All Activity

- Today

-

Sasquatch joined the community

Sasquatch joined the community - Yesterday

-

LIANPR joined the community

LIANPR joined the community - Last week

-

amangalore joined the community

amangalore joined the community -

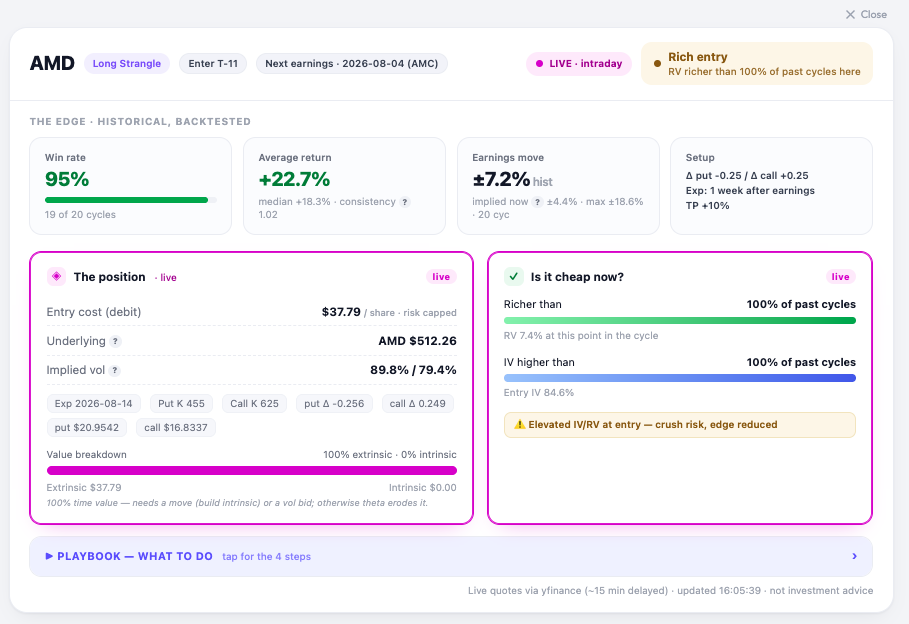

Update — at the open Markets opened, and here's AMD live: the strangle re-priced from $38.69 to $37.79, AMD gapped up to $512, and entry IV eased from ~87% to 84.6%. Marginally cheaper — but the verdict didn't budge: still "Rich entry," still richer than 100% of past cycles, still flagged for crush risk. On the charts, the live-value diamonds sit at the very top of every panel — value, relative value, and IV. Translation: the setup got a little bit cheaper, not cheap. It never dropped into its normal P25–P75 band, so the disciplined read is unchanged. Personnally I would pass, and let the backtest stay a backtest for this cycle. That's the tool doing its job: a 95% historical win rate is only worth having if you don't overpay to get in, from my POV. Romuald - OptionBench

Update — at the open Markets opened, and here's AMD live: the strangle re-priced from $38.69 to $37.79, AMD gapped up to $512, and entry IV eased from ~87% to 84.6%. Marginally cheaper — but the verdict didn't budge: still "Rich entry," still richer than 100% of past cycles, still flagged for crush risk. On the charts, the live-value diamonds sit at the very top of every panel — value, relative value, and IV. Translation: the setup got a little bit cheaper, not cheap. It never dropped into its normal P25–P75 band, so the disciplined read is unchanged. Personnally I would pass, and let the backtest stay a backtest for this cycle. That's the tool doing its job: a 95% historical win rate is only worth having if you don't overpay to get in, from my POV. Romuald - OptionBench

