All Activity

- Today

- Yesterday

- Last week

-

It’s a luck-based game that you’ll probably lose. Does this mean that you shouldn’t even consider investing unless you’re an expert? No. New investors can build wealth and experience, but it takes more than just going by vibes and hoping for the best. Here are a few tips to help you build a portfolio that can grow steadily and ideally mitigate what risks you come up against. 1. Create a Trading Plan The first mistake a lot of people make when they jump into crypto trading is that they don’t have a plan to start with. If you just get some money and buy some random currency, you might make money out of it, but you’ll probably just lose what you invested. Instead, make a crypto trading plan. Set goals for yourself and make some ground rules before you start trading. For example, you might set goals for: Day trading profits Passive income Long-term investment growth Asset diversification Goals like this allow you to work out a path to achieve what you want, rather than blinding buying and hoping for the best. You also want to determine what risks you’re willing and not willing to take, and stick to your ground rules. Finally, you can choose a trading strategy. Popular strategies include day trading, scalping, and buying and holding, but there are a few more to explore and choose from. 2. Understand Red Flags The first thing to be aware of is that investment, especially crypto currency investment, is risky. The easiest way to mitigate these risks is to develop an ability to identify and avoid red flags. These might include: Sellers trying to rush you Insubstantiated claims of good performance Pump and dump schemes A poor or nonexistent creator reputation You might miss out on a few good opportunities by being cautious with where you invest. But you’re much more likely to miss out on some pretty major issues, such as schemes designed to get loads of investors and take their money before dumping the stocks and selling fast. Unfortunately, there are plenty of scammers in the crypto-currency market, so learn their tricks and how to avoid them. If something seems to good to be true, it probably is. 3. Only Invest What You Can Afford to Lose Investment is a far better way to build wealth than savings account, but this comes at a price. You can always lose what you invest. Except for very rare situations (like real estate investments), you should never take out a loan to invest in anything. This is because if your investment goes poorly, you essentially put yourself into debt. If you’re already in debt, pay off your debts before you invest. Always use liquid funds that you can afford to lose before making an investment, especially if you’re going to invest in a high-risk venture like cryptocurrency. But what about people who seem to live entirely off credit and net worth? It is possible and viable to do this, but you should bear in mind that these people are usually worth millions, if not billions. It’s definitely not a strategy for people new to investing, because you can bankrupt yourself just as easily as making it big. 4. Dollar-Cost Averaging One strategy that some people find very effective is dollar-cost averaging. This is a great way to combat the inherent volatility of the crypto market. Essentially, it automates your investment so you can make regular, small investments that spreads out your purchases. This means that the amount you pay isn’t dominated by market timing. This is a long-term investment strategy that works great for beginner investors who want to slowly build up a portfolio without taking on a lot of risk at once. 5. Focus on Major Cryptocurrencies If you want to reduce your risk when investing in crypto, the best bet is often to focus on the big, more established players. Bitcoin and Ethereum are often much safer to invest in than smaller, newer cryptocurrencies that move about more violently. They’ve already proved their worth, surviving through market cycles and downturns, and have multiple financial products that use them as a foundation. This isn’t to say that there’s no risk in these investments, but it’s a good place to start. Once you are more established, you should start to look into newer, more promising and active prospects. 6. Invest With Your Mind, Not Your Heart The hype train can be very dangerous when it comes to cryptocurrencies. Always stay objective, even if your friends are jumping on a bandwagon. You should never invest due to vibes, FOMO, hype, or even memes. Instead, invest boringly. Make sure whatever information you’re investing based on is accurate. If it comes to it, don’t be afraid to cut your losses if an investment you thought was a sure deal falters. 7. Keep Your Investments Secure Unfortunately, crypto-currency can be vulnerable to theft. So make sure you store your holdings somewhere secure. A hardware wallet or a trusted crypto-custodian can keep your assets safe from potential hackers. You should also have a recovery phrase that’s kept somewhere safe and offline. This makes it much harder for anyone but you to access it. 8. Crypto-Accounting Software As you build a more complicated portfolio, with potentially multiple wallets and different types of assets, you should consider using crypto-accounting software to help you keep track of your investments and your income. This gives you accurate financial data and full coverage of your transactions and chains, so you can know exactly what’s going on in your portfolio no matter how complicated or extensive it might get. This also helps you to spot financial gaps and keep accurate books for compliance. This is a contributed post.

It’s a luck-based game that you’ll probably lose. Does this mean that you shouldn’t even consider investing unless you’re an expert? No. New investors can build wealth and experience, but it takes more than just going by vibes and hoping for the best. Here are a few tips to help you build a portfolio that can grow steadily and ideally mitigate what risks you come up against. 1. Create a Trading Plan The first mistake a lot of people make when they jump into crypto trading is that they don’t have a plan to start with. If you just get some money and buy some random currency, you might make money out of it, but you’ll probably just lose what you invested. Instead, make a crypto trading plan. Set goals for yourself and make some ground rules before you start trading. For example, you might set goals for: Day trading profits Passive income Long-term investment growth Asset diversification Goals like this allow you to work out a path to achieve what you want, rather than blinding buying and hoping for the best. You also want to determine what risks you’re willing and not willing to take, and stick to your ground rules. Finally, you can choose a trading strategy. Popular strategies include day trading, scalping, and buying and holding, but there are a few more to explore and choose from. 2. Understand Red Flags The first thing to be aware of is that investment, especially crypto currency investment, is risky. The easiest way to mitigate these risks is to develop an ability to identify and avoid red flags. These might include: Sellers trying to rush you Insubstantiated claims of good performance Pump and dump schemes A poor or nonexistent creator reputation You might miss out on a few good opportunities by being cautious with where you invest. But you’re much more likely to miss out on some pretty major issues, such as schemes designed to get loads of investors and take their money before dumping the stocks and selling fast. Unfortunately, there are plenty of scammers in the crypto-currency market, so learn their tricks and how to avoid them. If something seems to good to be true, it probably is. 3. Only Invest What You Can Afford to Lose Investment is a far better way to build wealth than savings account, but this comes at a price. You can always lose what you invest. Except for very rare situations (like real estate investments), you should never take out a loan to invest in anything. This is because if your investment goes poorly, you essentially put yourself into debt. If you’re already in debt, pay off your debts before you invest. Always use liquid funds that you can afford to lose before making an investment, especially if you’re going to invest in a high-risk venture like cryptocurrency. But what about people who seem to live entirely off credit and net worth? It is possible and viable to do this, but you should bear in mind that these people are usually worth millions, if not billions. It’s definitely not a strategy for people new to investing, because you can bankrupt yourself just as easily as making it big. 4. Dollar-Cost Averaging One strategy that some people find very effective is dollar-cost averaging. This is a great way to combat the inherent volatility of the crypto market. Essentially, it automates your investment so you can make regular, small investments that spreads out your purchases. This means that the amount you pay isn’t dominated by market timing. This is a long-term investment strategy that works great for beginner investors who want to slowly build up a portfolio without taking on a lot of risk at once. 5. Focus on Major Cryptocurrencies If you want to reduce your risk when investing in crypto, the best bet is often to focus on the big, more established players. Bitcoin and Ethereum are often much safer to invest in than smaller, newer cryptocurrencies that move about more violently. They’ve already proved their worth, surviving through market cycles and downturns, and have multiple financial products that use them as a foundation. This isn’t to say that there’s no risk in these investments, but it’s a good place to start. Once you are more established, you should start to look into newer, more promising and active prospects. 6. Invest With Your Mind, Not Your Heart The hype train can be very dangerous when it comes to cryptocurrencies. Always stay objective, even if your friends are jumping on a bandwagon. You should never invest due to vibes, FOMO, hype, or even memes. Instead, invest boringly. Make sure whatever information you’re investing based on is accurate. If it comes to it, don’t be afraid to cut your losses if an investment you thought was a sure deal falters. 7. Keep Your Investments Secure Unfortunately, crypto-currency can be vulnerable to theft. So make sure you store your holdings somewhere secure. A hardware wallet or a trusted crypto-custodian can keep your assets safe from potential hackers. You should also have a recovery phrase that’s kept somewhere safe and offline. This makes it much harder for anyone but you to access it. 8. Crypto-Accounting Software As you build a more complicated portfolio, with potentially multiple wallets and different types of assets, you should consider using crypto-accounting software to help you keep track of your investments and your income. This gives you accurate financial data and full coverage of your transactions and chains, so you can know exactly what’s going on in your portfolio no matter how complicated or extensive it might get. This also helps you to spot financial gaps and keep accurate books for compliance. This is a contributed post. -

How SteadyOptions Calculates Performance

Emily Carter commented on Kim's article in SteadyOptions Trading Blog

Really informative breakdown of how performance is calculated. I appreciate the transparency and the clear explanation of the relationship between ROI and portfolio returns. Very helpful for traders trying to understand realistic expectations. -

