Leaderboard

Popular Content

Showing content with the highest reputation on 06/06/20 in all areas

-

Most members will know www.art-of.trading, an open website I run with the purpose of easy plotting RV charts. Now I have some bad news to convey. But there is some good news also. First the bad news: I will discontinue www.art-of.trading. After running it and offering its content for free for more than a year now I will not maintain the webservice longer in its current form. Daily updates will continue for now but the site will not be accessible anymore within some short period of time. Now here is the good news: There will be a replacement - a good one. Taking the essence of numerous discussions here on Steady Options and my personal take-aways and learnings from running art-of.trading I am up to offer an entirely new service for providing tools for trading the Steady Options way (in the same breath I should add a big thank you for all remarks and positive feedback I have gotten over the entire period. That is what made me take that route. On top I see that Steady Options continues to be a unique community on the web for trading options, with very good people and quality content - reason enough to stick around). I invite you to take a look at https://www.chartaffair.com Currently the site is working but open only to beta testers and not 'officially' released yet. Am still looking for some more beta testers. If you want to have early access I invite you to PM me for a free invitation code. Beta testers will get free access for some time once the site launches officially. Technically chartaffair.com is a more professional approach to running a webservice. And I have completely redesigned its code base. It uses a new data architecture, specifically targeted at handling and serving from large amounts of data. This together with fast hosting hardware and the use of new web technologies allows for two things: 1) Greatly increase available information You will find much more tables and graphs for each symbol with all information needed for trading the SO way: Historical implied move vs. actual move (as graphs and tables), credit needed for hedging straddle decay, actual performance of straddles around earnings. But also basic stuff like the next dividend ex-date or how long before the actual earnings announcement the announcement date gets confirmed (more details on specific features in later posts). Also, you will find practically any symbol now which comes at least with some traded options volume. 2) All information for a symbol aggregated on one single page Having all information in one place elminates the need to jump back and forth between different pages and websites, having to reenter the same symbol again and again (which I understood is an issue). A side bar allows for easy and fast navigation up and down on the page. All features came out of discussions and from my own experiences while trading. I believe they will be helpful. I will introduce some in greater detail in a couple of follow-up posts in this thread. On top of that there are a couple more pages to be added to this site. They are in planning and partly already in implementation. They will be added in the course of the next weeks/months. Chartaffair will be a paid service after the beta phase (it is not possible elsewise. But it will be worth it.) Now, if you found art-of.trading helpful over the course of last year, I invite you to sign up to chartaffair.com when the beta phase is completed. You will find it even more helpful. 2026 UPDATE: This tool has been discontinued.1 point