-

@Romuald these revisions are a great step forward keep them coming

@Romuald these revisions are a great step forward keep them coming -

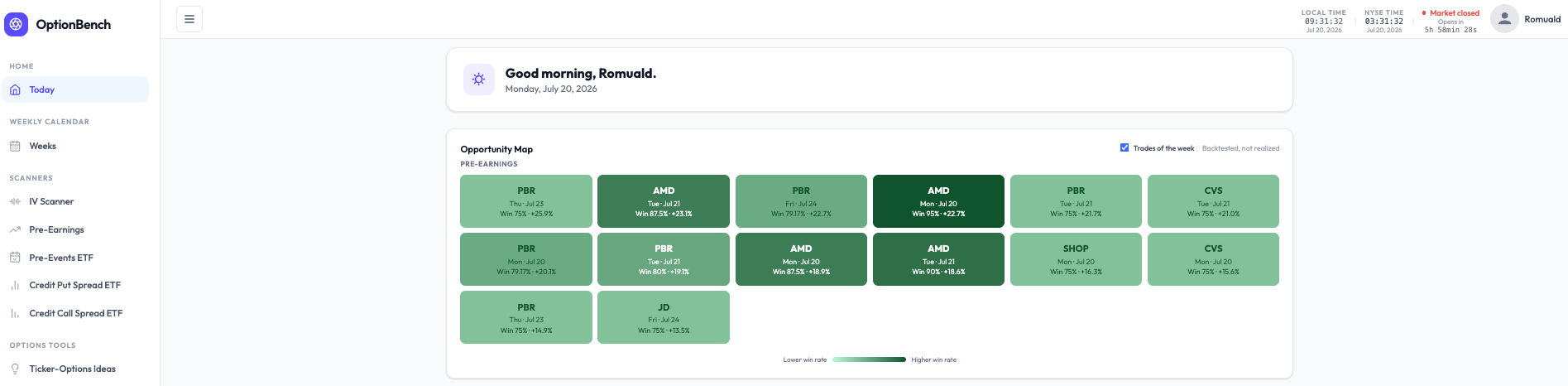

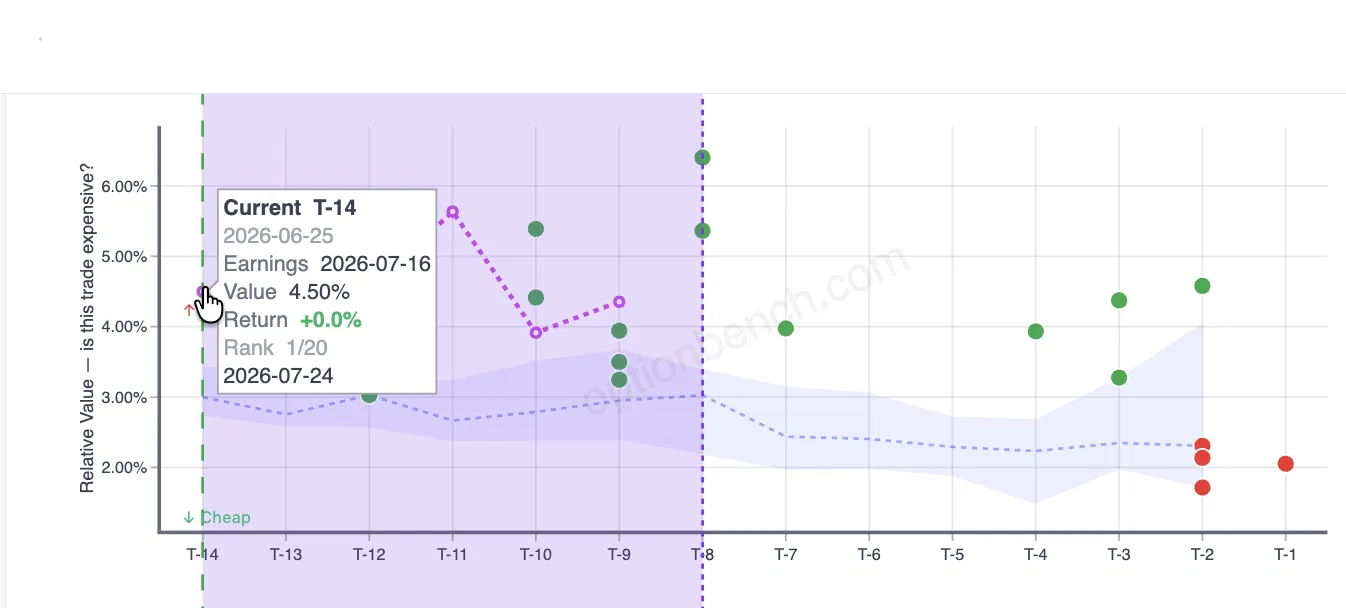

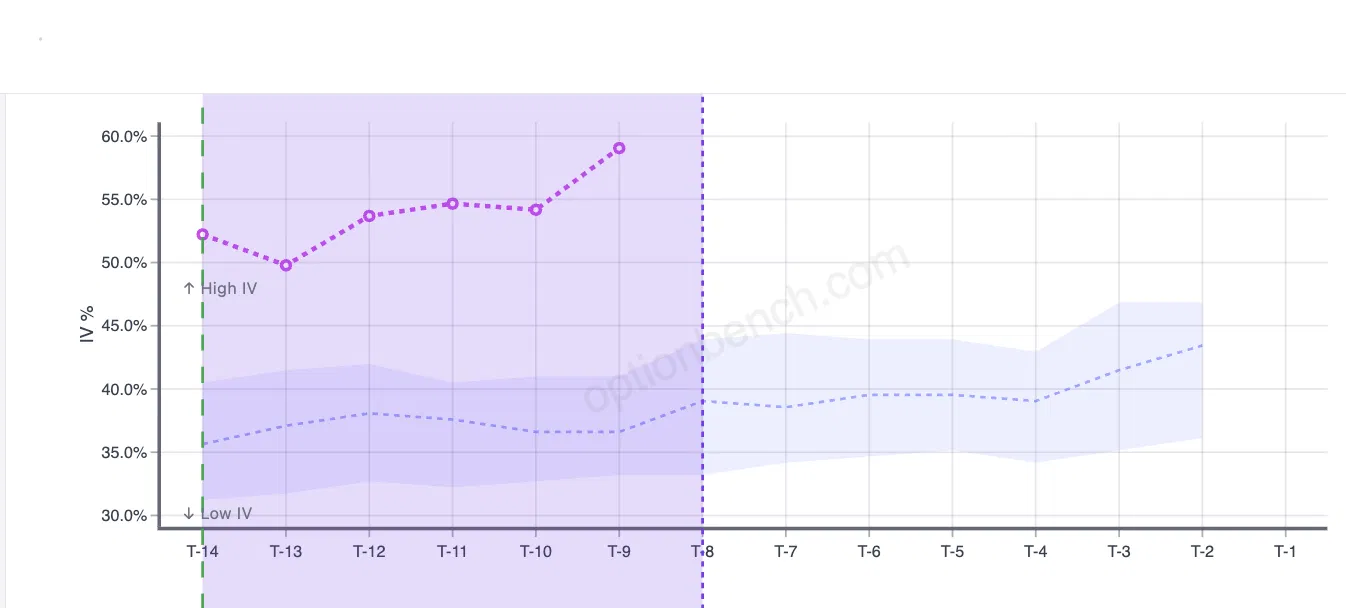

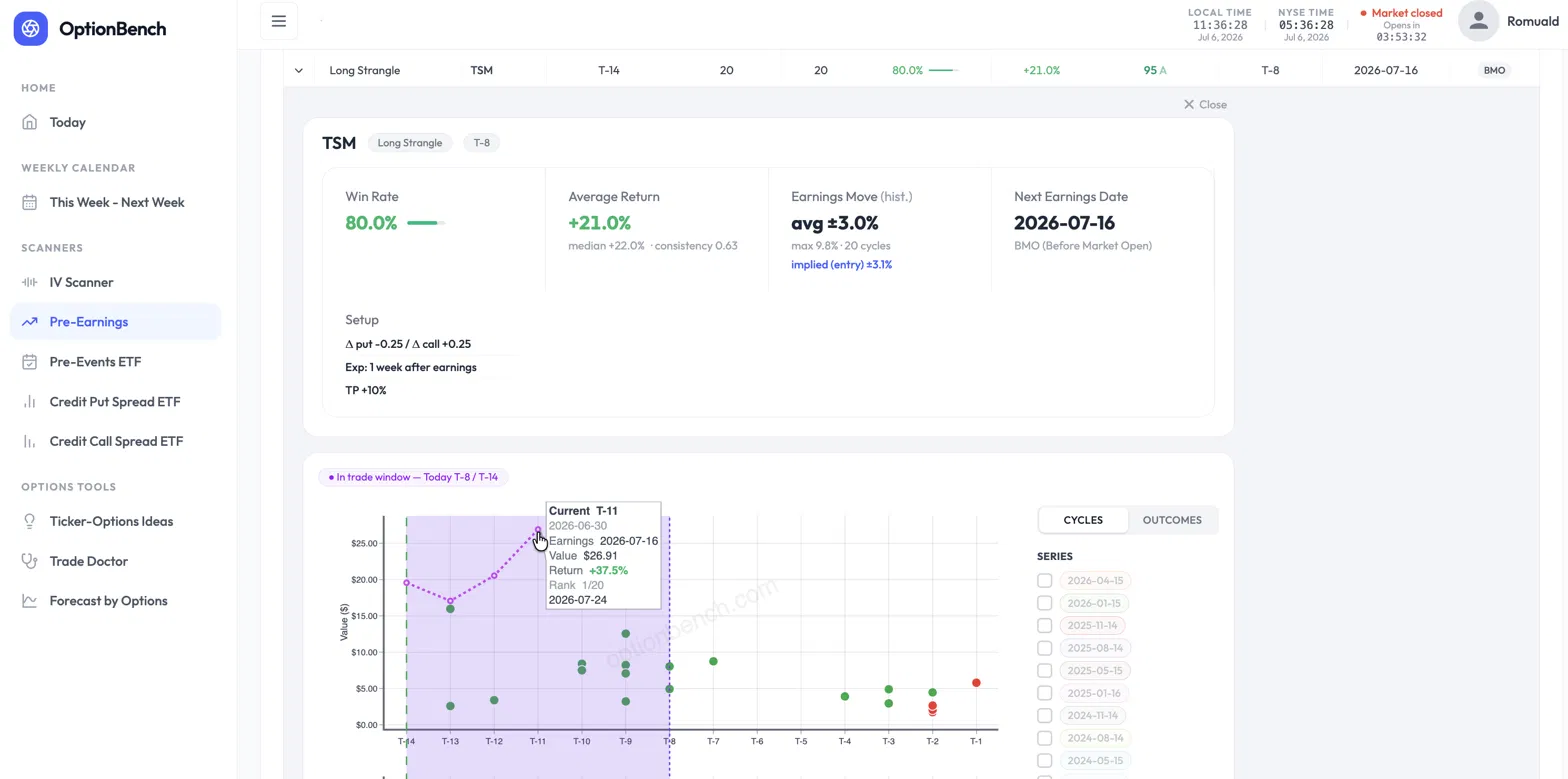

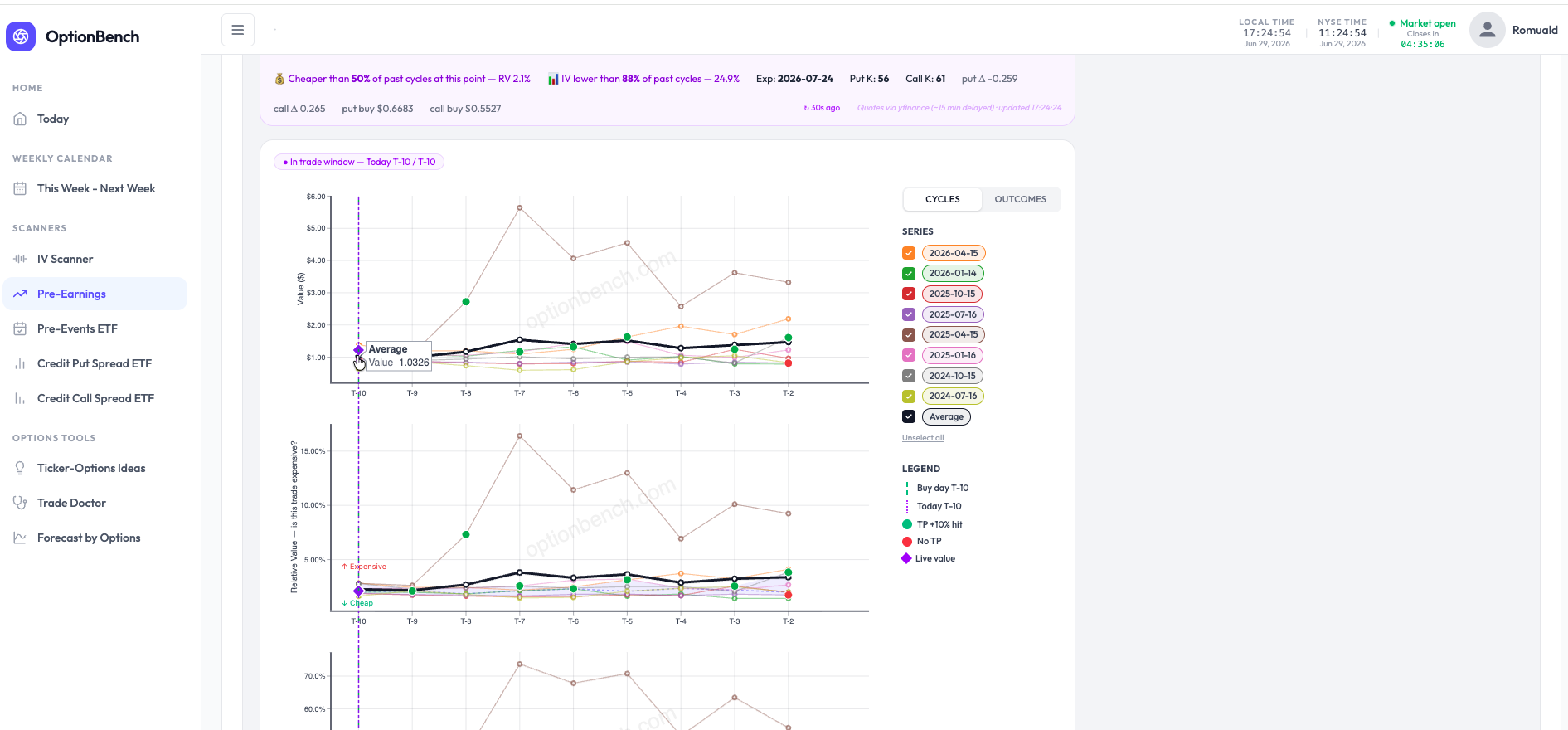

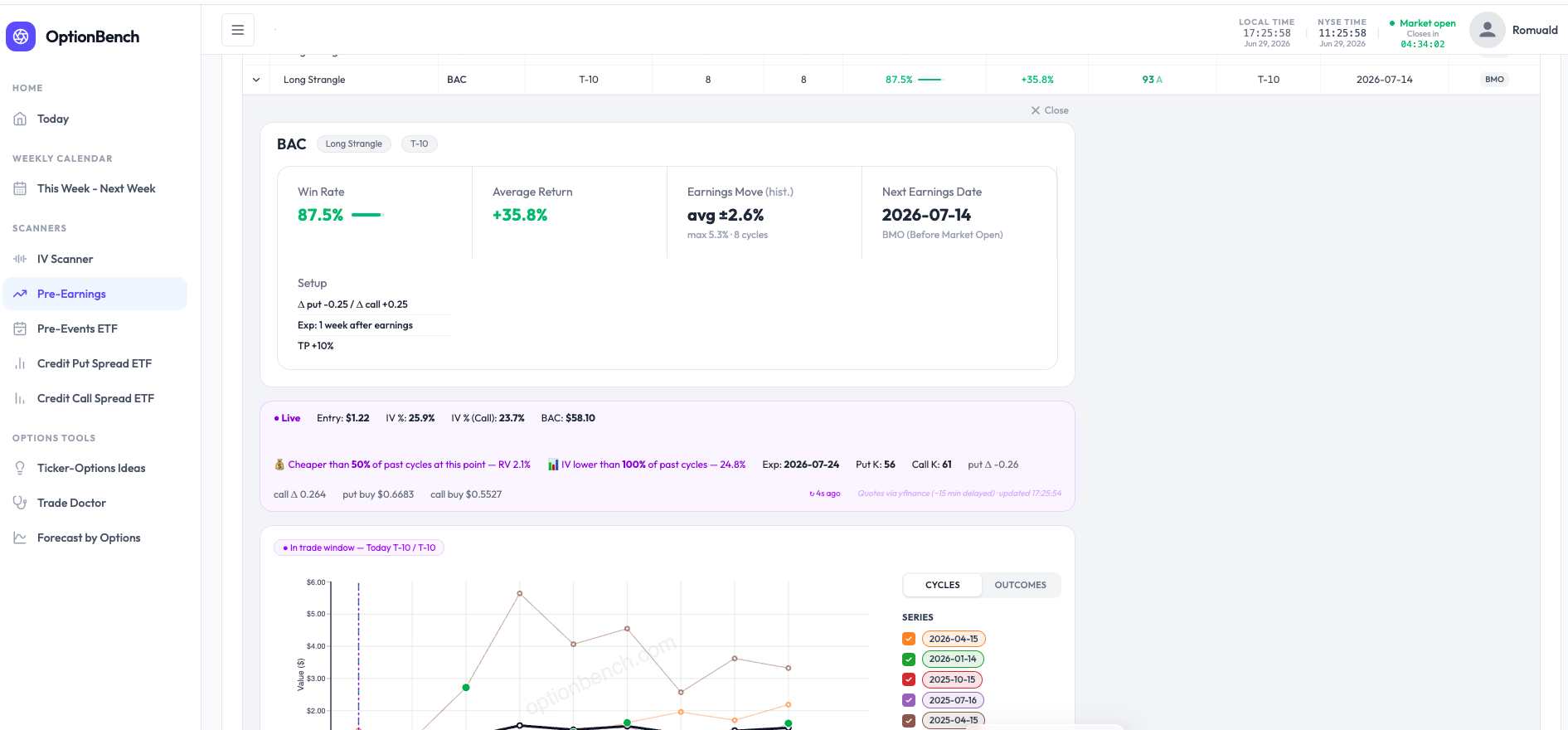

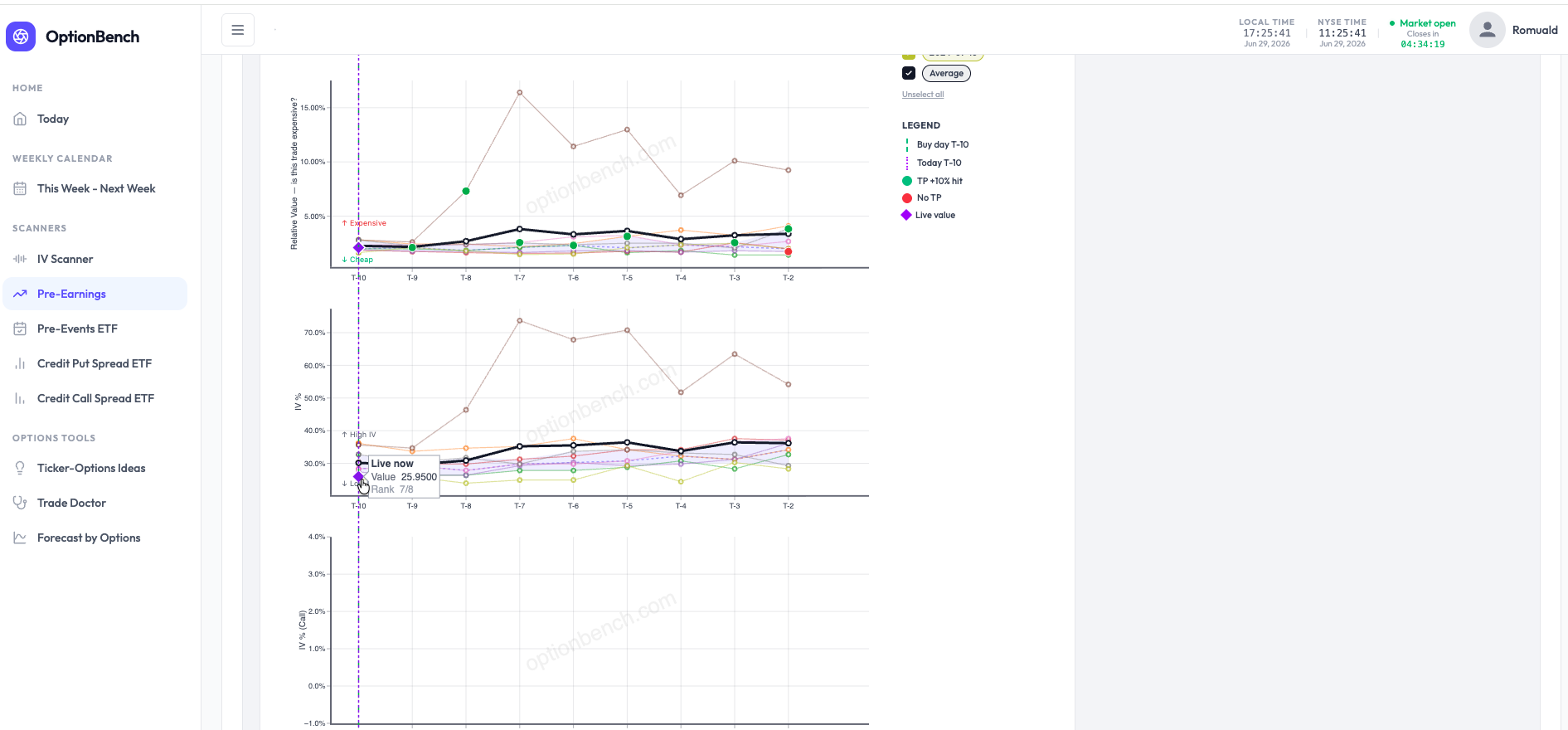

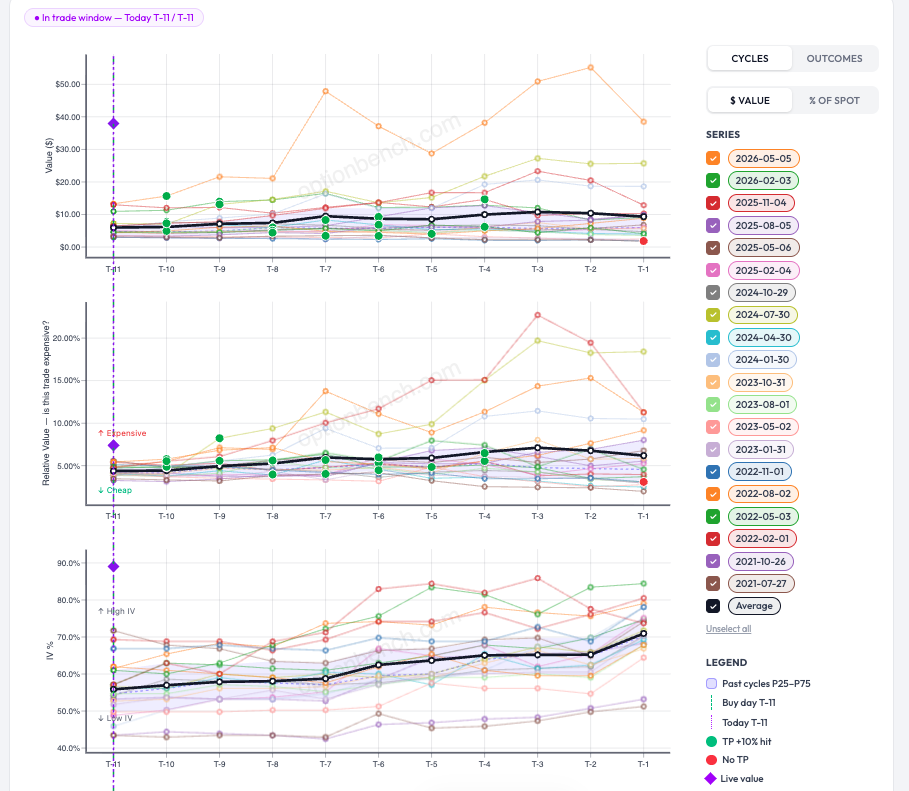

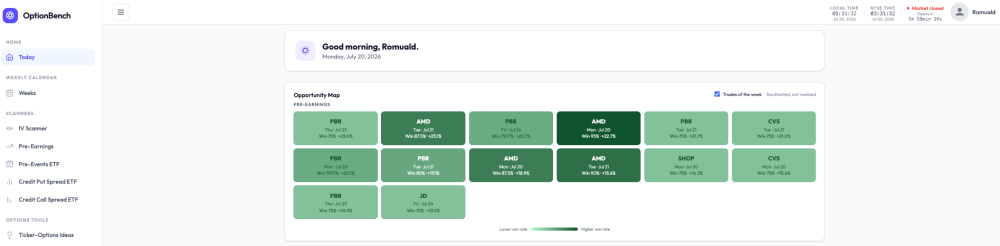

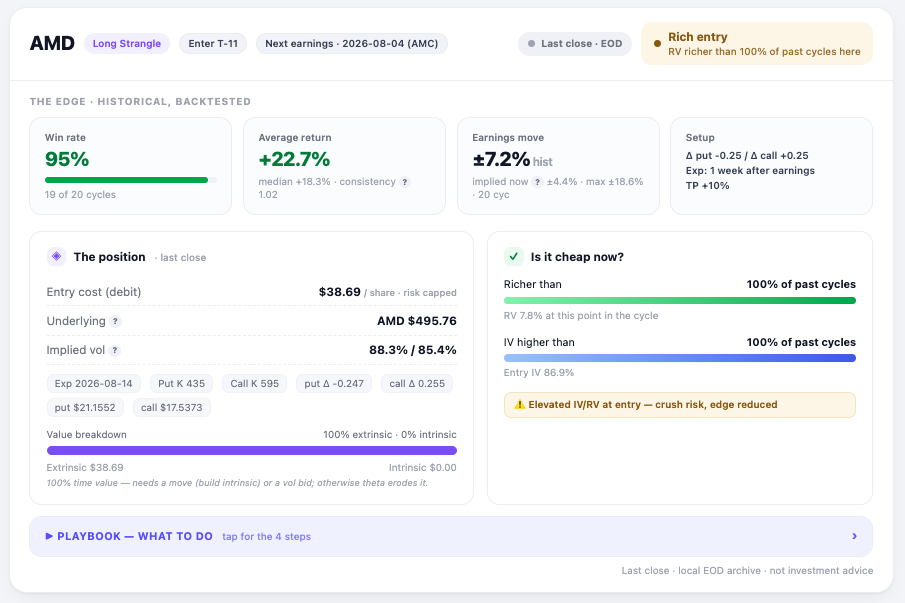

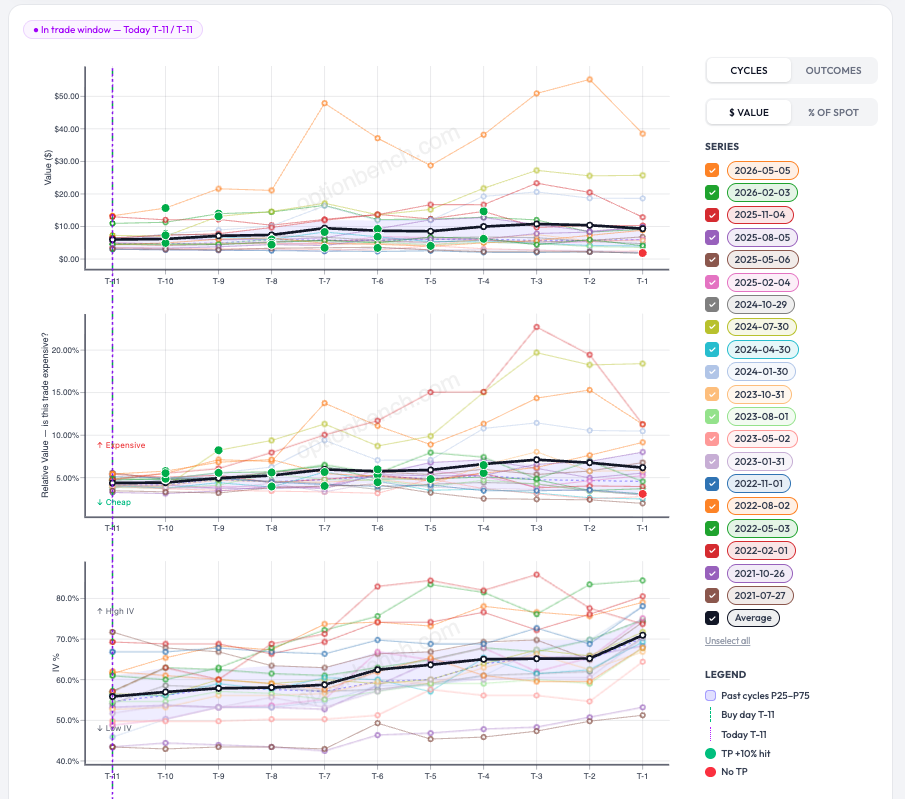

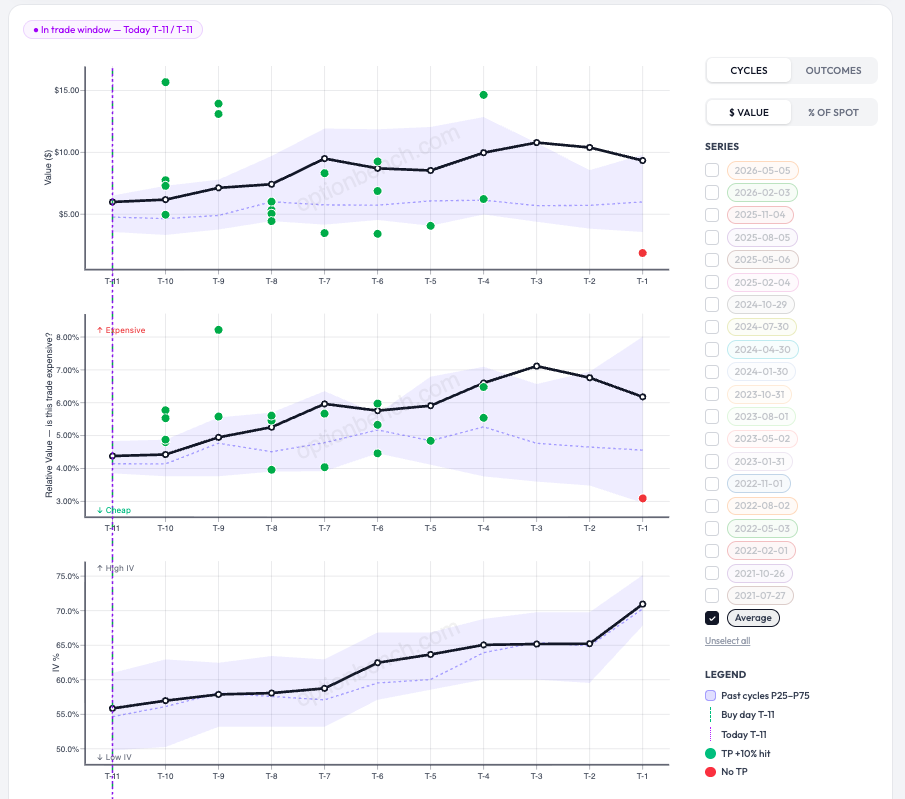

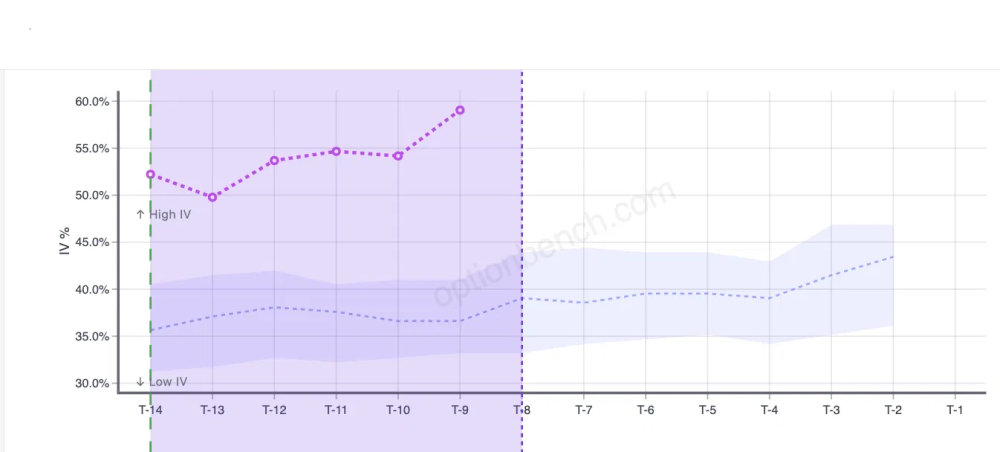

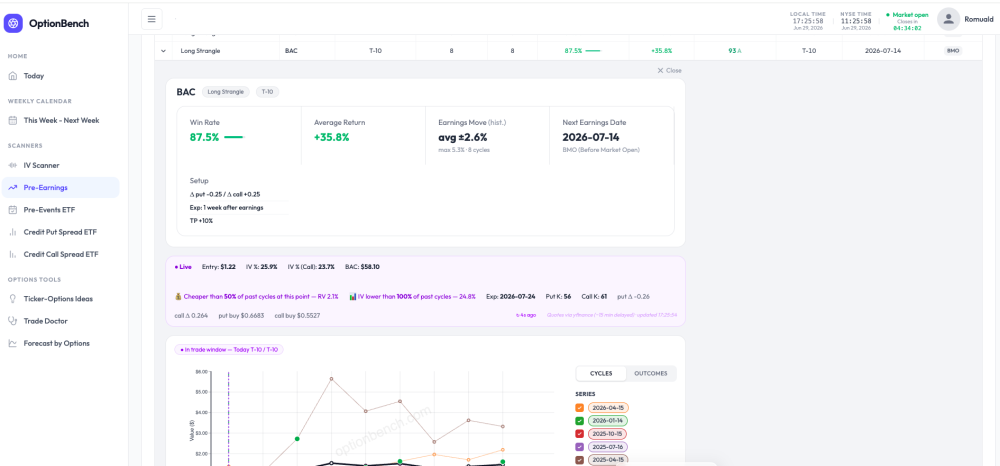

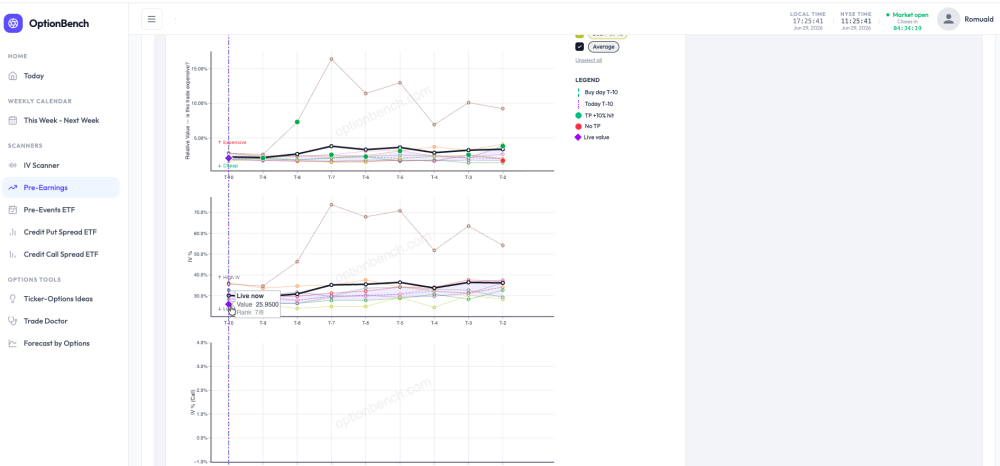

From a Green Tile to a Trade Decision: Inside OptionBench's Pre-Earnings Workflow Most screeners hand you a list. OptionBench hands you a decision — and then argues with you about it. Here's how that works, walking through a real setup on AMD. Start on the map The Today page opens on an Opportunity Map: where you can see one tile per backtested pre-earnings setup for the current week (or week ahead it it is the week-e,d). Each tile carries the ticker, the entry day, and two numbers: historical win rate and average return. The colour encodes the win rate: the darker the green, the more often the setup has worked across past earnings cycles. A "Trades of the week" toggle narrows the grid to the days just ahead, and the caption never lets you forget the key caveat: backtested, not realized. The darkest tile in this view is AMD — Mon, Jul 20 — Win 95% · +22.7%. Tempting. So we click it. One click into the analysis Clicking a tile doesn't dump you at the top of a table, it drops you straight onto that exact row in the scanner, ticker already in focus. For AMD, the setup is a long strangle entered eleven business days before the Aug 4 report and exited the latest about a week after, with a +10% take-profit. The top strip is the historical, backtested edge: a 95% win rate (19 of 20 cycles), a +22.7% average return, a +18.3% median, and a typical earnings move of ±7.2% versus ±4.4% implied today. On the backtest alone, this looks like one of the strongest setups on the board. The part that keeps you honest Here's where OptionBench stops cheerleading. The right-hand verdict reads "Rich entry — RV richer than 100% of past cycles here," and the cheapness panel flags elevated IV/RV at entry — crush risk, edge reduced. In plain terms: the strangle is currently more expensive than at any comparable point in its own history, so buying it now would mean overpaying for volatility, exactly how a great backtest quietly turns into a mediocre fill. One more detail to notice: the badge says "Last close · EOD." Markets are closed right now — it's Monday morning (in France), and the NYSE opens in about six hours — so every live number on the page is the last end-of-day snapshot, not a tradeable quote. The rich-entry read