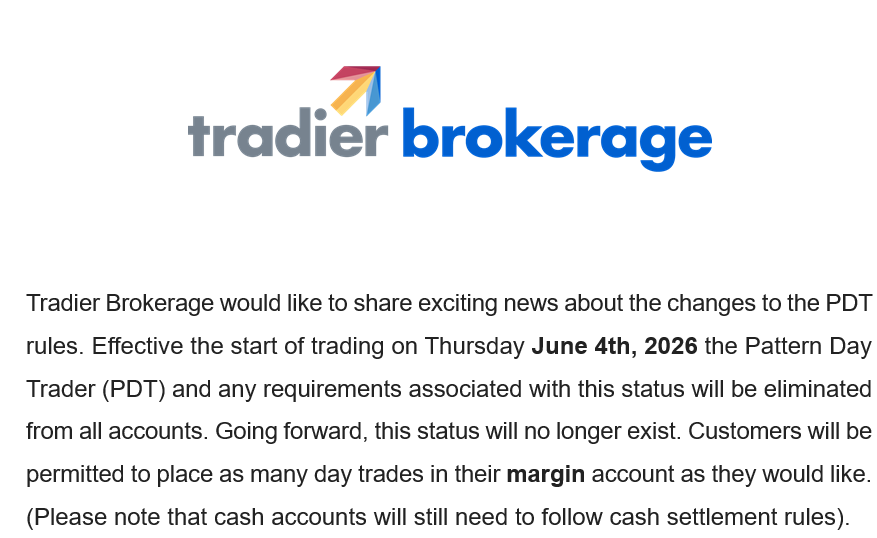

Yes, they are. The SEC announced the change on April 16, and allowed brokerages 18 months to implement it .This link from Schwab explains the change. In short: "...Under the new rules, traders will no longer be required to maintain a minimum account balance of $25,000 to engage in frequent margin day trading. Instead, eligible margin accounts of more than $2,000 will gain access to intraday margin buying power set by individual brokerages based on current positions and maintenance margin requirements. Currently, under the old rules, four or more day trades in five business days triggers a "pattern day trader" designation and the $25,000 requirement. Under the new framework, the pattern day trader designation will be eliminated, and day trades will no longer be counted...."

- 1 reply

-

- 2

-

-

Just received this mail, a little surprising as I believe in part these rules are ımposed by exchanges

