and that is one hundred percent true. The data we have discussed is pulling out the optimal curve. Some of this can be combated by using different time periods (e.g. 2007 to present and 2012 to present, or even smaller periods). If the conclusions founds hold over various time periods and various instruments (QQQ and IWM), it is more likely than not that the results are not merely curve fit, but instead due to consistent trends. However, as we all know, previous results are no guarantee of future performance – they merely increase our chances. In verifying our hypothesis about 28 days and profit target rolling, we went even more granular, across SPY, QQQ, and IWM. To our relief, the results generally stood. 28 day periods are more optimal than 7, 14, 21, 35 or 45 over the vast majority of time periods. There are years “here and there” were 21 days were better and one year on IWM were 35 days was a better period. But even in those years, 28 days was the second best performing. Over any multiple year period (from 2007 to the present), our conclusions held. The same held true for profit margins. Maybe one year 20% was the best and another 45% the best, but in all multi-year periods we looked at, using a profit margin of “around” 30% was much better than a static day roll with no profit margin requirement. Because of this, starting this Friday, we will be modifying Anchor’s rolling rules. Moving forward, we will be rolling to 28 days out and rolling once profits have gotten above 30%. This means we may be rolling on days other than Friday moving forward if profit targets are obtained. We could even roll several days in a row in a bull market. If profit targets are not hit, we will continue to hold, as the strategy currently operates. Next week we’ll discuss other Anchor modifications we will be implementing to ideally further improve Anchor’s average performance.1 point