is real, but it's a photograph from Friday's close. The right move isn't to trade it. It's to wait for the open and see whether the morning re-prices the strangle cheaper, or confirms it's still rich. Reading the cycle charts To judge that, we drop into the cycle charts (next Figure). Three stacked panels track the trade from T-11 to T-1 (business days before earnings): the strangle's dollar value, its relative value (RV% — "is this trade expensive?"), and its implied volatility. Every faint line is one past earnings cycle; the bold black line is the average; green dots mark the cycles that hit the +10% target, red dots the ones that didn't. It's a lot to take in at once — so a single click ("unselect all," keep Average) strips it down to the essentials: the average path, the outcome dots, and a shaded band. What the shaded band means That band is the P25–P75 range — the middle 50% of past cycles at each point in the run-up. At every T-x day, we take all the historical cycles and shade from the 25th percentile up to the 75th; the dotted line running through it is the median (P50). Think of it as the setup's normal range. When today's live reading sits inside the band, the trade is priced about as usual; below it, cheaper than history; above it, richer than history. To be continued — at the open So AMD is a beautiful backtest with a currently rich entry, frozen at Friday's close. The interesting moment is only a few hours away: when the market opens, we'll watch whether the strangle cheapens back down into its normal band — and only then decide whether it's worth putting on. That's the whole idea. The map surfaces the opportunity; the analysis tells you whether today is a good day to take it. The discipline is in the gap between the two. See you at the open. Romuald - OptionBench Backtested results are historical and are not realized returns. Nothing here is investment advice. Figures: (1) Today — Opportunity Map · (2) AMD analysis header · (3) Full cycle charts · (4) Simplified view with the P25–P75 band.

-

Rick123 joined the community

Rick123 joined the community - Earlier

-

om6063577 joined the community

om6063577 joined the community -

SaSung Jung joined the community

SaSung Jung joined the community -

Unlocking EarningsStudy's Daily Screener The Daily Screener — one of EarningsStudy's most-used tools, and until now reserved for SO Contributors — is being opened up to all Subscribers, free of charge. If you've been curious what the Contributors have been working from each morning, this is it, and now it's yours too. What the Daily Screener does Every trading day, the Daily Screener surfaces the names with earnings on the immediate horizon and lays out how the market is pricing them across EarningsStudy's strategy models — straddles, calendars, strangles, iron flies, double diagonals, long options, and call debit spreads,... — in a single, sortable view. Instead of hunting name by name, you get the day's opportunity set on one screen, ready