-

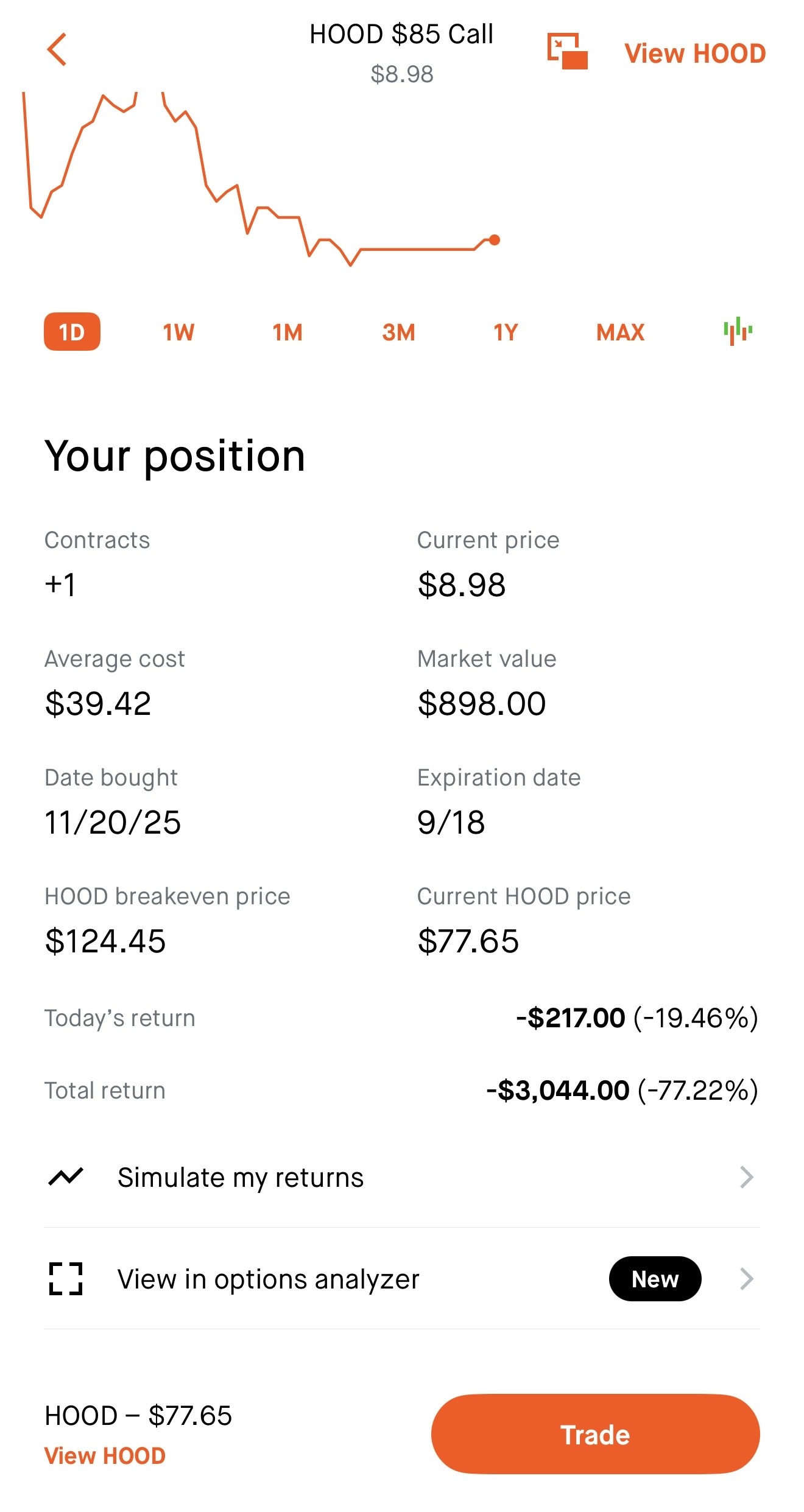

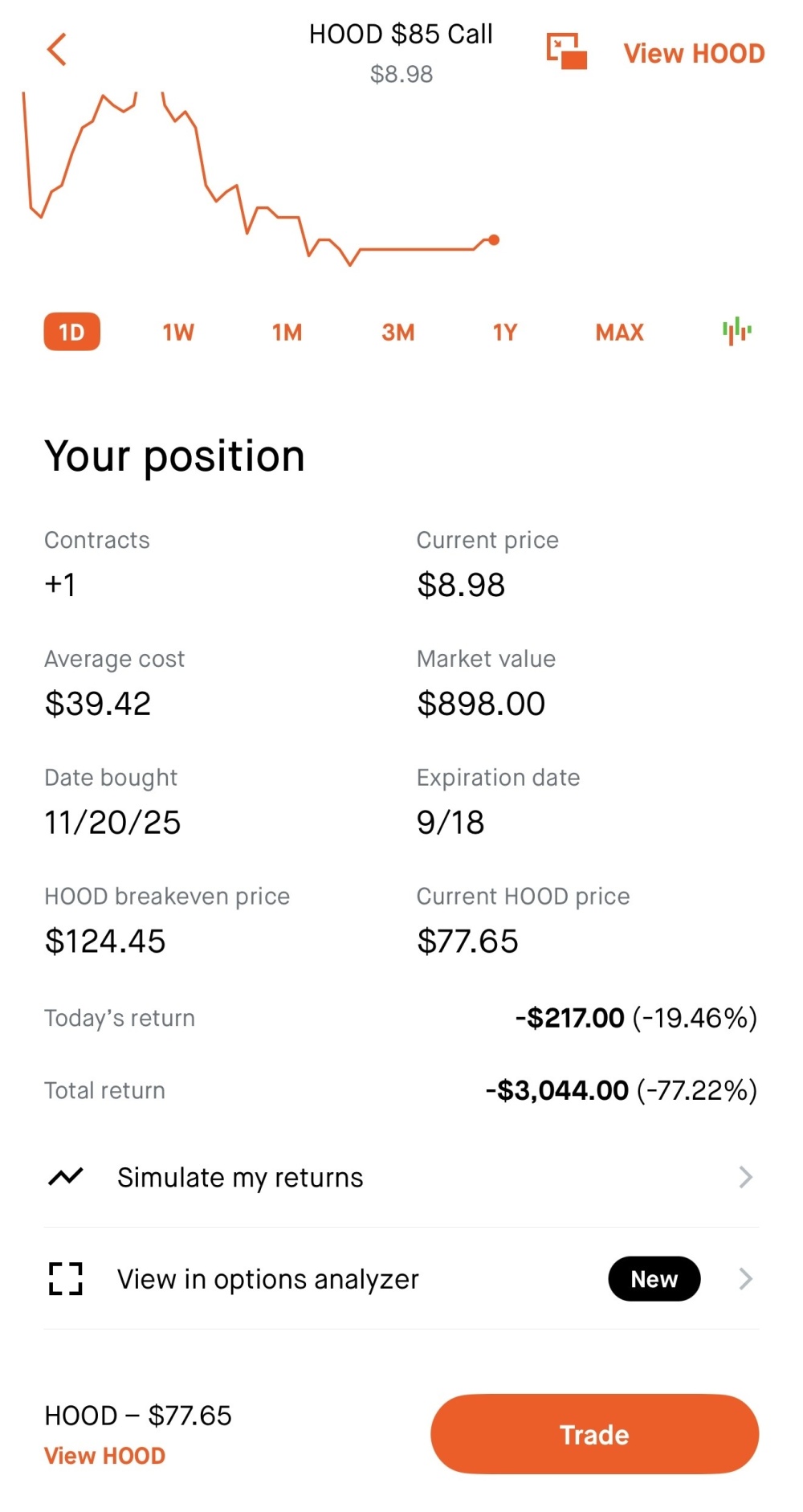

@rajavel44 Since you have 1 long option you can use a form of the stock recovery strategy. This would be buying a 1x2 call ratio spread where you'd buy another September 85 call and sell 2 September 105 calls - this could be done for close to zero or a small debit and leave you with 2 long 85 calls and 2 short 105 calls. This would cap your gains at the stock price of 105 or beyond at expiration - but it allows your gains to grow at 2x the rate (compared to just having the long call) between the stock prices of 85 and 105. Therefore, with this 1x2 spread added your overall break-even would be lowered to the stock price being at 105 or above by expiration (but since your gains are capped at a stock price of 105 this means your best case outcome is around break-even on your overall trade). Summarizing, if you hold until September expiration your results be as follows: Stock price below 85 - you lose 100% of what you paid (same as with just the long call), but since the 1x2 was put on for close to zero cost this will have minimal impact on your overall loss amount. Stock price between 86-105 - your loss gets smaller the more the stock price rises and the value of this spread will twice what just the long call would have been. Stock price above 105 - gains are capped at a stock price of 105 where the total value would be 40.00. If the stock price is above 105 it would be the same thing as stock price at 105.

- Earlier

-

Boatdrinks joined the community

Boatdrinks joined the community -

Luay joined the community

Luay joined the community -

13january13 joined the community

13january13 joined the community -

16january16 joined the community

16january16 joined the community -

rajavel44 joined the community

rajavel44 joined the community -

-

Which tools are best for backtesting trading?

Yowster replied to Tradingwise23's topic in General Board

I like OptionNetExlorer (ONE) for that. It allows you to enter any type of trade at a specific date in the past and then step through it day-by-day where you see dots that represent intra-day prices each day (so you can see the range of prices throughout the day). Other tools show end-of-day pricing for trades using SO strategies for stocks in prior earnings cycles, and this is a great scanning tool. But if you want to see the day-to-day daily detail of how a trade strategy progresses through time then ONE is great for that. -

kesalvijayeri joined the community

kesalvijayeri joined the community -

(1).thumb.png.0ab0145ca2102f360a8d3a7e17838eee.png) Tradingwise23 changed their profile photo

Tradingwise23 changed their profile photo -

Tradingwise23 joined the community

-

Which tools are best for backtesting trading?

-

Martin Sikora joined the community

Martin Sikora joined the community -

Guy the Great joined the community

Guy the Great joined the community -

Yes it includes the heatmap.

- 1130 replies

-

- 1

-

-

- rv chart

- volatilityhq.com

- (and 1 more)

-

I am about to subscribe. Can you confirm that the subscription also includes those heat maps? It is indeed a key piece of the puzzle I was missing, and it seems I am about to resolve it. (I have been nagging Kim for months about this issue.) The reason I ask is that the page https://www.volatilityhq.com/payments/subscribe/ says nothing about those heatmaps. It only mentions RV charts and a scanner. @Kim @Yowster

-

Seems to be back up. It may have had to do with an expired certificate somewhere on the provider's end.

-

YES for me Thank You

-

Is it back for anyone ? It seems it's back for me but i don't understand why i was down in the first place.

-

It's down for me too, i'm not sure what's going on. I think it's the first time the service goes down like that. Looking into it.

-

Same for me

- 1130 replies

-

- 1

-

-

- rv chart

- volatilityhq.com

- (and 1 more)

-

I see 503 error.

-

Hi is volhq currently down for anyone else right now?

-

Looks like a great tool but I dont have time to assess before June.