-

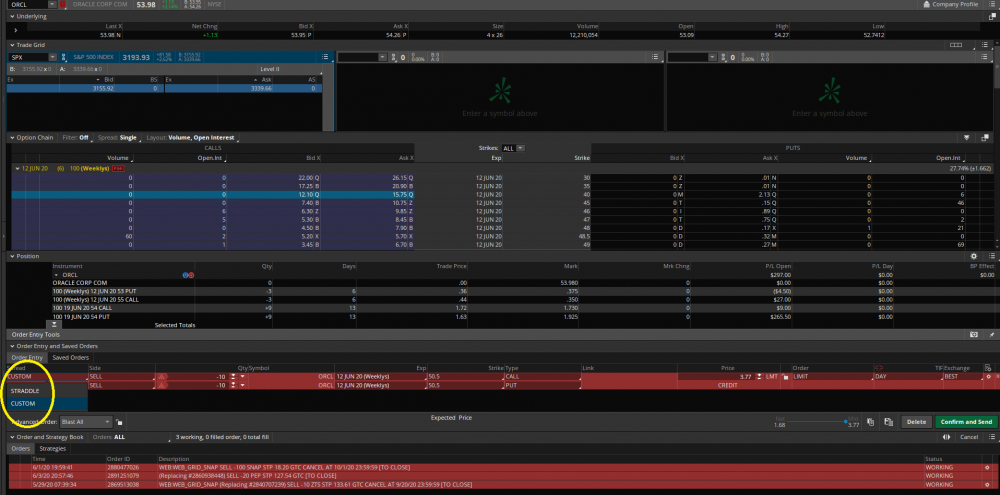

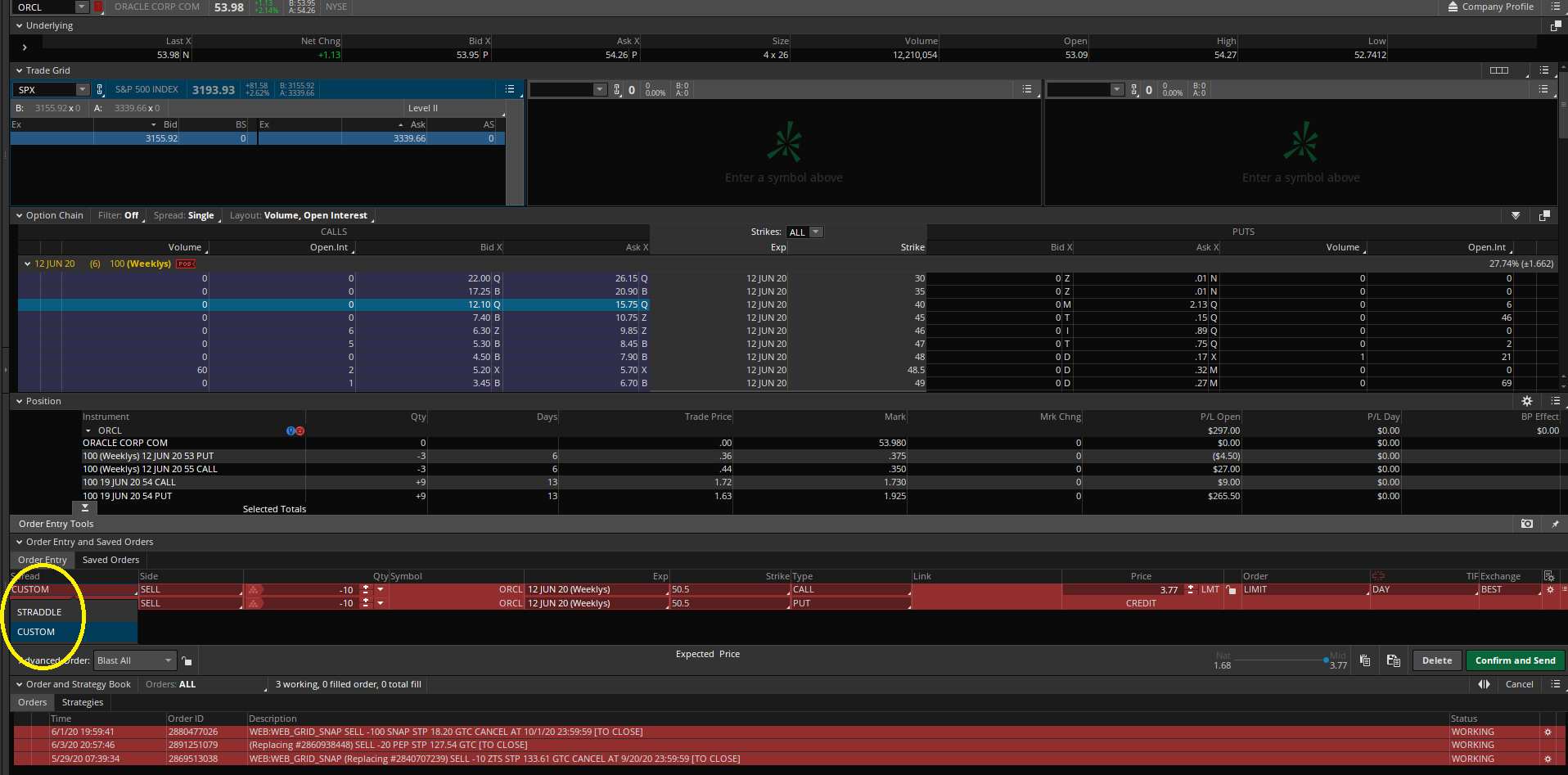

Morning Rumple! I think the most common problem people have is entering non standard trades with odd legs. To enter these trades you need to create a standard order and then change the order type to custom. You can then change the number of contracts on each leg independently. Let me know if you have specific questions and I'll try to help. Otherwise, youtube is a great resource for general educational videos on ToS. I would advise searching for videos from within the last year to make sure you are viewing content that is still valid. Best - Matt.