before the bell. A couple of things worth knowing It's a daily tool — check it daily. The screen is built around what's reporting now. It refreshes each trading day, so its value is in the habit: a quick morning look to see which setups are live before the window closes. Yesterday's screen isn't today's. It's built for comparison, not just a list. Each candidate is shown with strategy-level context and historical win-rate framing, so you're weighing setups against one another on their merits rather than reacting to a single number. If a name trades weekly options, you can fold those into the view as well. It's a research tool, not a signal service. The Daily Screener is there to sharpen your own judgment and point you toward setups worth a closer look — not to tell you what to trade. As always, do your own diligence before putting on any position. How to access it Already using EarningsStudy? The Daily Screener is now in your sidebar — just sign in and open it. Not signed up yet? Register at https://earningsstudy.com/ with the same email you use on SteadyOptions, and you'll have it alongside the rest of the core platform. This is exactly the kind of thing we set out to do with this partnership: take the tools that were once behind an extra tier and put them in the hands of the whole community. More to come. — The SteadyOptions Team

-

@Romuald no rush I'm sure there are other more pressing issues that need your attention ... good luck with the maintenance over the weekend

-

OK, in my (long...) todo list

-

Quick heads-up for anyone using or checking out OptionBench this weekend: app.optionbench.com will be in scheduled maintenance from this Friday 10th of July afternoon (France Time) through the weekend, back to normal Monday. We're doing a planned infrastructure migration on the backend — consolidating the data layer so the scanners run faster and cleaner as we grow. Nothing's broken; we'd just rather take it offline than serve half-migrated data. If you hit a maintenance page over the weekend, that's why — everything will be back Monday. If you were mid-analysis on something and want a hand once we're back up, just ping me and I'll help you pick it back up. Thanks for your patience — doing the plumbing properly now so the tool holds up as more of you come on board. — Romuald, OptionBench.com

-

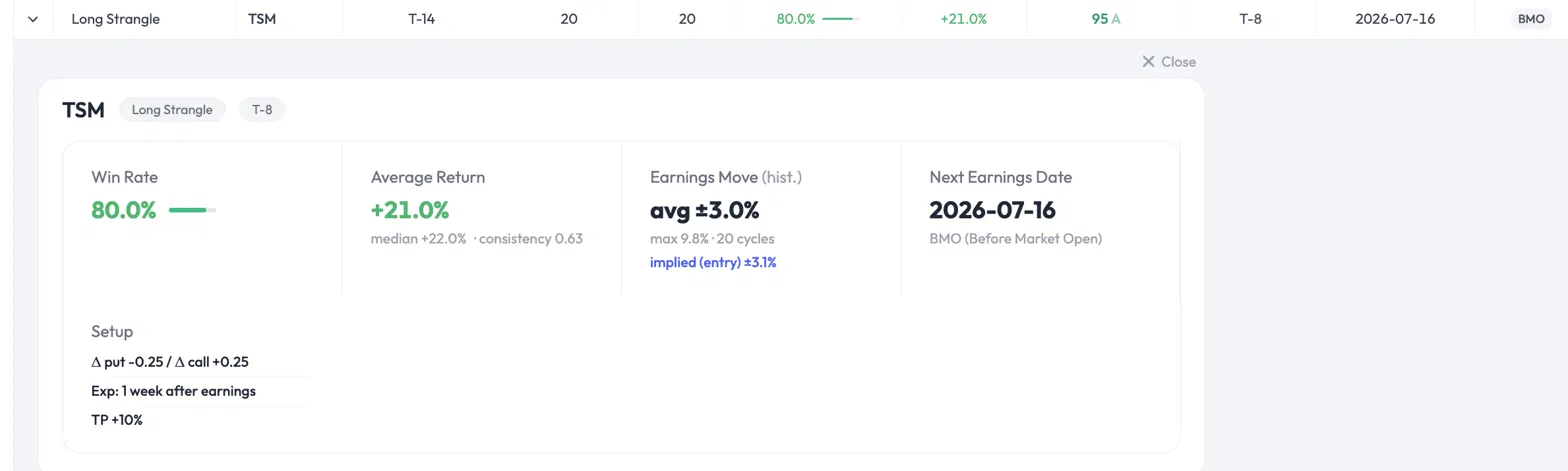

@Romuald thanks for sharing those thoughts .... I did consider both of them before jumping in .... the richness factor did concern me somewhat and I realize there may be a reduced edge due to that .... I also looked at the other cycles and well not as good as 8 cycles they were all still acceptable in my books as an aside is there anyway to pick more than one strategy in the scanner .. . it would be nice to be able to choose straddles and strangles together as they are closely related ... thanks for the words of thanks it has been a great ride thus far in being able to play a small role in the development of OB