Looks like a great tool but I dont have time to assess before June. -

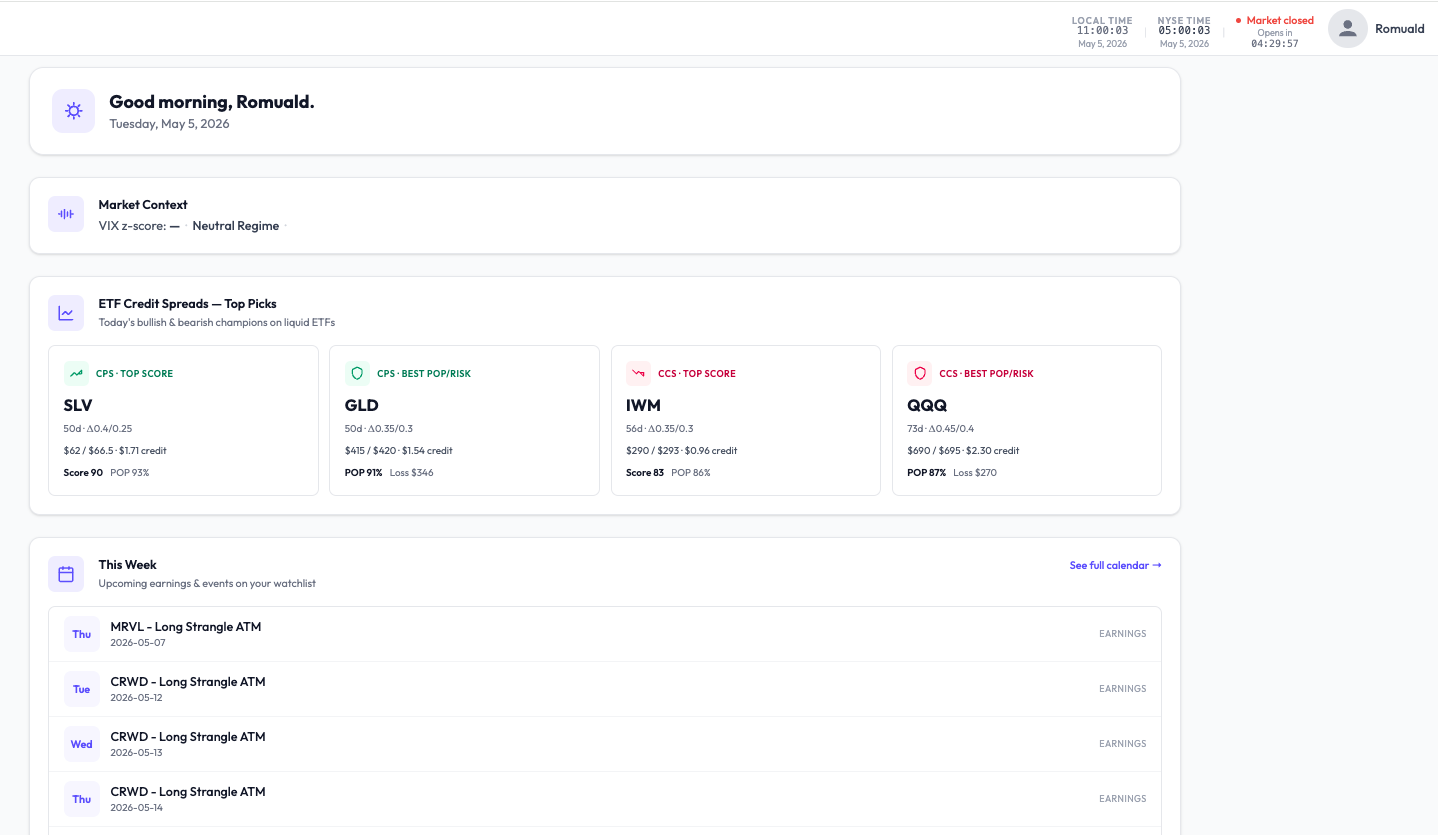

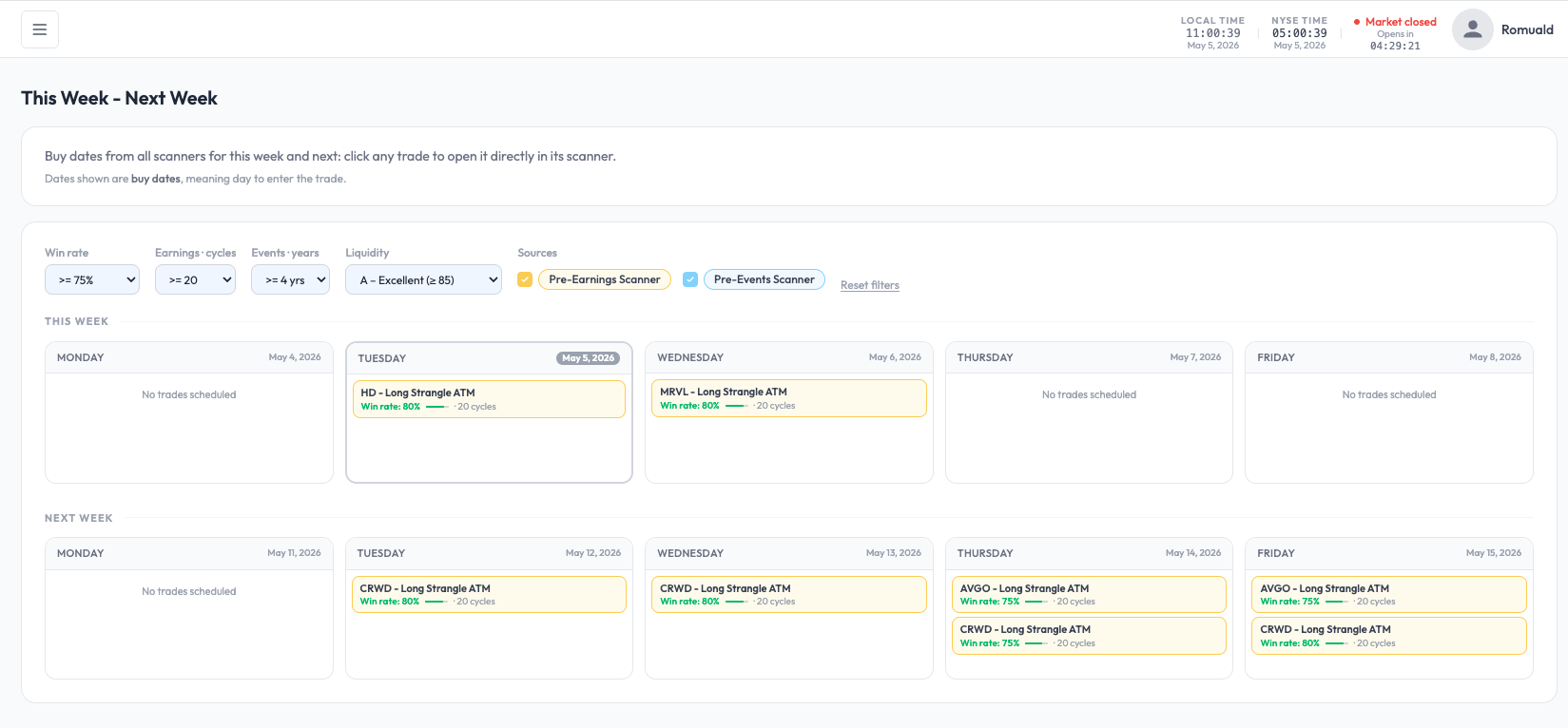

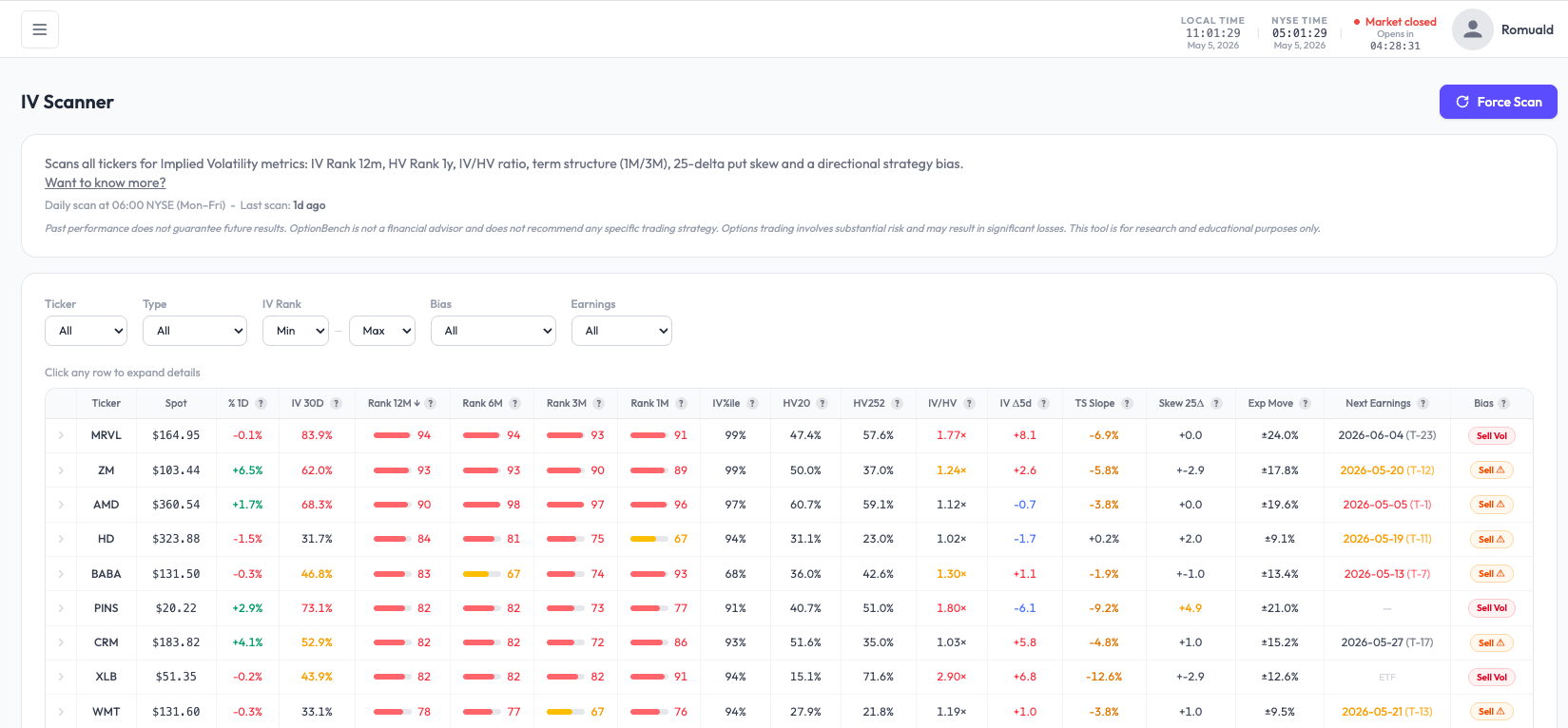

Here is an interesting discussion with Srini M: Romuald 889 Replied: 16 hours ago · IP Hi Srini, thanks for the honest feedback — those are exactly the right questions. How is OptionBench different from MarketChameleon? MC is a great general-purpose options data platform — they cover earnings strategies, IV scans, unusual options activity, and a lot more. We're going in a more focused direction: - We only scan a curated universe (26 liquid ETFs for credit spreads, ~80 stocks for pre-earnings) instead of the whole market — the goal is depth over breadth on the setups that actually work for retail credit-spread traders - Every metric shows its uncertainty: POP comes with a confidence band (e.g., "93.32% ± 0.91"), not just a single number. Backtests show sample size warnings (Low / Medium / High confidence based on number of historical analogues) - We Monte-Carlo every credit spread across 12 DTEs × 7 delta pairs × 5 take-profit levels (5,000 sims each) — the scanner doesn't pick one "right" setup, it shows you the entire opportunity surface and scores them - Pricing target ~50% of MC, single tier, no upsell pressure - We publish negative results too — when we backtest a strategy and it doesn't have edge, it gets archived as "tested but not deployed", not buried. Keeps us honest with ourselves and users. Different positioning, not better — we're a focused tool for traders who already know credit spreads and want depth, not a one-stop shop. On videos / quick learning Fair point and I agree. For the beta, I'll have a Quick Start guide (5-min read) and 2-3 short walkthrough videos focused on the most-asked workflows: 1) "I have 30 minutes, find me 3 credit spread candidates" 2) "Pre-earnings setup walkthrough on a real ticker" 3) "What do all these metrics mean and which ones matter most" Tooltips on every metric in-app too. On "minimal time to find profitable trades" That's literally the design philosophy. The "Today" briefing on the homepage shows the 4 best CPS picks, 4 best CCS picks, this week's earnings tickers, and upcoming macro events — all curated, not raw data dumps. The full scanners are there if you want to dig deeper, but the homepage is built to answer "what's worth my time today". Beta starts in a few weeks. If you want to test it and call out where we miss the mark, I'd genuinely value the feedback. Romuald Disclaimer: not financial advice, options trading involves substantial risk.

