Leaderboard

Popular Content

Showing content with the highest reputation on 12/09/17 in all areas

-

With GMCR below 90 for the last couple of days, I closed this trade today. I closed the diagonal for 1.25 for a 36% gain, this is actually better than I anticipated given that GMCR had fallen well below my short 93 strike - but since GMCR options have relatively high IV there was still enough time premium in my May29 94 puts to allow me to get 1.25 even though the strike differential was 1.00 in the diagonal. I was thinking GMCR would have a less substantial drop this week, but with the diagonal trade structure I was able to make a nice gain even though the drop was much higher than I thought. I did the same thing with WMT after its post-earnings drop, buying the May29/May22 77.5/76.5 put diagonal yesterday morning for 0.72 (I didn't post that one in the forum because within 15 minutes of me making the trade WMT dropped some more and the trade was already up over 10%, so I didn't want anyone to jump in at a price much higher than mine). That trade is currently up a little over 30%, but I'm still holding and hoping to close for 1.00 or more by the end of the week. I'm liking this trade structure as a post-earnings (or post-event) directional trade when a stock has clear momentum in either direction - it can make gains if the stock price stays steady, moves a little in either direction or moves a lot in your direction, and you can adjust if the stock price gradually starts moving against you. The bigger loss scenario is when you get a quick and large move in the opposite direction, which is why I think the best time to trade it is when you get an outsized stock price move where a clear directional momentum is established. This may also be a good structure for VXX trades where the momentum is almost always downward - the BWB or 1x3x2 all start to lose if the VXX drops too much in your timeframe, so a VXX diagonal may work well although will have do some more analysis on this.1 point