It immediately became clear this could be used, not only for put selling testing, but to test Anchor over longer periods of time than previously done and try to find other areas to improve the strategy, which has been a core part of SteadyOptions for quite some time. After two weeks of testing, much of what Anchor has evolved to over the past few years was validated, but we also identified some areas for improvement that should increase performance of the strategy. In this article, and a future one next week, I will discuss the conclusions from our expanded optimization, back testing, and review. Later articles will dive into the implications for the leveraged versions of the Anchor Strategy, as well as the benefits of expanding Anchor by diversifying into IWM, QQQ, DIA, and potentially other indexes. I. Selling Calls for Credit Anyone who has been following Anchor recently knows we have been on a quest to find other ways to pay for the hedge. The biggest drag on the strategy is the hedge, and any way we can improve paying for the hedge cost helps. In this decade long bull market, paying for the hedge has been particularly problematic, more so in recent years. For the past few months, we’ve been structuring and testing a variety of call selling strategies in an effort to extract a few more basis points of performance out of Anchor. Initial paper trading had us optimistic, as well as the manual testing done over the previous nine months. Further, the CBOE maintains covered call indexes, which seemed to indicate that the strategy should work. We were optimistic enough to start tracking it on the forums in the leveraged anchor accounts. What a thorough back testing demonstrated was that selling naked calls on indexes, SPY in particular, is a losing strategy, or at best a breakeven one, since 2007. This is true over shorter periods of time as well, such as since 2012. If calls, three weeks and one standard deviation out are used, since 2012, the strategy would have lost a 1.6% per year. If data from 2007 is used, so as to capture 2008 and 2009, the strategy still would have lost 0.20% per year. Trying further out in time over periods such as 28 days, 45 days, or 60 days were all losers. What about putting in stop losses or profit targets – also all losers. In fact, only through extreme curve fitting, was I able to identify any possible profitable naked call selling strategy at all, and only if you use the data set from 2007 to the present – even then performance would only have gone to 0.55% per year. Then if you remove 2008 from the data set, results immediately went back to negative performance. Changing from an at the money position, to a 30 delta position did not help much either. Since 2007, selling a 30 delta one month call, would have netted you only 0.22% per year – essentially flat. Changing the delta to 10 or 60 did not help either. This result was initially puzzling, as the covered call index (BXM) is up over 50% over the last five years and 75% over the last ten – until those results are broken down. BXM is not naked call selling, it is covered call selling. Given over the last five years, the S&P 500 is up about 75%, which means call selling is responsible for 25%, or more, of BXM’s losses. If covered call selling was profitable, there would not be this drag. By eliminating the gains from the long stock positions, the returns go to negative – as indicated by our testing. The conclusion? Simple Anchor will not be selling calls as a way to gain additional income to help cover the cost of the hedge and such strategies will be removed from the leveraged versions of Anchor. II. 14 vs. 21 vs. 28 Days for the Short Puts A few years ago, we switched from selling puts either one or two weeks out to three weeks till expiration. Doing so gives the strategy more time to “be patient” in the event of small market moves down and not realize losses that did not have to be realized simply due to normal market fluctuations. When making the selection on how many days “was optimal” we used the past 18 months of actual Anchor data for back testing purposes. ORATS confirmed that over that 18 month period, 21 days was the optimal time to use. However, with more data at hand, we have been able to confirm that 28 days is a significantly better time period over history than a 21 day period. In testing, we used two data sets on SPY – from January 2012 to present and from January 2007 to present. January 2012 was picked because after that point, SPY weeklies were fully available. January 2007 was picked because that’s the furthest back in time the software’s data went. From January 2012 to the present, selling puts 21 days out, with a profit target of 30%, would have returned, on average, 8.87% per year with a Sharpe Ratio of 1.63. From 2007, a return of 5.32% was realized with a Sharpe Ratio of 0.42. Merely by increasing from 21 days to 28 days, those numbers increase to 11.08% and 2.14 for 2012 to the present and 8.52% and 0.93 for 2007 to the present. This is a massive increase. It was enough of an increase to make us question the results. If this was a more “optimum” period, as theorized, such results should hold across other, similar instruments. For both QQQ and IWM, the results held. 28 days achieved much better returns on a put selling period than 21. We also learned that rolling the short puts on a set day (Friday), anytime you can for a gain, is not close to an optimal roll period. Significant improvements can be gained by ensuring the profits are somewhere between 25%-35% prior to rolling. Interestingly, waiting till profits are in excess of 50% began to have a negative impact on results. (Profits are defined as a percentage of credit received. So if we receive $1.00 for selling a put, a thirty percent gain would occur when the price declined to $0.70) Anchor’s current put selling strategy has us making an adjustment each Friday. If there’s a gain in the position, we roll, and if not, we hold – simple rules. Unfortunately, by adhering to “simpler” rules in an effort to make the strategy easier to manage for everyone, we cost ourselves significant performance. If we rolled when a profit target was reached, regardless of day, as opposed to on a Friday at any profit point, we would have increased our returns to 11.08% and Sharpe Ratio to 2.14 from the 6.87% return and 0.7 Sharpe Ratio we have experienced since 2012 on put selling. Using the same put selling ratio we have, that means by doing Friday roles, instead of a profit target, we’ve cost ourselves between 1.5% to 2.0% per year in total performance. III. Cautionary Notes One thing to be careful with software such as ORATS is over mining and getting confused by the noise. For instance, why not pick 25% or 33% profit target instead of 30%? Once you get that granular, randomness becomes a factor. One year 25% might work significantly better and another 33% and yet another 30%. Given that there are only 12-24 trades per year, which profit target hit on that tight of a range is a bit of “luck.” For instance, if we sold a put for $1.80, a 25% profit would have the price dropping to $1.35 and at 33%, $1.21. Prices move that much intraday frequently, so trying to target the “exact” price to do everything is a fool’s errand. The inability and/or inaccuracy in trying to overly optimize is a concern in getting exact performance numbers. It is not a concern in identifying major trends. If profit targets between 1%-20% all underperform profit targets from 25%-35%, over multiple periods, clearly we should be using 25%-35%. Similarly if all results are worse over 50%, then 50% is too high. Using different instruments (IWN and QQQ) provided further verification for this process, providing a higher degree of confidence. There is also a concern that any back testing is simply “curve fitting,” and that is one hundred percent true. The data we have discussed is pulling out the optimal curve. Some of this can be combated by using different time periods (e.g. 2007 to present and 2012 to present, or even smaller periods). If the conclusions founds hold over various time periods and various instruments (QQQ and IWM), it is more likely than not that the results are not merely curve fit, but instead due to consistent trends. However, as we all know, previous results are no guarantee of future performance – they merely increase our chances. In verifying our hypothesis about 28 days and profit target rolling, we went even more granular, across SPY, QQQ, and IWM. To our relief, the results generally stood. 28 day periods are more optimal than 7, 14, 21, 35 or 45 over the vast majority of time periods. There are years “here and there” were 21 days were better and one year on IWM were 35 days was a better period. But even in those years, 28 days was the second best performing. Over any multiple year period (from 2007 to the present), our conclusions held. The same held true for profit margins. Maybe one year 20% was the best and another 45% the best, but in all multi-year periods we looked at, using a profit margin of “around” 30% was much better than a static day roll with no profit margin requirement. Because of this, starting this Friday, we will be modifying Anchor’s rolling rules. Moving forward, we will be rolling to 28 days out and rolling once profits have gotten above 30%. This means we may be rolling on days other than Friday moving forward if profit targets are obtained. We could even roll several days in a row in a bull market. If profit targets are not hit, we will continue to hold, as the strategy currently operates. Next week we’ll discuss other Anchor modifications we will be implementing to ideally further improve Anchor’s average performance.1 point -