Here is an interesting discussion with Srini M: Romuald 889 Replied: 16 hours ago · IP Hi Srini, thanks for the honest feedback — those are exactly the right questions. How is OptionBench different from MarketChameleon? MC is a great general-purpose options data platform — they cover earnings strategies, IV scans, unusual options activity, and a lot more. We're going in a more focused direction: - We only scan a curated universe (26 liquid ETFs for credit spreads, ~80 stocks for pre-earnings) instead of the whole market — the goal is depth over breadth on the setups that actually work for retail credit-spread traders - Every metric shows its uncertainty: POP comes with a confidence band (e.g., "93.32% ± 0.91"), not just a single number. Backtests show sample size warnings (Low / Medium / High confidence based on number of historical analogues) - We Monte-Carlo every credit spread across 12 DTEs × 7 delta pairs × 5 take-profit levels (5,000 sims each) — the scanner doesn't pick one "right" setup, it shows you the entire opportunity surface and scores them - Pricing target ~50% of MC, single tier, no upsell pressure - We publish negative results too — when we backtest a strategy and it doesn't have edge, it gets archived as "tested but not deployed", not buried. Keeps us honest with ourselves and users. Different positioning, not better — we're a focused tool for traders who already know credit spreads and want depth, not a one-stop shop. On videos / quick learning Fair point and I agree. For the beta, I'll have a Quick Start guide (5-min read) and 2-3 short walkthrough videos focused on the most-asked workflows: 1) "I have 30 minutes, find me 3 credit spread candidates" 2) "Pre-earnings setup walkthrough on a real ticker" 3) "What do all these metrics mean and which ones matter most" Tooltips on every metric in-app too. On "minimal time to find profitable trades" That's literally the design philosophy. The "Today" briefing on the homepage shows the 4 best CPS picks, 4 best CCS picks, this week's earnings tickers, and upcoming macro events — all curated, not raw data dumps. The full scanners are there if you want to dig deeper, but the homepage is built to answer "what's worth my time today". Beta starts in a few weeks. If you want to test it and call out where we miss the mark, I'd genuinely value the feedback. Romuald Disclaimer: not financial advice, options trading involves substantial risk. -

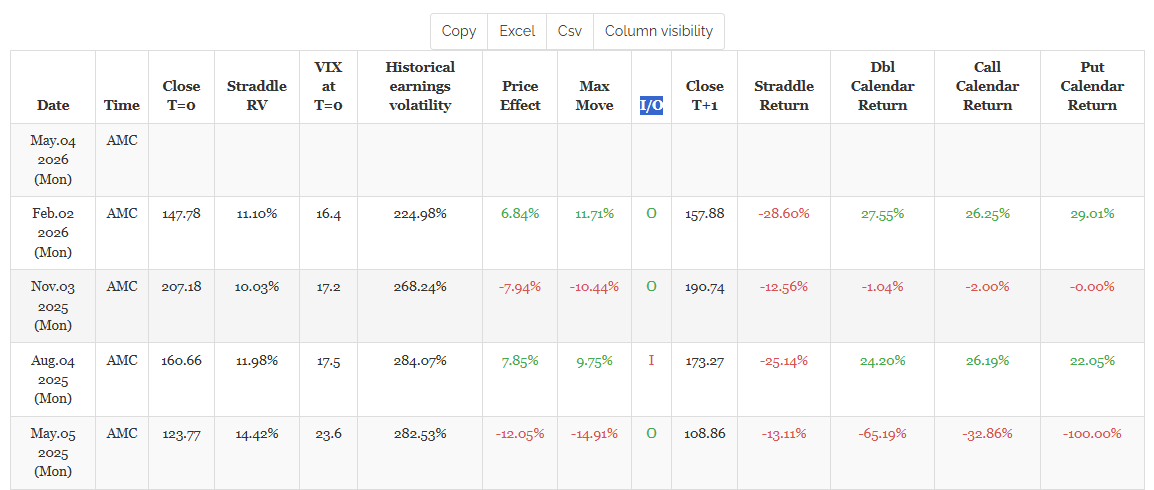

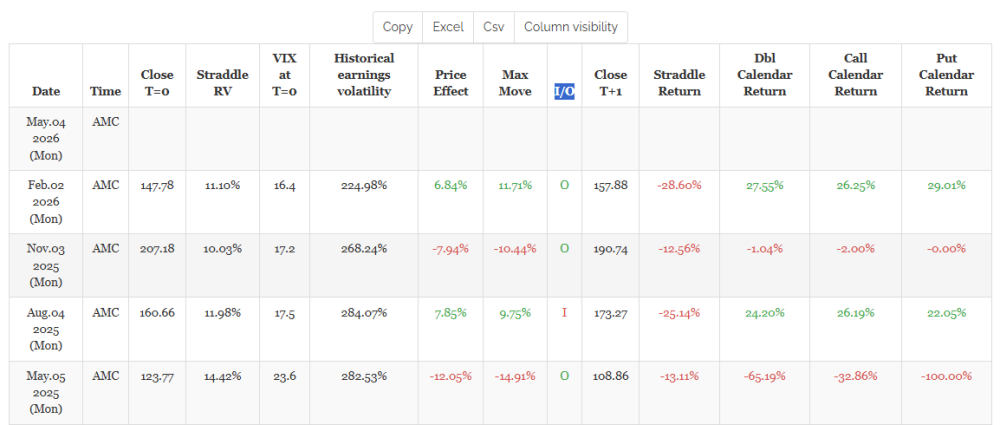

I/O is : I (inside) if absolute value(max_move) < straddle RV, else it's O (outside).

