If 75% to 90% of "professional" money managers fail to beat the S&P500, then you are also guaranteeing better results than most "professionals". So, overall you are being extremely lazy, keeping trading costs to a minimum, as well as tax liabilities. You are paying very little attention to the markets and still, beating the vast majority of participants while nicely growing your nest egg.

I also argued that perhaps selling out of the money Calls, in addition to holding the index, was even better but I was not sure until I saw the evidence: BXM, an index that simulates a permanent Covered Call strategy on the S&P500 and has beaten the market in almost three decades. I discussed BXM in the Covered Call vs Buy and Hold article.

Well, today I want to talk about another very simple option selling strategy that beats most traders/investors:

Short Puts on the index, the CBOE PutWrite Index (PUT)

If you are selling a Put on an index and the market moves sideways you out-perform the buy & holder who went nowhere. If the index goes up, slightly (by less than the premium collected by the Put seller), the Short Put options strategy still outperforms the buy and holder. If the market falls, the Short Put options lose, but the cost basis for the investor is smaller than that of the buy and holder, who is also losing. So, in these three scenarios the Short Put wins over Buy and Hold which only outperforms during very strong markets.

Based on this idea, the PUT index was created by the CBOE years ago and it aims to simulate a permanent Short Put strategy on the S&P500. Taken from the CBOE site:

"PUT is an award-winning benchmark index that measures the performance of a hypothetical portfolio that sells S&P 500 Index (SPX) put options against collateralized cash reserves held in a money market account. The daily historical data for the PUT Index now extends back to June 30, 1986."

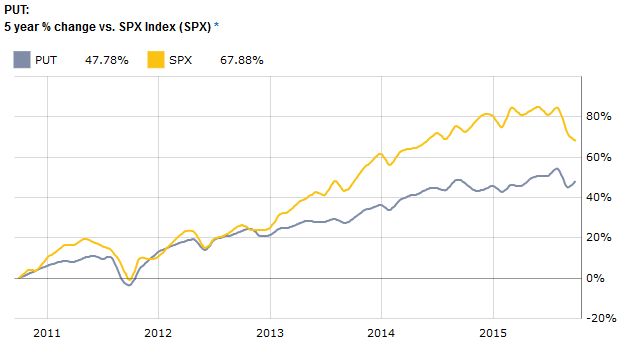

So, what is the performance of the PUT Index anyways?

What is more remarkable is the fact that it has done so with about 30% less volatility than the S&P500.

In terms of Risk Adjusted Returns, PUT shows a Sortino Ratio of 0.90 vs 0.50 for the S&P500. So, less risk, better returns. It's not that the strategy has obtained better returns because it is "riskier". It is in fact less risky.

Without a question, PUT is a superior strategy than Buy & Holding SPY (as proxy for holding the S&P500). But what about BXM?

PUT: +1153%

BXM: +830%

S&P500: +807%

That is as of this writing (October 2015)

The next interesting step would be to investigate how a portfolio made up of both PUT and BXMperforms, with half the capital allocated to each index. I'm curious about the potential of that approach where you are owing SPY, receiving dividends from it, selling Covered Calls on it and additionally shorting Puts to constantly reduce cost basis. All happening at the same time. This simulation is possible given the fact that the data on both indexes is public and free. So, I'll see what I can do. Even if the absolute return of this approach is about the same, it could still be worth it if it shows better risk-adjusted returns and even smaller draw-downs. Folks, has anybody seen some research on this? A portfolio combining both PUT and BXM? If so, feel free to share in the comments section.

Another nice thing about PUT is that it is compatible with tax advantaged accounts, like an IRA. Even though deep down, the mechanic is that of naked short selling, in practice you are simply "long" an Index, so it's perfectly legal.

If I were a passive Index follower with a very long term horizon of more than a decade, I would definitely invest in BXM and PUT instead of the S&P500. Without question. That way, I'm not only beating the majority of retail traders and professional money managers. I'm also beating passive index followers in the long run and suffering much less throughout the process (less volatility and smaller draw-downs).

UPDATE: After some email communication with readers it has been confirmed that both the PUT index and BXM index are just benchmarks for a public strategy but cannot be invested on directly. However, there are instruments that follow both index and can be used for investing or active trading. PBP can be used as a substitute for BXM and HVPW can be used as a substitute for PUT (Thanks Cherry)

For more information on the PUT index, visit the following CBOE pages:

- Definition and Results at a high level

- The PUT index methodology

- Research on PUT's out-performance over BXM

There are no comments to display.

Join the conversation

You can post now and register later. If you have an account, sign in now to post with your account.

Note: Your post will require moderator approval before it will be visible.