I'm with you on that!1 point

-

Yes, I see them on Tradehawk1 point

-

Those are good guidelines. I too, was looking to enter around the same time you mentioned, and exit well before heavy gamma kicks in. As far as underlying movement, we can look at the history of relative price move% to get some idea of how much tendency the underlying has moved in the past, during this specific time frame, to see if there are any repeating patterns, As far as the loss of value, on the short expiration, I think people tend to look in the wrong place for this. There is a big difference between the rate at which an option deteriorates, and the amount of premium an option loses. Most option sellers like to focus on the last 30 DTE, because time decay is the greatest. But, the gamma risk, associated with that is the highest. The thing that many people are missing, is that while an option may deteriorate at the fastest rate, during the last 30 DTE, it is not losing the most amount of it's value during that time. There is a period between 75 DTE- 50 DTE, ( it is hard to pinpoint the exact spot, but generally), where a 10 delta option will lose 50% of it's value, and not have much gamma risk associated with it that far away. An option is "born" with x amount of premium. By the the time it reaches T-30, it has already lost 90% of that premium. So, it is losing it's last 10% at the fastest rate of decline, with the most amount of gamma. So, this is sort of the worst spot to focus on for an option seller. Also, with regard to these 2 different calendar strategies, while a "normal" calendar, is a "long IV" position, one can make a case that a "pre earnings calendar" can be a short IV position. Look at the case where the long and short IV starts out at 45 and 43, and winds up at 95 and 50 IV....This does happen in some cases, and while the value of 1 vega is much greater, in the longer dated expiration, sometimes the front expiry IV gain is even greater than that. But, during non earnings times, a calendar is a long IV position. What is good about this trade is that the leg that you are long, is the first expiration post earnings. This is the expiry where, eventually most of the money will flow into, and will reach the highest IV of all expirations. This may not happen during the time frame of this trade, but the long leg will have a degree of "IV support".1 point