-

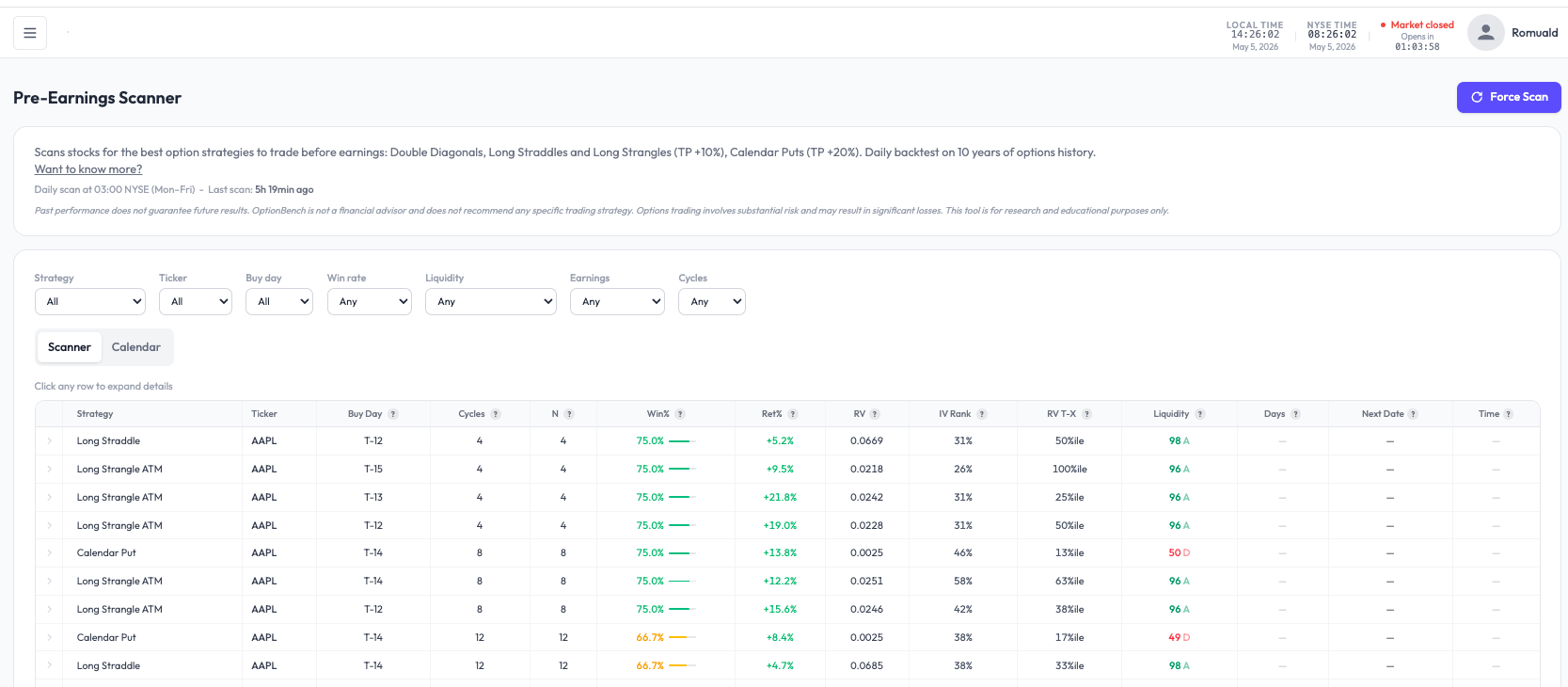

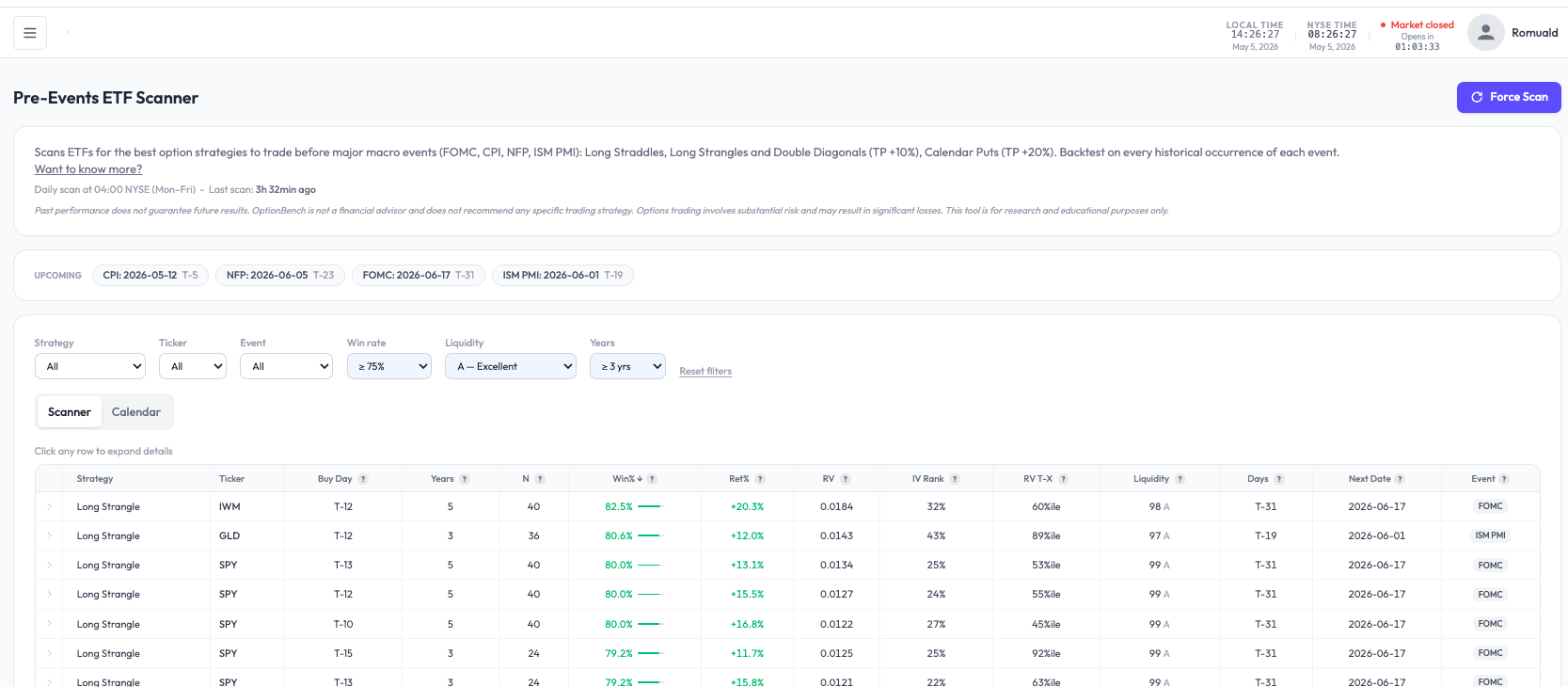

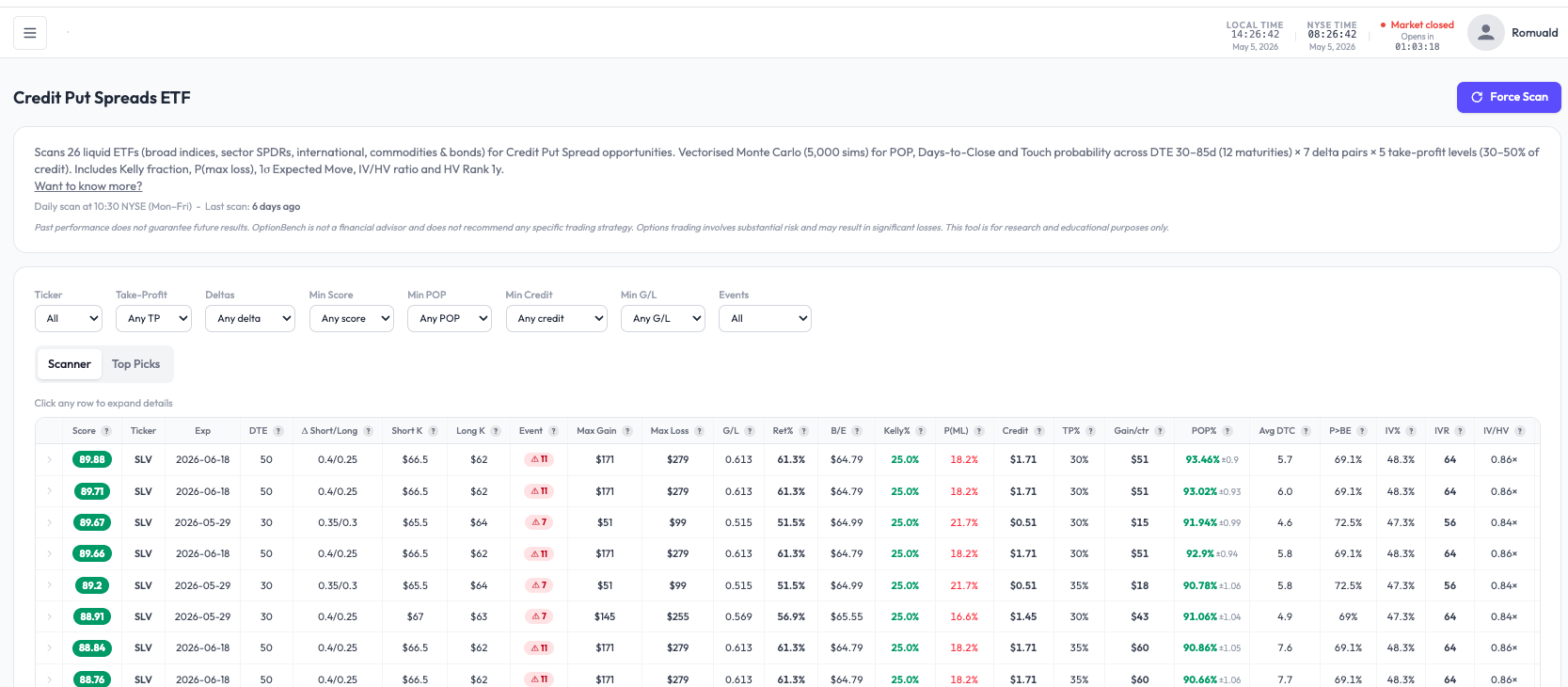

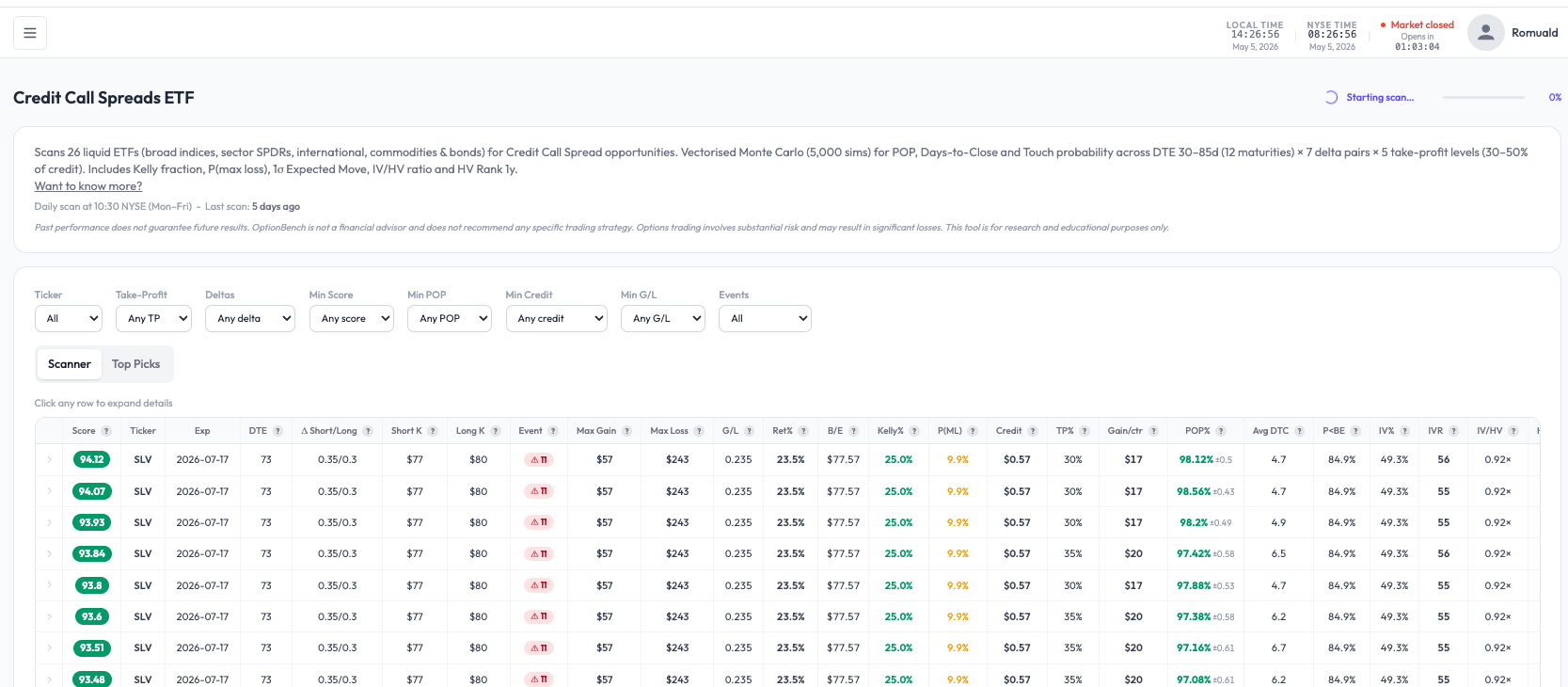

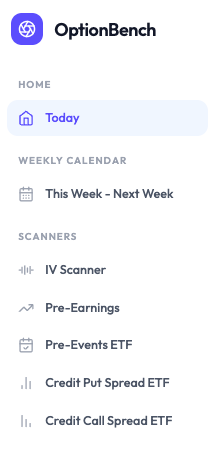

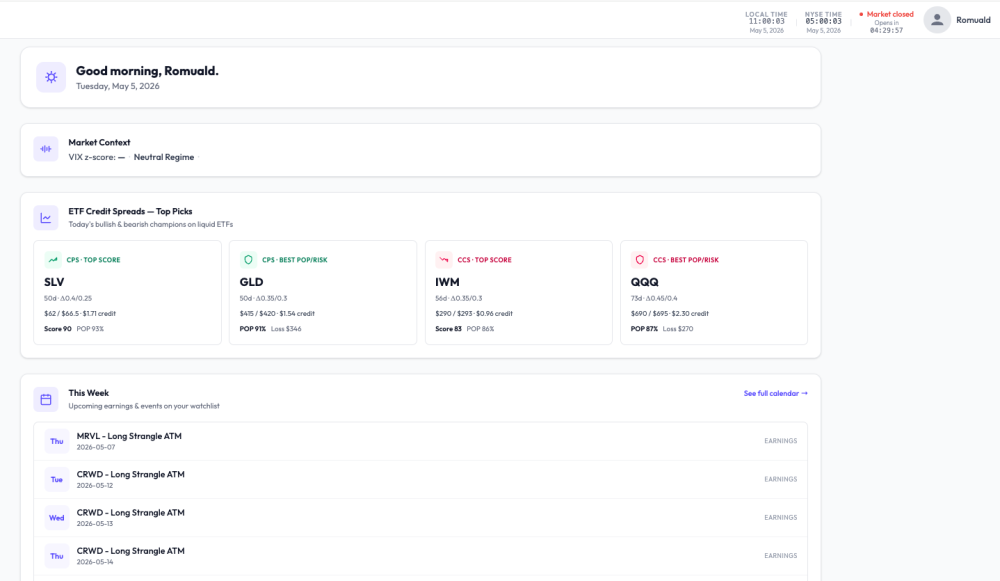

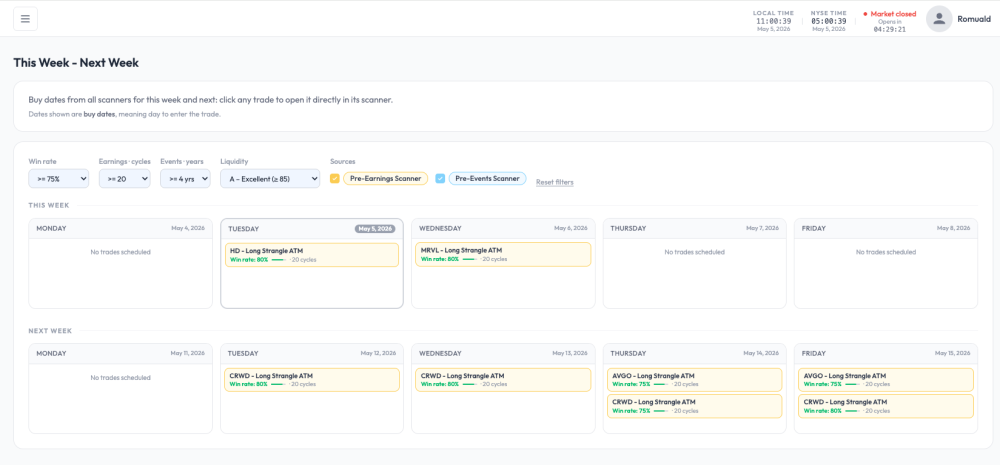

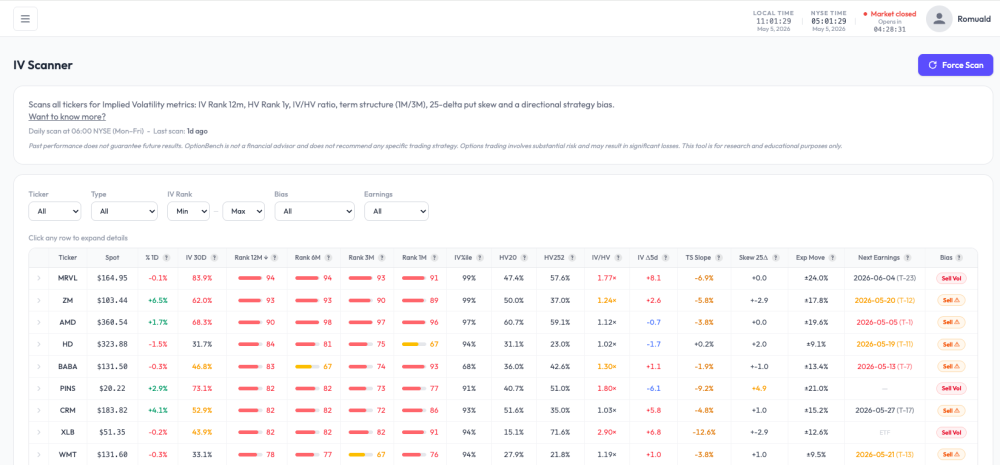

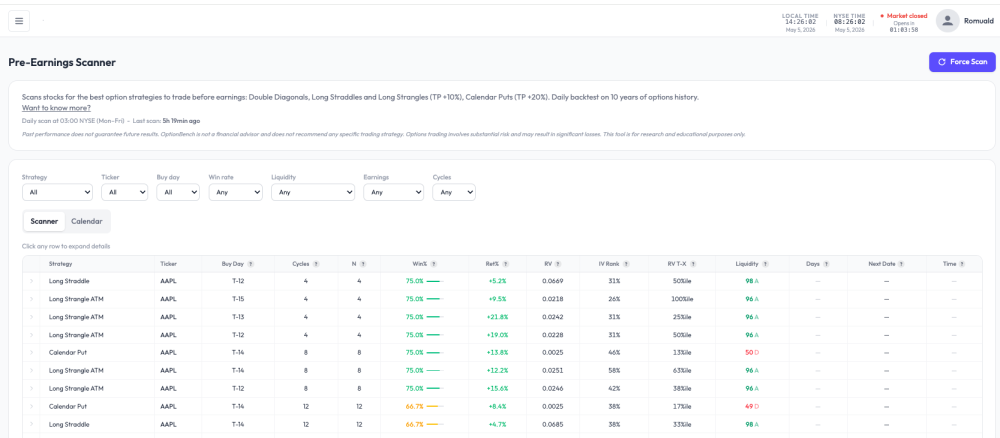

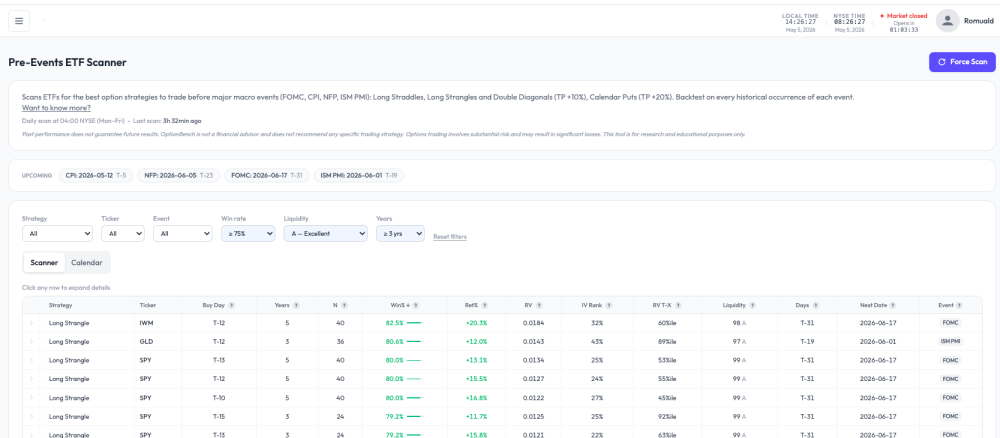

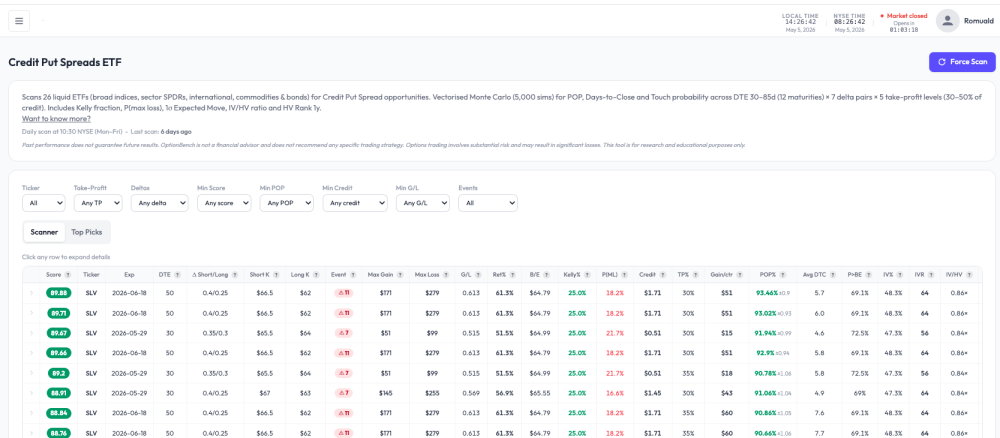

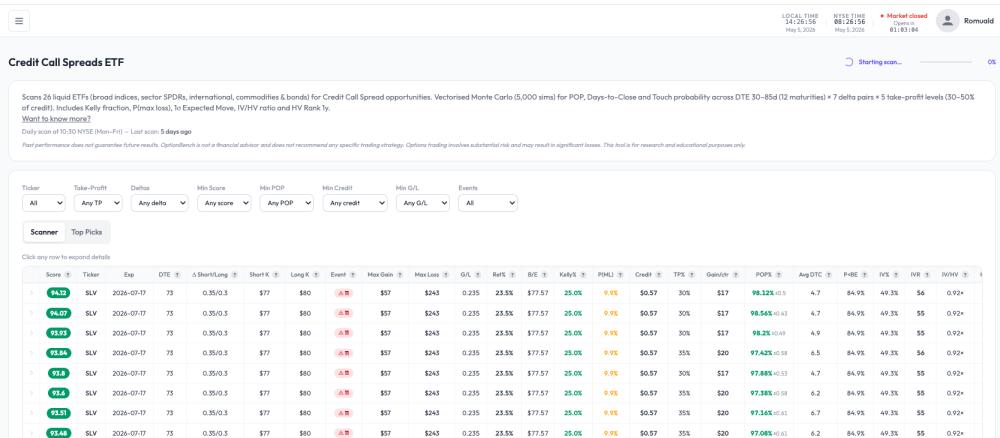

Hi all, I'm Romuald, an options trader and member of SO. Over the past several months I've been building a scanner suite called OptionBench, primarily to scratch my own itch — I wanted a tool that surfaces credit-spread and pre-earnings setups with transparent methodology, without hype and signal-service noise. Then, in the future V2 version of the tool, there will be a powerful and fast options-strategies-backtester. Public launch is targeted for June 2026. Before that, I'd like to (1) show the community what it does, (2) get critical feedback from people who actually trade options seriously, and (3) recruit a small group of beta-testers who'll get free access during the beta phase. What OptionBench does — V1 In the V1 there will be five scanners, a "Today" landing dashboard, and a two-week trade calendar. The UI is intentionally sober — no flashy graphics, no countdown timers, no upsell pop-ups. "Today" dashboard Single landing view with the day's top CPS / CCS picks (Top Score + Best POP/Risk for each side) and the upcoming earnings/events on your watchlist. Weekly calendar (This Week / Next