-

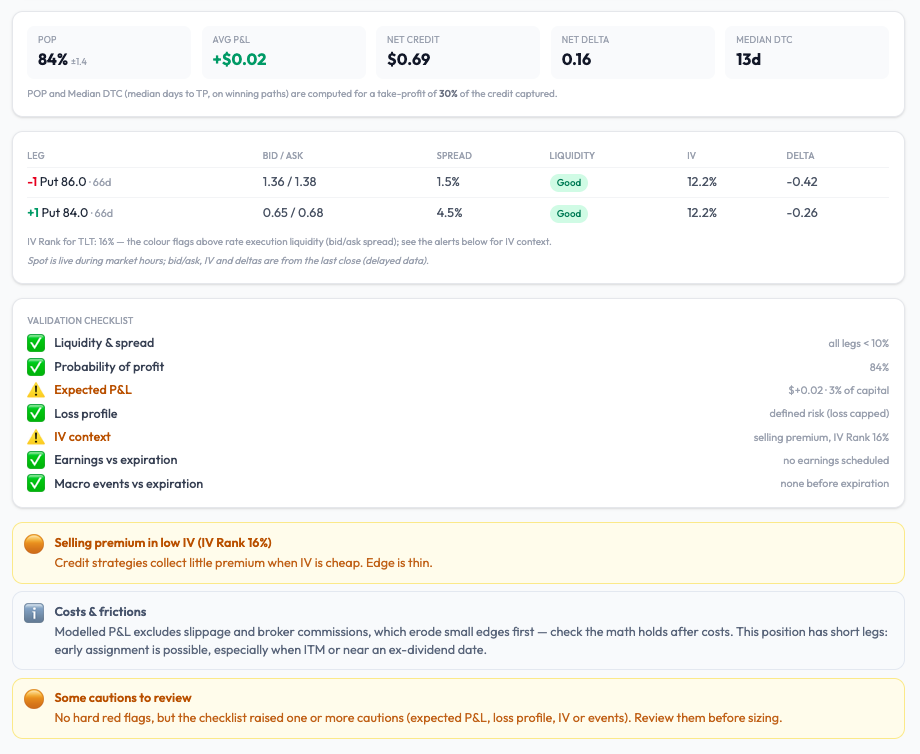

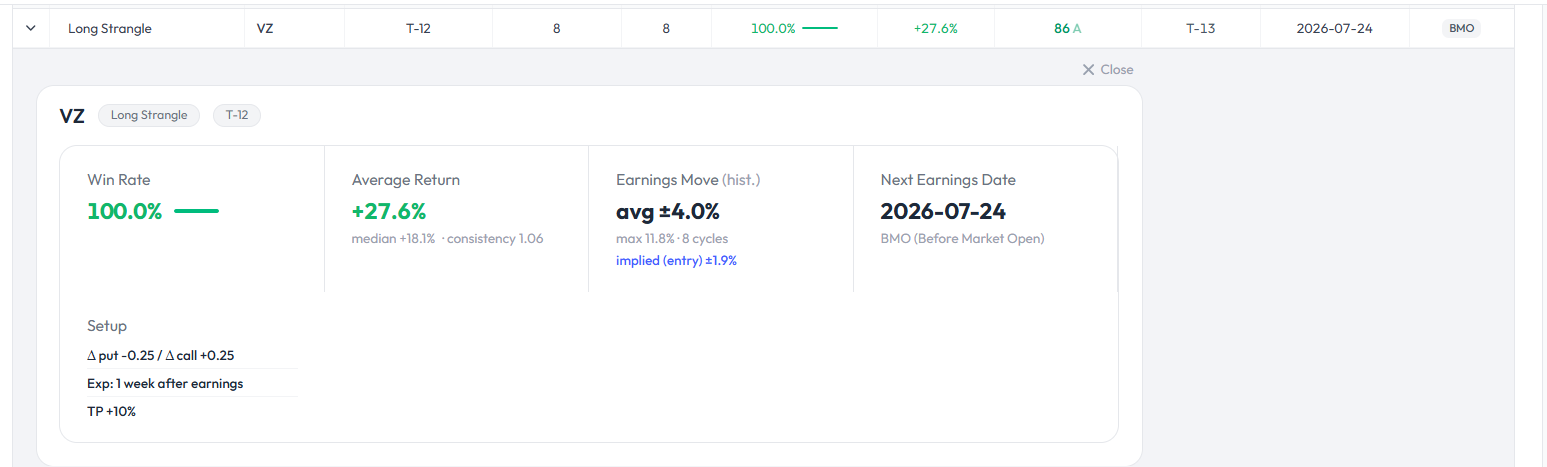

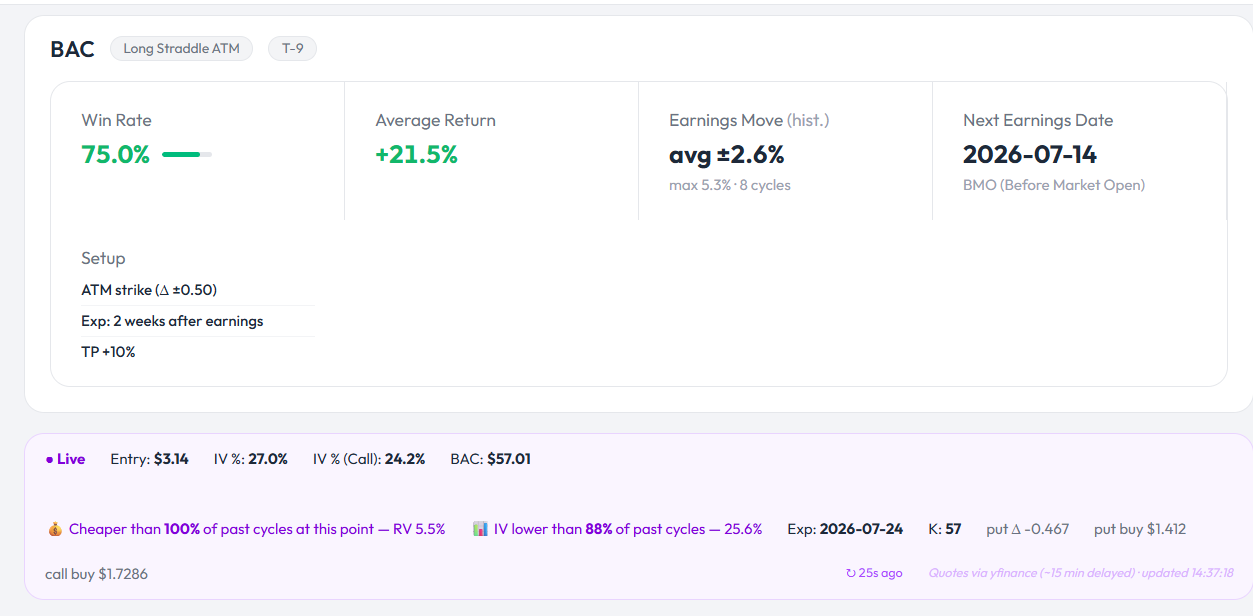

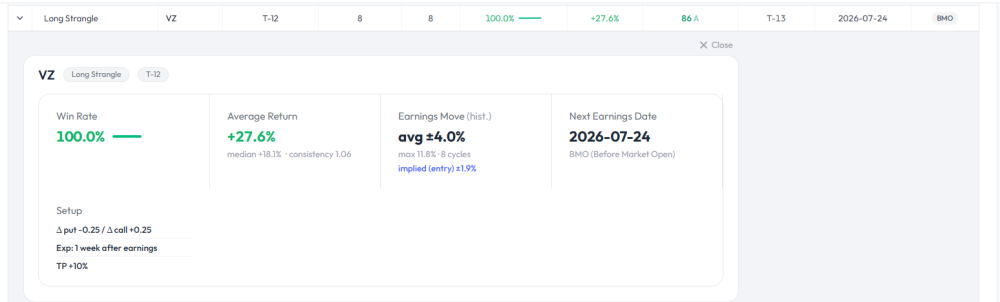

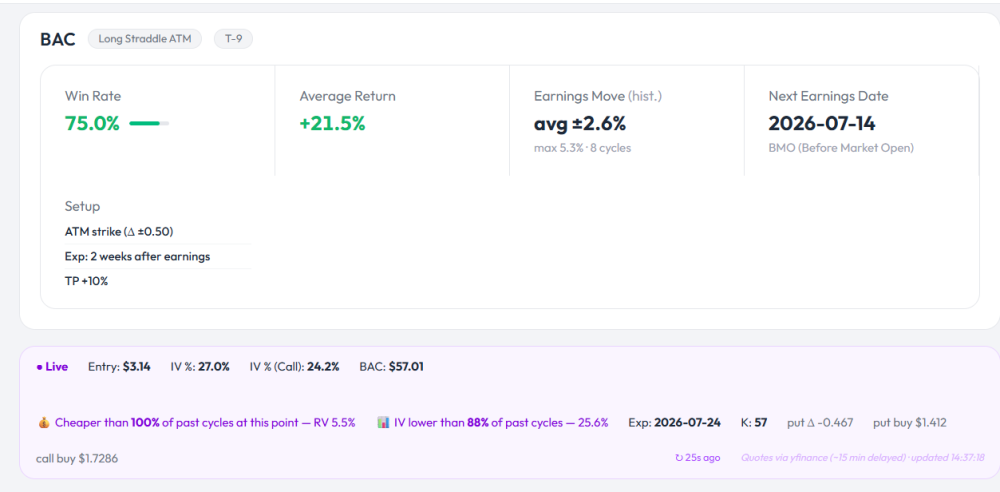

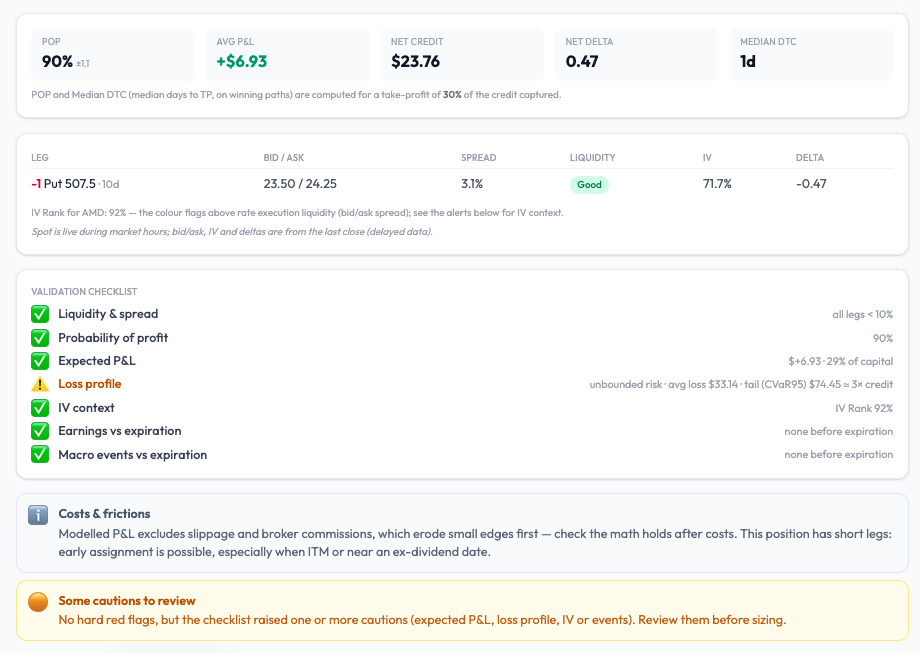

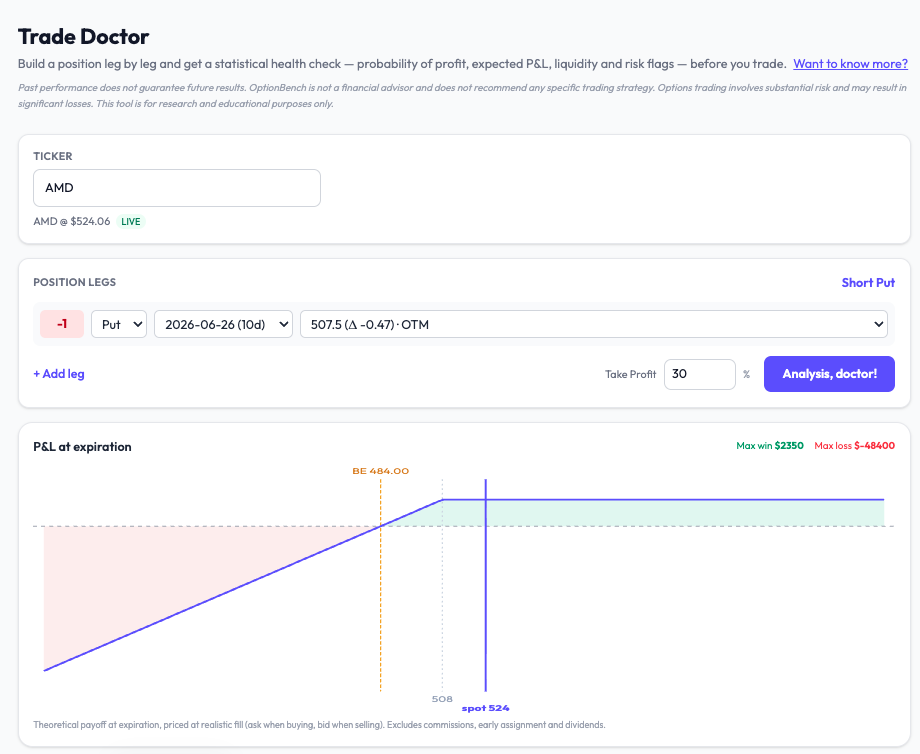

Hey Dave, first of all, thanks a lot for putting OptionBench through its paces and sharing your trades on Discord, it genuinely helps during the beta. On this VZ one, a couple of things I'd flag for how I read these cards — not a verdict on your trade, just the lens I use, but it is very personal. The 100% win rate is on 8 cycles. VZ only reports earnings four times a year, so 8 cycles is about two years of history — a small sample. A 100% rate on 8 is statistically fragile: the true rate underneath could be anywhere from ~65% to ~95%, you just can't tell from 8 observations. So I treat the headline number as "promising, low confidence" rather than a strong edge, and I lean harder on cycle counts of 20+ where the win rate actually stabilises. But, again, this is my POV. The other thing I personally always check before entering is the live banner — the "richer/cheaper than X% of past cycles" read. The historical win rate tells you the setup worked before; the live cheapness tells you whether you're entering at a good price right now. A great historical setup entered when the premium is rich can lose the edge to a vol crush even when the direction's right. So I wait to see that read before pulling the trigger. None of this means it won't work out — just how I'd weigh it. Really appreciate you testing and posting; keep them coming, this back-and-forth is exactly what makes the tool better :).

-

@Romuald time for another test drive VZ strangle

-

I've been exploring how AI can predict market changes. The potential of combining it with options trading looks promising for improving strategies by identifying trends early. What do others think?

-

For an active trader, those differences can add up to thousands of dollars a year. This article breaks down what actually separates the two, using concrete dollar examples, and gives you a simple framework for choosing the right instrument for your account and your strategy. Underlying Asset Differences: Index vs. ETF Options SPX is the S&P 500 index itself. It is a statistical construct, not a security — there are no shares to buy or sell. You can only trade options (and futures) on it, and those options settle in cash. SPY is the SPDR S&P 500 ETF. It holds the actual 500 stocks, trades like any share, and its options settle by delivering shares. That single distinction — cash settlement versus physical share delivery — cascades into almost every practical difference that follows: exercise style, assignment risk, contract size, and even how the two are taxed. SPX vs SPY Option Contract Sizes and Capital Requirements SPY trades at about one-tenth the level of the SPX index. With SPX near 7,500 and SPY near $750, the notional exposure of each contract looks like this: SPX SPY Approx. level 7,500 $750 Multiplier $100 100 shares Notional per contract ~$750,000 ~$75,000 One SPX contract carries roughly the same market exposure as ten SPY contracts. For a trader putting on size, that means fewer contracts, fewer commissions, and less execution complexity. For a smaller account, it means SPX can be too coarse — you may only be able to hold one or two contracts where ten SPY contracts would let you scale in and out with precision. Settlement and exercise: European vs American SPX options are European-style. They can only be exercised at expiration, and they settle in cash. If you hold a long 5,900 call and SPX settles at 5,910, you simply receive $1,000 (10 points × the $100 multiplier). No shares ever change hands. SPY options are American-style. They can be exercised at any point before expiration, and in-the-money contracts result in shares being delivered or called away. For anyone trading multi-leg positions, this is bigger than it sounds. If you are short the body of an SPX iron condor or butterfly and the index blows through your strike intraday, nobody can exercise against you early — the position stays intact until expiration. With SPY, a short leg that goes deep in the money (especially around an ex-dividend date) can be assigned early, leaving you with an unwanted 100-share-per-contract stock position and a hedge that no longer lines up. Cash settlement removes that failure mode entirely. Section 1256 Tax Advantages of SPX Options This is where SPX earns its keep for active traders. SPX options are taxed more favorably than SPY options because they qualify as Section 1256 contracts. This subjects them to a 60% long-term and 40% short-term capital gains tax split, whereas SPY options are taxed at 100% short-term capital gains if held under a year. Even a 0DTE trade opened and closed in the same afternoon gets 60/40 treatment. Section 1256 positions are also marked to market at year-end, and wash-sale rules do not apply. SPY options are taxed like ordinary equity options. A trade held under a year is taxed 100% at your short-term (ordinary income) rate, and wash-sale rules do apply. Consider a trader with $20,000 of net options profit in a year, in a 32% marginal bracket with a 15% long-term rate: SPY (all short-term): $20,000 × 32% = $6,400 in tax. SPX (60/40): ($12,000 × 15%) + ($8,000 × 32%) = $1,800 + $2,560 = $4,360 in tax. Same trades, same market, roughly $2,000 saved — purely from the instrument you chose. For a high-volume premium seller, that gap compounds year after year. Tax treatment of options is complex and depends on your situation. Section 1256 generally applies to broad-based index options, but confirms applicability with a tax professional. Dividends: a wrinkle SPY carries and SPX doesn't SPY pays a quarterly dividend. Its price drops on the ex-dividend date, and market makers price that expected drop into the options — call premium tends to sag and put premium firms up ahead of the event. Deep in-the-money SPY calls also face elevated early-assignment risk right before the ex-dividend date, as holders exercise to capture the payout. SPX, being an index, pays no dividend and has no ex-dividend date. One less variable to track. Liquidity and spreads: it depends how you measure SPY options are the most actively traded options in the world. In absolute dollar terms they carry the tightest bid-ask spreads and offer the most granular strike selection, which suits smaller accounts and precise position sizing. SPX spreads look wider in dollar terms, but remember one SPX contract equals about ten SPY contracts — so on an apples-to-apples exposure basis the relative cost is competitive, and you are crossing the spread on one contract instead of ten. At-the-money SPX and SPXW strikes trade with deep liquidity and penny-wide markets during active sessions. A quick word on the ticker: SPX vs SPXW In your option chain you will see both SPX and SPXW. SPX (the classic monthly) is AM-settled — it stops trading Thursday and settles off Friday's opening prices, which introduces some overnight gap risk on the final day. SPXW covers the weekly and daily expirations and is PM-settled off the 4:00 PM close, so you can trade it right up to the bell. If you are trading 0DTE, you are in the SPXW chain. Both get identical Section 1256 tax treatment. XSP Options: The Mini-SPX Alternative to SPY XSP is the Mini-SPX option — it trades at one-tenth of the SPX level (comparable in size to SPY) but keeps SPX's cash settlement, European exercise, and Section 1256 tax treatment. In theory it is the best of both worlds for a smaller account that still wants the tax and assignment advantages. The catch is liquidity: XSP volume is far thinner than either SPX or SPY, so spreads are wider and fills are harder. Worth knowing about, worth checking the chain before you commit. How SPX and SPY Options Behave During a Flash Crash Everything above is theory until you watch it play out in a live position. On Friday, June 26, 2026 — during a jittery week in which JPMorgan (read more on that) had publicly warned of flash-crash risk in crowded AI names — the S&P 500 delivered a textbook demonstration of why the SPX-vs-SPY distinction matters. Right at the 4:00 PM close, a wave of sell orders hit thin liquidity. On a standard 1-minute line chart, nothing looked wrong: the line simply connects close-to-close, and the close held around 731 on SPY. But pull up the 1-minute candlestick chart for that final bar and the story changes completely — a tiny body around 731 with an enormous lower wick stabbing all the way down to 716.58, then recovering, all within a single closing minute. The volume bar on that candle dwarfed everything around it. That's the signature of a flash crash: a momentary liquidity air-pocket where a flood of orders blows through a thin book before buyers step back in and the close resolves. This is a closing-bell liquidity cascade — arguably the single most dangerous moment for this kind of event. At 4:00 PM, market-on-close imbalance orders execute, index rebalancing flows hit, and options-expiration settlement pressure peaks all at once. A large sell imbalance in that window can momentarily overwhelm the order book before the closing auction resolves. Here's where it gets instructive. That 716.58 print was SPY's worst individual tick. But the SPX cash index — pulled from live data — only printed down to about 7,336 in the same minute. At the roughly 10:1 ratio, SPY's 716.58 implies an SPX near 7,232, yet the actual index bottomed 100 points higher. Why the gap? During a flash crash, the ETF and the index decouple. SPY is a single instrument, so a market-sell order blows straight through its book and prints an extreme low. The SPX index, by contrast, is an average of all 500 constituents — and not every stock crashes to the same degree in the same instant. The index is "cushioned" by its own construction. The true dislocation sat somewhere between the two readings, with SPY overshooting to the downside. Now apply this to two hypothetical traders, each holding the same S&P 500 put spread going into that close: The SPY trader watched the ETF physically trade at 716.58 — potentially deep inside a danger zone — and, because SPY is American-style and physically settled, faced real assignment mechanics around any in-the-money strikes, plus the gut-punch of seeing the market trade through their level. The SPX trader settled off the official closing print near 7,354–7,357, determined by the closing auction — not the wick. Even the intraday SPX low of ~7,336 stayed above where an equivalent short strike would have sat. The terrifying wick, however real, never touched a cash-settled position that keys off the close. The lesson isn't that SPX is risk-free — that wick proves the market physically traded at a stressed level, and a stop-loss order resting in that zone would have been triggered, auction or not. The lesson is that cash settlement and European exercise changed the outcome. The same market event that could have been painful in SPY or in stock was, on a cash-settled SPX position, a non-event that expired off the official close. That is the structural edge described in the tax and settlement sections above, made concrete in a single closing minute. The decision framework Lean SPX if you: Trade meaningful size (one SPX replaces ten SPY, cutting commissions and complexity) Have enough capital and margin to handle the larger contract comfortably Run an active income strategy where the 60/40 tax treatment materially lowers your bill Want zero early-assignment risk on multi-leg structures Prefer the simplicity of cash settlement and no dividend exposure Lean SPY if you: Trade a smaller account and need granular position sizing Want the tightest absolute spreads and the widest strike selection Are building a strategy around actually holding shares (covered calls, cash-secured puts as accumulation) Are trading inside an IRA, where the Section 1256 tax edge is irrelevant Are newer to S&P 500 options and want to learn on a smaller, more familiar contract Consider XSP if you want SPX's tax and settlement benefits at a SPY-sized contract — and can live with thinner liquidity. The bottom line SPX and SPY track the same market, but they are not interchangeable. For a serious, active options trader — especially one selling premium or trading 0DTE at size — SPX's Section 1256 tax treatment, cash settlement, and freedom from early assignment give it a structural edge that compounds over time, in your fills and in your tax bill. SPY remains the better tool for smaller accounts, share-based strategies, and IRAs. Many experienced traders end up using both: SPX for tax-efficient premium selling at size, SPY for tactical trades and anything involving shares. The right answer isn't universal — it comes down to your account size, your tax situation, and the specific strategy in front of you. Choose the instrument that fits the trade, not the other way around. The examples above exclude commissions and fees and are for educational purposes only. Options trading involves substantial risk and is not suitable for every investor. Review the Characteristics and Risks of Standardized Options before trading.