1 point

1 point -

What I began to realize over the years was that the risk I was taking with iron condors was excessive, so the thought of selling a “naked” strangle was unimaginable. This risk was due to ridiculously large position size, or leverage, and over time I began to understand this reality better. An iron condor is simply a short strangle with long options that are further out of the money than the short options. Some traders refer to the long options as “wings”. Because an iron condor creates a maximum potential loss equivalent to the width of the spread, traders make the mistake of often trading their account up to or near the maximum number of contracts that would wipe out most of their account if that max loss occurred, which during periods of low market volatility may be as minor as a 10-15% drop in the market.The average intra-year drawdown for the S&P 500 has been about 14% since 1980, so this is something that occurs almost every year. This is of course why you hear so many stories of retail traders and credit spread/iron condor newsletters blowing up. As is almost always the case, the risk isn’t really the strategy…but instead the position size of the strategy! There’s no strategy so good that enough leverage can’t make it a blow up waiting to happen. Due to the nature of out of the money option selling, the negatively skewed return stream can take a while to materialize when there are long periods of relatively calm market conditions. Today, I think of a strangle as a cash secured put along with an out of the money short call. Thinking about the trade this way transforms a short strangle from seemingly risky into a rather conservative trade, due to the position sizing rule. For example, with SPX currently trading at about $3,000, a strangle would be sized at about 1 contract per $300,000. Compare this to selling 10-point wide put and call credit spreads to create an iron condor, and many newsletters might suggest that you sell something like 275 contracts per $300,000 of capital! Think about that for a moment…technically the iron condor has “defined risk” of $275,000 (ignoring the credit received), while the strangle has “undefined” risk because the short call is naked and prices can theoretically rise forever. Yet the risk is immensely different for the two trades due to the number of contracts involved. The strangle has a positive expected return and will very likely survive and succeed over the long-term due to the well documented Volatility Risk Premium (VRP), while the iron condor will cause an eventual blowup. When someone says they prefer iron condors over strangles because the risk is “defined” with an iron condor, they probably haven’t spent a lot of time thinking about position sizing. This should be the biggest lesson from this article…risk is defined by your position size to a much greater degree than it is by the strategy. Yet it’s a topic that is not well understood or appreciated by most traders. I think about an iron condor similar to how I’d think about owning 100 shares of a stock and then buying a protective put. A strangle is like owning just those 100 shares, while an iron condor is like owning those 100 shares along with an out of the money protective put. That put will reduce your downside during extreme selloffs that are greater than the market already baked into prices, but at a substantial cost over the long run (again, due to the VRP). To illustrate this, I backtested SPY strangles and iron condors using the ORATS wheel. Selling 30 delta strangles on SPY since 2007 has produced an average annual return of 5.34% (volatility of 8.36%, Sharpe Ratio 0.64), while a 30 delta iron condor with wings set at 20 delta returned only 0.15% (volatility of 3.08%, Sharpe Ratio of 0.05). I ran the test a few times just to make sure I was getting consistent results. The additional transaction costs and performance drag of the long options is so significant that almost the entire return generated from the short options disappears. Another comparison is Iron Condor Vs. Iron Butterfly Conclusion On your journey as an options trader you’ll hear a lot of conventional wisdom repeated over and over that simply isn’t true or provides incomplete information. One of those myths is how selling strangles is risky and instead a trader should sell an iron condor. This statement tells us nothing about position sizing. If you read this article and are still resisting the information I’m sharing, ask yourself this question: Is the reason you still want to use an iron condor over a strangle due to how you might look at the expected return of the strangle as I’ve laid it out and feel a little underwhelmed? Perhaps this article is also what you need to hear instead of what you want to hear, because I know I was in that camp at one time. You might consider that the 5% return of the SPY strangle since 2007 is similar to the long-term global equity risk premium, which serves as the benchmark for virtually everything since so few investments have been proven to be able to reliably exceed it over the long term.Until someone shows you an independently audited decade plus long track record of a fund or newsletter selling iron condors with the “X% per month” average returns that are often fantasized about and marketed to new traders, use the position sizing algorithm presented in this article instead as your baseline. Think in terms of notional risk instead of margin requirements, and you’ll substantially reduce the risk of an unrecoverable negative surprise on your trading journey. Jesse Blom is a licensed investment advisor and Vice President of Lorintine Capital, LP. He provides investment advice to clients all over the United States and around the world. Jesse has been in financial services since 2008 and is a CERTIFIED FINANCIAL PLANNER™ professional. Working with a CFP® professional represents the highest standard of financial planning advice. Jesse has a Bachelor of Science in Finance from Oral Roberts University. Jesse manages the Steady Momentum service, and regularly incorporates options into client portfolios. Related articles Selling Naked Strangles: The Math Selling Short Strangles And Straddles - Does It Work? Selling Options Premium: Myths Vs. Reality Karen The Supertrader: Myth Or Reality? Karen Supertrader: Too Good To Be True? How Victor Niederhoffer Blew Up - Twice The Spectacular Fall Of LJM Preservation And Growth James Cordier: Another Options Selling Firm Goes Bust Trading An Iron Condor: The Basics The Hidden Dangers Of Iron Condors1 point