Week) Buy-dates aggregated from all scanners across the current week and the next, filterable by win rate, cycles, years of history, and liquidity grade. Click any cell to jump straight to the underlying scanner row. The five scanners 1. IV Scanner Scans ~100 tickers daily for IV Rank 12m, HV Rank 1y, IV/HV ratio, term structure (1M/3M), 25-delta put skew, and a directional bias signal. Useful for premium-selling candidate selection. 2. Pre-Earnings Scanner For tickers with upcoming earnings, runs historical analogues across Long Straddle, Long Strangle ATM, Double Diagonals and Calendar Put strategies (TP +10% / +20%). Roughly 10 years of options history, win rate by buy-day (T-15 to T-1), Ret%, RV, IV Rank, liquidity grade. 3. Pre-Events ETF Scanner Same idea but for ETFs around macro events: FOMC, CPI, NFP, ISM PMI. Backtest on every historical occurrence of each event. Shows upcoming dates with T-X countdowns and ranks setups by win rate, Ret%, and liquidity. 4. Credit Put Spreads ETF (CPS) 26 liquid ETFs (broad indices, sector SPDRs, international, commodities, bonds). Vectorised Monte Carlo (5,000 sims) for POP, Days-to-Close, and Touch probability. 5. Credit Call Spreads ETF (CCS) Mirror of CPS for bearish setups. Same universe, same engine, same metrics. Beta-tester recruitment I'm looking for a small group (target ~10–20 people) of active options traders to use OptionBench during the beta phase, free of charge, in exchange for substantive feedback — what's broken, what's missing, what's misleading, what would make you stop using your current scanner, what would make you switch. If you'd like in: send me a PM with your email address and a one-line note on what you currently trade (credit spreads, pre-earnings, premium selling, IV plays, etc.) so I can balance the cohort across use cases. Not interested in the beta but want to be notified at launch? You can leave your email directly on the site: https://www.optionbench.com (waitlist form on the homepage — no spam, just a launch ping). And — if you have feedback, objections, or features you'd want to see in V1, I'd genuinely rather hear it now than after launch. Reply here or PM, both work. Critical feedback especially welcome. Thanks for reading. — Romuald Past performance does not guarantee future results. OptionBench is not a financial advisor and does not recommend any specific trading strategy. Options trading involves substantial risk and may result in significant losses. This tool is for research and educational purposes only.

-

I don't recall any execution issues.

-

@Djtux Is I/O column (that implies if the move was inside or outside Straddle RV), does it consider Max Move Column to make that determination? Or the move at Market Open after earnings because sure looks like it is not based on Price Effect (which is at close?)

-

Thank you for responding. Did you notice any differences while you were designated a professional? Were fills the same or did orders just sit there?

-

Yes, it happened to me some years ago with IB. I forget the details but I think they put me on professional rates the following month or two, until I went through a period of trading below the threshold and was able to revert to non-professional status again.