For an active trader, those differences can add up to thousands of dollars a year. This article breaks down what actually separates the two, using concrete dollar examples, and gives you a simple framework for choosing the right instrument for your account and your strategy. Underlying Asset Differences: Index vs. ETF Options SPX is the S&P 500 index itself. It is a statistical construct, not a security — there are no shares to buy or sell. You can only trade options (and futures) on it, and those options settle in cash. SPY is the SPDR S&P 500 ETF. It holds the actual 500 stocks, trades like any share, and its options settle by delivering shares. That single distinction — cash settlement versus physical share delivery — cascades into almost every practical difference that follows: exercise style, assignment risk, contract size, and even how the two are taxed. SPX vs SPY Option Contract Sizes and Capital Requirements SPY trades at about one-tenth the level of the SPX index. With SPX near 7,500 and SPY near $750, the notional exposure of each contract looks like this: SPX SPY Approx. level 7,500 $750 Multiplier $100 100 shares Notional per contract ~$750,000 ~$75,000 One SPX contract carries roughly the same market exposure as ten SPY contracts. For a trader putting on size, that means fewer contracts, fewer commissions, and less execution complexity. For a smaller account, it means SPX can be too coarse — you may only be able to hold one or two contracts where ten SPY contracts would let you scale in and out with precision. Settlement and exercise: European vs American SPX options are European-style. They can only be exercised at expiration, and they settle in cash. If you hold a long 5,900 call and SPX settles at 5,910, you simply receive $1,000 (10 points × the $100 multiplier). No shares ever change hands. SPY options are American-style. They can be exercised at any point before expiration, and in-the-money contracts result in shares being delivered or called away. For anyone trading multi-leg positions, this is bigger than it sounds. If you are short the body of an SPX iron condor or butterfly and the index blows through your strike intraday, nobody can exercise against you early — the position stays intact until expiration. With SPY, a short leg that goes deep in the money (especially around an ex-dividend date) can be assigned early, leaving you with an unwanted 100-share-per-contract stock position and a hedge that no longer lines up. Cash settlement removes that failure mode entirely. Section 1256 Tax Advantages of SPX Options This is where SPX earns its keep for active traders. SPX options are taxed more favorably than SPY options because they qualify as Section 1256 contracts. This subjects them to a 60% long-term and 40% short-term capital gains tax split, whereas SPY options are taxed at 100% short-term capital gains if held under a year. Even a 0DTE trade opened and closed in the same afternoon gets 60/40 treatment. Section 1256 positions are also marked to market at year-end, and wash-sale rules do not apply. SPY options are taxed like ordinary equity options. A trade held under a year is taxed 100% at your short-term (ordinary income) rate, and wash-sale rules do apply. Consider a trader with $20,000 of net options profit in a year, in a 32% marginal bracket with a 15% long-term rate: SPY (all short-term): $20,000 × 32% = $6,400 in tax. SPX (60/40): ($12,000 × 15%) + ($8,000 × 32%) = $1,800 + $2,560 = $4,360 in tax. Same trades, same market, roughly $2,000 saved — purely from the instrument you chose. For a high-volume premium seller, that gap compounds year after year. Tax treatment of options is complex and depends on your situation. Section 1256 generally applies to broad-based index options, but confirms applicability with a tax professional. Dividends: a wrinkle SPY carries and SPX doesn't SPY pays a quarterly dividend. Its price drops on the ex-dividend date, and market makers price that expected drop into the options — call premium tends to sag and put premium firms up ahead of the event. Deep in-the-money SPY calls also face elevated early-assignment risk right before the ex-dividend date, as holders exercise to capture the payout. SPX, being an index, pays no dividend and has no ex-dividend date. One less variable to track. Liquidity and spreads: it depends how you measure SPY options are the most actively traded options in the world. In absolute dollar terms they carry the tightest bid-ask spreads and offer the most granular strike selection, which suits smaller accounts and precise position sizing. SPX spreads look wider in dollar terms, but remember one SPX contract equals about ten SPY contracts — so on an apples-to-apples exposure basis the relative cost is competitive, and you are crossing the spread on one contract instead of ten. At-the-money SPX and SPXW strikes trade with deep liquidity and penny-wide markets during active sessions. A quick word on the ticker: SPX vs SPXW In your option chain you will see both SPX and SPXW. SPX (the classic monthly) is AM-settled — it stops trading Thursday and settles off Friday's opening prices, which introduces some overnight gap risk on the final day. SPXW covers the weekly and daily expirations and is PM-settled off the 4:00 PM close, so you can trade it right up to the bell. If you are trading 0DTE, you are in the SPXW chain. Both get identical Section 1256 tax treatment. XSP Options: The Mini-SPX Alternative to SPY XSP is the Mini-SPX option — it trades at one-tenth of the SPX level (comparable in size to SPY) but keeps SPX's cash settlement, European exercise, and Section 1256 tax treatment. In theory it is the best of both worlds for a smaller account that still wants the tax and assignment advantages. The catch is liquidity: XSP volume is far thinner than either SPX or SPY, so spreads are wider and fills are harder. Worth knowing about, worth checking the chain before you commit. How SPX and SPY Options Behave During a Flash Crash Everything above is theory until you watch it play out in a live position. On Friday, June 26, 2026 — during a jittery week in which JPMorgan (read more on that) had publicly warned of flash-crash risk in crowded AI names — the S&P 500 delivered a textbook demonstration of why the SPX-vs-SPY distinction matters. Right at the 4:00 PM close, a wave of sell orders hit thin liquidity. On a standard 1-minute line chart, nothing looked wrong: the line simply connects close-to-close, and the close held around 731 on SPY. But pull up the 1-minute candlestick chart for that final bar and the story changes completely — a tiny body around 731 with an enormous lower wick stabbing all the way down to 716.58, then recovering, all within a single closing minute. The volume bar on that candle dwarfed everything around it. That's the signature of a flash crash: a momentary liquidity air-pocket where a flood of orders blows through a thin book before buyers step back in and the close resolves. This is a closing-bell liquidity cascade — arguably the single most dangerous moment for this kind of event. At 4:00 PM, market-on-close imbalance orders execute, index rebalancing flows hit, and options-expiration settlement pressure peaks all at once. A large sell imbalance in that window can momentarily overwhelm the order book before the closing auction resolves. Here's where it gets instructive. That 716.58 print was SPY's worst individual tick. But the SPX cash index — pulled from live data — only printed down to about 7,336 in the same minute. At the roughly 10:1 ratio, SPY's 716.58 implies an SPX near 7,232, yet the actual index bottomed 100 points higher. Why the gap? During a flash crash, the ETF and the index decouple. SPY is a single instrument, so a market-sell order blows straight through its book and prints an extreme low. The SPX index, by contrast, is an average of all 500 constituents — and not every stock crashes to the same degree in the same instant. The index is "cushioned" by its own construction. The true dislocation sat somewhere between the two readings, with SPY overshooting to the downside. Now apply this to two hypothetical traders, each holding the same S&P 500 put spread going into that close: The SPY trader watched the ETF physically trade at 716.58 — potentially deep inside a danger zone — and, because SPY is American-style and physically settled, faced real assignment mechanics around any in-the-money strikes, plus the gut-punch of seeing the market trade through their level. The SPX trader settled off the official closing print near 7,354–7,357, determined by the closing auction — not the wick. Even the intraday SPX low of ~7,336 stayed above where an equivalent short strike would have sat. The terrifying wick, however real, never touched a cash-settled position that keys off the close. The lesson isn't that SPX is risk-free — that wick proves the market physically traded at a stressed level, and a stop-loss order resting in that zone would have been triggered, auction or not. The lesson is that cash settlement and European exercise changed the outcome. The same market event that could have been painful in SPY or in stock was, on a cash-settled SPX position, a non-event that expired off the official close. That is the structural edge described in the tax and settlement sections above, made concrete in a single closing minute. The decision framework Lean SPX if you: Trade meaningful size (one SPX replaces ten SPY, cutting commissions and complexity) Have enough capital and margin to handle the larger contract comfortably Run an active income strategy where the 60/40 tax treatment materially lowers your bill Want zero early-assignment risk on multi-leg structures Prefer the simplicity of cash settlement and no dividend exposure Lean SPY if you: Trade a smaller account and need granular position sizing Want the tightest absolute spreads and the widest strike selection Are building a strategy around actually holding shares (covered calls, cash-secured puts as accumulation) Are trading inside an IRA, where the Section 1256 tax edge is irrelevant Are newer to S&P 500 options and want to learn on a smaller, more familiar contract Consider XSP if you want SPX's tax and settlement benefits at a SPY-sized contract — and can live with thinner liquidity. The bottom line SPX and SPY track the same market, but they are not interchangeable. For a serious, active options trader — especially one selling premium or trading 0DTE at size — SPX's Section 1256 tax treatment, cash settlement, and freedom from early assignment give it a structural edge that compounds over time, in your fills and in your tax bill. SPY remains the better tool for smaller accounts, share-based strategies, and IRAs. Many experienced traders end up using both: SPX for tax-efficient premium selling at size, SPY for tactical trades and anything involving shares. The right answer isn't universal — it comes down to your account size, your tax situation, and the specific strategy in front of you. Choose the instrument that fits the trade, not the other way around. The examples above exclude commissions and fees and are for educational purposes only. Options trading involves substantial risk and is not suitable for every investor. Review the Characteristics and Risks of Standardized Options before trading. -

That's great to hear — congrats on the BAC fill! And thank you, that really means a lot!

-

Thanks Sarang, really appreciate it! More to come with other analyses. Encouragement like yours on my work helps me move forward!