What I began to realize over the years was that the risk I was taking with iron condors was excessive, so the thought of selling a “naked” strangle was unimaginable. This risk was due to ridiculously large position size, or leverage, and over time I began to understand this reality better. An iron condor is simply a short strangle with long options that are further out of the money than the short options. Some traders refer to the long options as “wings”. Because an iron condor creates a maximum potential loss equivalent to the width of the spread, traders make the mistake of often trading their account up to or near the maximum number of contracts that would wipe out most of their account if that max loss occurred, which during periods of low market volatility may be as minor as a 10-15% drop in the market.The average intra-year drawdown for the S&P 500 has been about 14% since 1980, so this is something that occurs almost every year. This is of course why you hear so many stories of retail traders and credit spread/iron condor newsletters blowing up. As is almost always the case, the risk isn’t really the strategy…but instead the position size of the strategy! There’s no strategy so good that enough leverage can’t make it a blow up waiting to happen. Due to the nature of out of the money option selling, the negatively skewed return stream can take a while to materialize when there are long periods of relatively calm market conditions. Today, I think of a strangle as a cash secured put along with an out of the money short call. Thinking about the trade this way transforms a short strangle from seemingly risky into a rather conservative trade, due to the position sizing rule. For example, with SPX currently trading at about $3,000, a strangle would be sized at about 1 contract per $300,000. Compare this to selling 10-point wide put and call credit spreads to create an iron condor, and many newsletters might suggest that you sell something like 275 contracts per $300,000 of capital! Think about that for a moment…technically the iron condor has “defined risk” of $275,000 (ignoring the credit received), while the strangle has “undefined” risk because the short call is naked and prices can theoretically rise forever. Yet the risk is immensely different for the two trades due to the number of contracts involved. The strangle has a positive expected return and will very likely survive and succeed over the long-term due to the well documented Volatility Risk Premium (VRP), while the iron condor will cause an eventual blowup. When someone says they prefer iron condors over strangles because the risk is “defined” with an iron condor, they probably haven’t spent a lot of time thinking about position sizing. This should be the biggest lesson from this article…risk is defined by your position size to a much greater degree than it is by the strategy. Yet it’s a topic that is not well understood or appreciated by most traders. I think about an iron condor similar to how I’d think about owning 100 shares of a stock and then buying a protective put. A strangle is like owning just those 100 shares, while an iron condor is like owning those 100 shares along with an out of the money protective put. That put will reduce your downside during extreme selloffs that are greater than the market already baked into prices, but at a substantial cost over the long run (again, due to the VRP). To illustrate this, I backtested SPY strangles and iron condors using the ORATS wheel. Selling 30 delta strangles on SPY since 2007 has produced an average annual return of 5.34% (volatility of 8.36%, Sharpe Ratio 0.64), while a 30 delta iron condor with wings set at 20 delta returned only 0.15% (volatility of 3.08%, Sharpe Ratio of 0.05). I ran the test a few times just to make sure I was getting consistent results. The additional transaction costs and performance drag of the long options is so significant that almost the entire return generated from the short options disappears. Another comparison is Iron Condor Vs. Iron Butterfly Conclusion On your journey as an options trader you’ll hear a lot of conventional wisdom repeated over and over that simply isn’t true or provides incomplete information. One of those myths is how selling strangles is risky and instead a trader should sell an iron condor. This statement tells us nothing about position sizing. If you read this article and are still resisting the information I’m sharing, ask yourself this question: Is the reason you still want to use an iron condor over a strangle due to how you might look at the expected return of the strangle as I’ve laid it out and feel a little underwhelmed? Perhaps this article is also what you need to hear instead of what you want to hear, because I know I was in that camp at one time. You might consider that the 5% return of the SPY strangle since 2007 is similar to the long-term global equity risk premium, which serves as the benchmark for virtually everything since so few investments have been proven to be able to reliably exceed it over the long term.Until someone shows you an independently audited decade plus long track record of a fund or newsletter selling iron condors with the “X% per month” average returns that are often fantasized about and marketed to new traders, use the position sizing algorithm presented in this article instead as your baseline. Think in terms of notional risk instead of margin requirements, and you’ll substantially reduce the risk of an unrecoverable negative surprise on your trading journey. Jesse Blom is a licensed investment advisor and Vice President of Lorintine Capital, LP. He provides investment advice to clients all over the United States and around the world. Jesse has been in financial services since 2008 and is a CERTIFIED FINANCIAL PLANNER™ professional. Working with a CFP® professional represents the highest standard of financial planning advice. Jesse has a Bachelor of Science in Finance from Oral Roberts University. Jesse manages the Steady Momentum service, and regularly incorporates options into client portfolios. Related articles Selling Naked Strangles: The Math Selling Short Strangles And Straddles - Does It Work? Selling Options Premium: Myths Vs. Reality Karen The Supertrader: Myth Or Reality? Karen Supertrader: Too Good To Be True? How Victor Niederhoffer Blew Up - Twice The Spectacular Fall Of LJM Preservation And Growth James Cordier: Another Options Selling Firm Goes Bust Trading An Iron Condor: The Basics The Hidden Dangers Of Iron Condors1 point

This leaderboard is set to New York/GMT-04:00