-

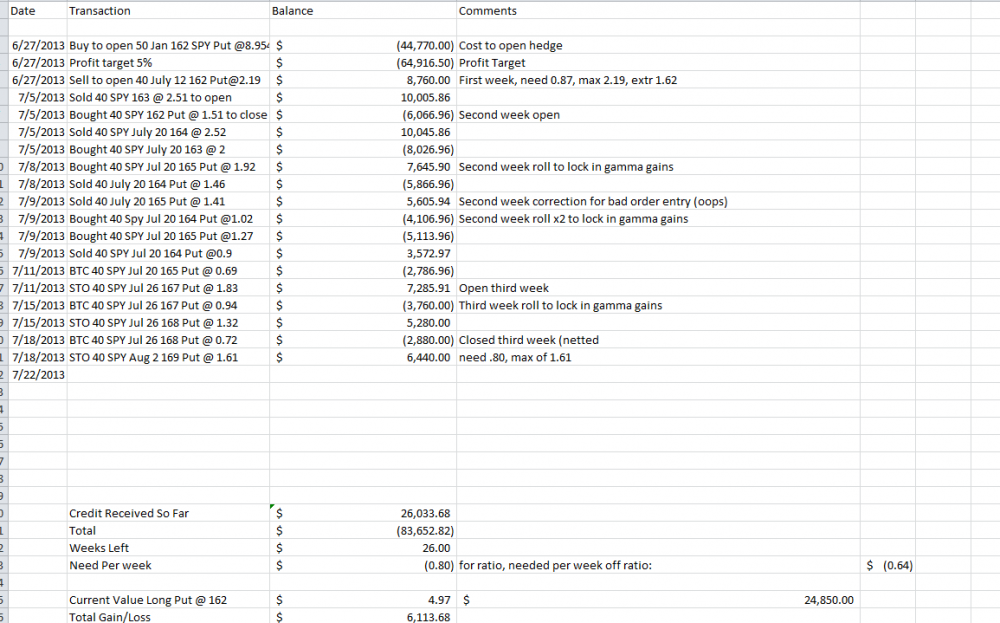

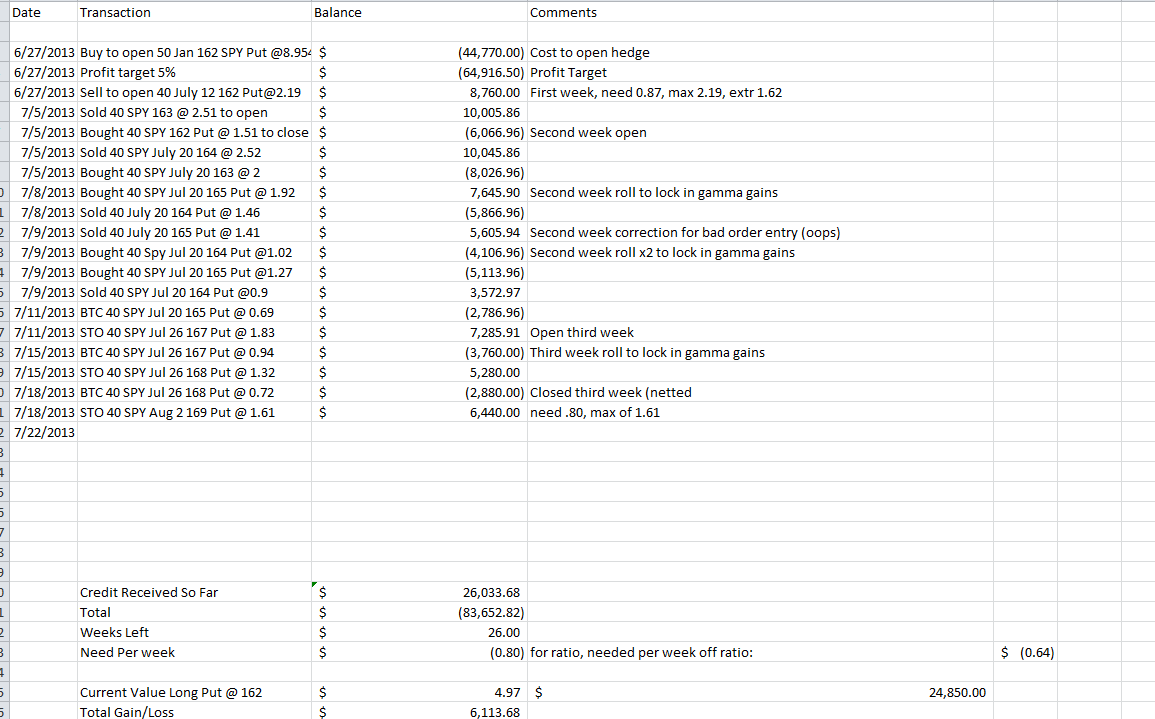

Here you go -- I normally don't include my trade sizes, but this well let you see exactly what I've been doing: Some of the comments got snipped, but if you have questions on a particularly week, just let me know. As you can see, part of the reason I think this trade is still working well -- we initially needed .87 a week to meet our profit target -- we're currently down to needing only .80/week. As of right now this week isn't going as well (only have netted about .15 so far on the week), but theta decay will give us another .07 or more by tomorrow, and if the market stays flat or goes up slightly, we'll get even more. The "total gain loss" and "credit receive so far" are both a little off as they each assume we keep the entirety of the credit from this week (so above the full 6,440), and that just probably won't happen. I keep the "off ratio" number in case the longs get to be DITM, then I know what my target has to be.

1 point

1 point -

I'll try to answer these in alternative order: 1. It is impossible to remove all assignment risk on any American Style option. I have actually been assigned on an option that was FAR OTM, that I was just going to let expire worthless -- with less than 2 days left on it. I'm sure some idiot just exercised his options for an unknown reason or an accident. While this is unusual, you can be assigned on an American Style Option at anytime. However, as long as there is extrinsic value left in the option, the chance of assignment is small. I never open an option position without knowing (a) if the option is European style or American style and ( what to do if it is an American style and I get assigned. Again the risk is normally small, but it is always there unless you trade a European style option. 2. The downside risk, if you're using leverage, in a ratio trade like this is if the market quickly spikes. A ratio trade like this is directionally biased. Take the last two days for instance, while my shorts have done GREAT, and I am earning extrinsic plus intrinsic value, the longs are getting hammered. Yesterday wasn't as bad as this morning, but right now my longs are down 22% more than my shorts are up. I'm not concerned with this right now, as I still am receiving more than enough credit to pay for things over time. But if this happened 2-3 weeks in a row, that would really hurt. If I was levered up 5x or 6x, it would destroy me. I would not use high leverage on this type of trade -- or any trade that is directionally biased unless I was prepared to lose 100% of my capital (I do have a high risk high reward portion of my portfolio that I do take naked long option or naked short option positions in, or other similar positions, but that makes up a small portion of the portfolio and I can stomach the risk and wild swings in it). 3. I wouldn't say it's a guessing game. I use a ratio trade if the current short strikes are OTM, ATM, or barely ITM. Once we get deeper in the money, I go 1:1 -- but that's because I'm neutral to downward biased right now, for a whole host of reasons. If I am wrong and the market goes up 5-10%, I'll roll up and out once or twice, but at some point I'd have to accept my market theory was wrong and just take my losses and move on. This strategy will work best in downward or neutral markets (or VERY slowly rising markets). As some readers have noted, the inverse trade can be done on the call side to accept the other side of the risk. I have not modeled what the effect of doing both in conjunction will do -- it might perform better overall, or it might perform less because the two perfectly cancel each other out -- don't know without actual back testing. 4. And yes there is -- it's called the Anchor Strategy (or an investment in the Anchor Fund). It's a variation of this strategy that's meant to have positive annual returns in all market conditions. That said, the cost of such a strategy is sacrificing the opportunity to write yourself checks at a rate of 2-5% per week. I personally do both. I would NEVER recommend on a board like this an allocation or investment plan (as everyone's goals, situations, and risk tolerances are different) -- that's why I have an actual investment firm (Lorintine Capital) to provide such advice to clients. My personal blend, and please note that I am young, very open and tolerant of risk (which the general investing public never understands), and can accept some losses. My current personal allocations and investments are: A. Six months of living expenses (all expenses, including house payments, car payments, bills, food, gas, etc), in six month rolling CDs paying a whopping .25% interest right now (so each month one CD comes up and I buy another one six months out) -- this is my safety cushion. Now that I have a kiddo, I have another account building up as I would like this to get up to one year worth, but at six months, I'm still comfortable; B. Fully fund IRAs -- in the US in particular, not doing this simply makes no sense, the benefits over time are just too large. My wife's IRA uses the Anchor Strategy while my IRA 50% Anchor strategy and 50% speculative strategies; C. Rest of my investments/savings are broken down as follows: -- 50% Anchor Strategy (actually in the Anchor Fund that I run) -- 15% in the LC Fund (a highly volatile hedge fund I run that uses many of the trades discussed on here, plus several others) -- 10% Option income strategies (some of which are the ones on here) -- 5% in Oil and Gas and Pipeline MMLPs and MMLP funds, partially hedged against dropping oil prices -- 5% REITs -- 5% Gold & Silver (some hard bullion some various funds, sometimes ETFs, it moves around) -- 5% tax exempt bonds -- 2.5% unrestrained bonds -- 2.5% bond funds hedged against changing interest rates AGAIN -- this is my division and should not be yours. The percentages aren't exact either as the markets move daily and I haven't done my quarterly adjustments -- right now I'm probably under weighted in bonds and precious metals, and over weighted in other areas. Hope that helps.,1 point

This leaderboard is set to New York/GMT-04:00