-

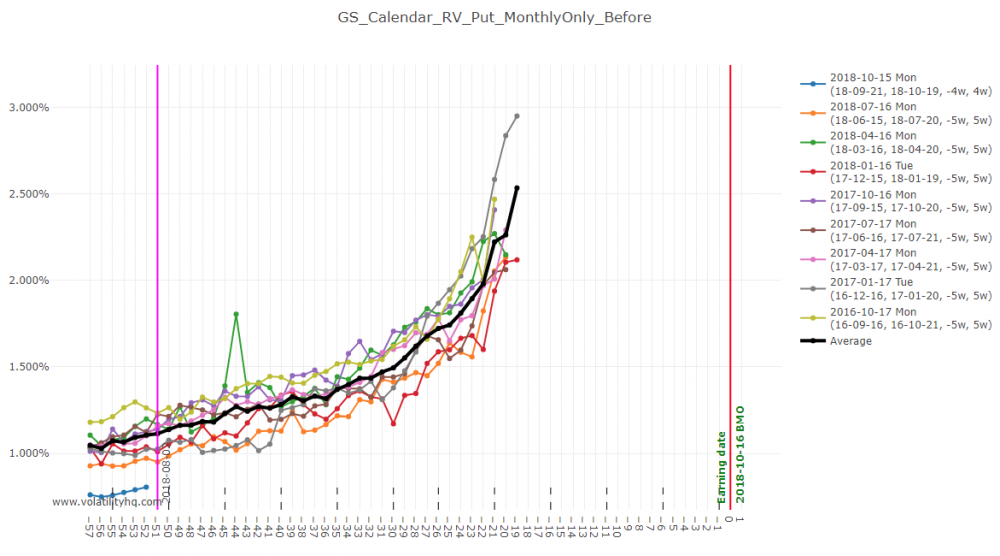

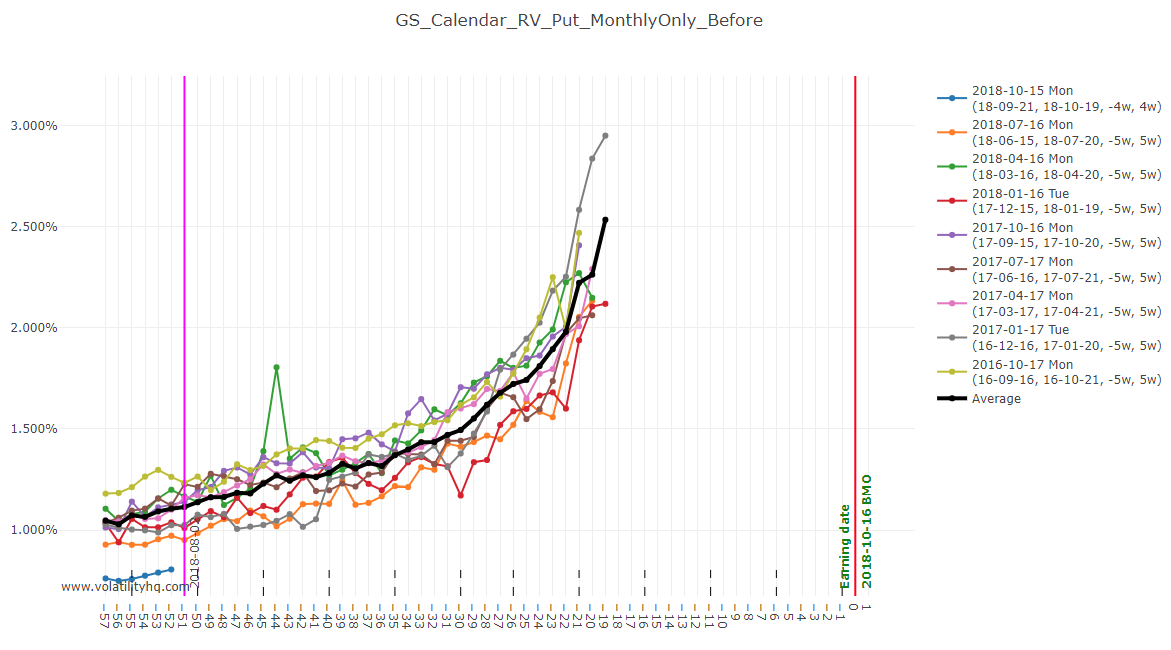

I just added a new option on the Calendar RV page to support a 'pre-pre earnings' calendar. The short leg expires before the earnings date. That feature is in beta for now as i have not done extensive testing yet, and is slower than the rest of the functionalities because i have not implemented that much caching. Note that if you select the option to have the short leg before earnings, then you also need to select to use ONLY monthly options. Here is an example :

1 point

1 point -

@NikTam Look at https://steadyoptions.com/forums/forum/topic/4666-discussion-gs-october-2018-trade/?do=findComment&comment=105877 for the start of the discussion of the 'pre-pre earnings' calendar. The short leg is the monthly expiry before earnings, not after earnings. @cuegis I'm working on that, i should have some prototype ready on the production website tonight. It won't be the fastest for now (page might load slower than the rest, there won't be caching like the rest of the website, but it's just to get something out there). Noted, i think it makes sense. Maybe i could show it in 2 spots : In the RV chart, when you hover a data point, i can show both the straddle/calendar price and the VIX I can also add a new chart to the Straddle RV page and the Calendar RV page. The new chart will be called VIX, and for each cycle i will show the VIX That way you can do a spot check on the VIX chart, and then drill down on the hover if needed. It's a start until we find a better way to represent that.1 point

This leaderboard is set to New York/GMT-04:00