-

@Romuald first test run was a success as BAC hit 10% target just after open .... that write up is awesome very worthy of a second or even third read ... thanks

-

Why new developments call for a fresh look at pinning Here are, however, specific reasons to revisit pinning as a retail option investor strategy and the first and foremost of this was the announcement on April 16 by the SEC as reported (in this case) by Schwab: "...Under the new rules, traders will no longer be required to maintain a minimum account balance of $25,000 to engage in frequent margin day trading. Instead, eligible margin accounts of more than $2,000 will gain access to intraday margin buying power set by individual brokerages based on current positions and maintenance margin requirements. Currently, under the old rules, four or more day trades in five business days triggers a "pattern day trader" designation and the $25,000 requirement. Under the new framework, the pattern day trader designation will be eliminated, and day trades will no longer be counted...." (or see this video) 1) The biggest limitation to use pinning or expiry strike price effects was the pattern day trader issue. Inevitably strike price effects whilst usable from the Thursday before expiry to the Friday concentrated on the last trading day. Relatively complex positions are required with three or more legs and therefore pattern day trading was unavoidable. This in turn meant that $25,000 had to be in your account and yada yada. Well this is no longer the case and we can trade freely with most brokers; 2) The advent of 0DTE options has contributed massively to an increase in strike price effects. Older research attributed strike price effects to market makers unwinding massive static open positions built up over month at the crunch time of the 3rd Friday expiry. The effects being strongest at the so called ‘triple witching hour’ when stock index futures, stock index options and stock options would expire (3rd Friday of March, June, September and December respectively). With the multiplication of expiries this has decreased dramatically but the advent of shorter options drives market maker gamma hedging. Positive gamma (net long options) forces market makers to buy shares when a stock drops and the reverse if it rises. This creates a mean-reversion mechanism that drives stocks towards strike price levels. 3) A great deal more study was expended looking at the 0DTE options and they have validated something noted in the 2019 article: mid-strike pinning. At the time it was an empirical observation that stocks prone to pinning sometimes gravitated to the exact mid-point between strikes and pinned there instead. This phenomenon is now known as the gamma wall. Competing hedging behaviour finds an exact equilibrium which causes a pin at the mid-level as every hedge needs to be either over or under the current stock price. As the market is a random phenomenon market, makers cannot choose altogether to go for the one or the other. The stock then becomes stuck in a liquidity pocket halfway between strikes. In other words pinning and strike price effects are alive and well and in fact exploitable more than ever. Strike price effects: pinning, crosses, wild trading Steady Options is a unique service in that it proposes strategies that are typically appropriate for the retail investor. Most of us are unable to harness quant strategies or massive positions exploiting minute arbitrage pricing differences. Many people feel that the game is therefore rigged in favour of big money. Sure, if you go head to head with Goldman Sachs you will be crushed. What else would you expect? It’s like going head to head boxing with Mike Tyson in his prime. The retail investor benefits from his ability to trade small, which means better prices than those opening very large positions. Furthermore, there are certain phenomena like rising volatility towards earnings or the effect of additions to the S&P index that cause predictable effects on elements involved in option pricing. A retail investor can count on those and exploit them where a larger investor would find the market as a whole moving if he attempted the same. Pinning is a phenomenon that certain stocks gravitate towards the strike price of an option on the expiry of that option (generally Friday). Pinning is deemed to occur if the stock price remains (and ends) within 15% of strike spacing. This is an adaptation of Jeff Augen’s approach which used static values to determine whether pinning occurs or not. Nominal Stock Price Strike Spacing Old Static Threshold Dynamic Threshold (15% of Spacing) $40.00 $1.00 $0.40 (Too loose) $0.15 $150.00 $2.50 $0.40 (Perfect) $0.37 $350.00 $5.00 $0.40 (Too tight) $0.75 $600.00 $10.00 $0.40 (Impossible) $1.50 This simple visual from my previous article with a live example by AAPL speaks plainly enough as regards to the phenomenon of pinning itself: Figure 1: APPLE 17 March 2017 Expiry The Y-axis is in dollars representing the amount that the stock was trading away from a strike price. The X-axis represents the number of minutes since trading started (a total of 390 minutes). As noted, a stock can also pin in between strikes – a so called mid-way pin. One needs to analyze specific stocks to make a choice but the phenomenon sometimes takes the shape of the above with a sudden plunge or rise towards a strike. At other times a stock will cross a strike price over and over during the final trading day. Another known strike price effect is the sudden inflation of IV (Implied Volatility) towards the day prior to expiry (usually Thursday) around 4 p.m. and the deflation of that IV in the first half hour of trade on the Friday morning. Same as with our earnings or SPY addition trades, no effect is repeated 100% of the time, in fact even in ideal conditions the effect occurs only 50% of the time. Any strategies must therefore be combined with clear risk limitation tactics taking into account we also know that IV will rise exponentially as we near the bell for ATM strikes. Which stocks are suitable? Broad research shows all stocks are affected – oddly even ones without options – however most option strategies that can be used to exploit them require liquidity and narrow spreads. Here is a list of requirements that need to be fulfilled, ideally in all cases but in any case not massively off target: Liquid large cap optionable stocks with small spreads and a stock price over 100$ or more. The general environment must be one of low VIX – if VIX is high you will get ripped because of underlying market effects. Absence of macro catalysts, so no morning CPO, FOMC, significant earnings by market moving stocks and above all shield us from Trump tweets. Check open interest on the day – it should be heavily stacked on a single psychological strike generally a round number or at least a multiple of 5. This should be quite asymmetric to the remainder of stock open interest at other strikes. The expiry day strike price effects occur over a slightly broader range than my original article averred. You can start looking for effects around 11 a.m. right up to even 1 p.m.. Closing always before the end of day and a minimum of 15 minutes as closing minutes get crazy. If we speak of volatility effects of the end of day before expiry the opening should be around 4 p.m. and closing maximum 30 minutes after the opening. With the proliferation of expiry dates, Friday is not necessarily the only day but liquidity remains the biggest issue. AAPL remains a pinning stalwart and before its company split FDX was the loose electron that would gravitate over and under a strike. GS, MA, NVDA and similar stocks are all worth examining for potential strike price effect opportunities. What option strategies are suitable? In options trading nothing beats being right on direction whatever that direction is, so this includes the stock being stationary. How to exploit that knowledge really has no limit due to the flexibility of options as a trading instrument. Here are just some scenarios with stocks that you believe will pin. The ideas can be tweaked based on the situation. Exploiting the day before expiry This builds on the brief collapse in volatility after 4 p.m. on Thursday, its reinflation on Friday morning and the fall again after 10 p.m. that day. A simple way is the ratio trade for example if the stock is between strikes S and S+1 (the +1 in this case being the next optionable strike not 1$ necessarily). The position is to be opened on Thursday around 4 p.m. if the other criteria for strike price effects (see above) have been met. Buy 10 calls of next day expiry at S Sell 30 calls of next day expiry at S+1 The position should be closed at 10a.m. on Friday and will generate substantial profits even if the stock rises to the S+1 strike price. This is due to volatility decreasing and theta decay. A heavy drop in the stock will be buffered and losses should be manageable. Likewise an unexpected strong rise of the stock is temporarily buffered by the volatility loss and the long underlying position. The position is not proof to all circumstances but simply sufficiently flexible to bail if it goes sideways. If the stock is really pinning at S+1 you should hold till the end as that will maximize profits. On the hand a massive, runaway gap up past represents a maximum risk zone, which is why a disciplined hard exit at Friday's 10 a.m. open is non-negotiable. The classic pin This strategy presumes that you see pin occurring at a particular strike S. As stated, that should become apparent between 11 a.m. to 1p.m. on the expiry day. The lull in trading caused by lunch is helpful to get good prices. Buy 10 calls at S-1 Sell 30 calls at S Buy 20 calls at S+1 or Buy 20 calls S=2 to limit margin and have an open balanced wing butterfly. This position should be closed at the latest 10-15 minutes before the bell when ideally the value of the ATM calls has been bled dry by theta. It relies fully on a real pin at a strike occurring and will lose money in free trading or mid-pin outcomes. A less trade intensive variant is to sell a call or put at S (the pinning strike) and buy the same one week out. You then wait for the short option to bleed its premium whilst the smaller amount of theta bleeding from your long still protects you in case things go sideways. The mid-way pin If you foresee the stock sticking between two strikes one can open an Iron Condor ‘Plateau’ spread (again between 11 a.m. to 1 p.m. on the expiry day). Buy 1 Put at (OR S-1) Sell 1 Put at -1 (OR S) Sell 1 Call at (OR S) Buy 1 Call at (Or S+1) Like all these strategies, you can’t afford to walk away whilst this is playing out but the set-up works in case of a mid-strike pin and if held to (near) the end even if S-1 or S+1 are reached. The biggest issue used to be that not many stocks provide sufficient premium to make it worth one’s while to open this but it is possible with some high volatility high priced stocks. With the current run of high value tech stocks, however, the story is different and IC premiums can be attractive. Utilizing crosses-gamma scalping As mentioned some stocks are known– FDX was notorious for this at least until their stock divestment – for not pinning in a fixed manner but continually crossing a pinning strike either to the upside or the downside. The idea in this case is to utilize the lull in trade as of 11am to 1pm to open a straddle at S if the stock happens to be there. If the stock moves up or down, one or the other side of the spread will make a gain. Occasionally this in itself will be enough to take a profit but usually it is not. The trick is then to delta hedge by either going long or shorting shares to neutralize your delta. Option software to know how many shares to sell is helpful here but one can eyeball it to a degree. Once the stock moves back to S one can close the stock position (or the whole position) and make small gains. Beware of attempting to sell short straddles when the stock is away from S, pinning happens tops 50% of the time so you can find yourself with a huge loss if the stock goes to S+1 or S-2 whilst the profits from all the above strategies are modest. Finding candidates As mentioned above, we need high liquidity stocks with massive option volumes and a clear indicator in the open interest that a pinning situation or crossing is on the books. With the advent of AI, things have become considerably simpler compared to 2019 when the previous article was published. At the time there was nothing for it but to laboriously download data and run analyses through excel on it (at least as a retail investor). With the help of AI we have created a number of little python scripts which can help you. They can be run from python directly if you have that installed but you can also run it in Google Colab. When you run this simple script (see file below entitled simple script), you will be asked to input a ticker, a date for which you want to run the analysis – limited in this case to the previous 4 weeks as the source is Yahoo which is free for that period – and then an entry time. You will get – for example for MSFT – an output like this: So in this example MSFT did a min pin level for most of the trading and a strategy utilizing that and closed in time would have yielded a good result. Historical outcomes do not guarantee a repeated pattern but the idea is to visualize for you how you can identify what the potential pinning level might be and see where trades might have been successful. This can then help you to open positions. The second script (see file below called complex script) is a little more involved, it requires you to have a polygon.io account (free) so that the minute by minute stock data can be downloaded. If you register, your dashboard will give you an API Key that you need to paste in to run it. The script requires 10 minutes+ to run because there is a limit on the amount of data you may download. It gives the following output for, again, MSFT in this case: Note that the values for the option spreads are based on Black & Scholes and not downloaded data. They are not going to be identical to what’s in the market but not a million miles away either. In this case we asked the script to determine the best entry price rather than asking it to pick one as that wouldn’t make sense during a whole year. The outcome is that actually the midday lull – after major morning institutional activity is over – remains the best time to take the jump to open a position. Waiting until at least 12 noon reduces the number of Free Trading outcomes – that is where no perceptible pinning occurred – to 25% or less. What is also clear is that when VIX is higher – i.e. over 16 – more free trading failures occur, whereas below this the number of successful trades is almost double. The cross count column is a powerful indicator of market maker positioning. The distributions across your 39 weeks reveal a stark reality: Intraday Gravity Days: Feature a massive average of 20.2 strike crosses. Classic Pin Days: Feature a clean average of 7.3 strike crosses. Mid-Pin Trap Days: Feature a low average of just 4.4 strike crosses. If you enter a trade during the midday lull and the stock begins to continuously slice back and forth across your target strike, market-maker gamma walls are actively trapping the asset. The heavy volume is forcing a tight mean-reversion around that strike pivot. However, if you establish a position and the stock drifts away without crossing your strike at least twice within the first 30 minutes, the gravity is absent. Given the low cross average on trap days, the asset is likely locked into a clean, low-friction trajectory straight toward a mid-pin hit. For MSFT – based on the last year – a good guide seems to be to open after 12 noon, to avoid ratio strategies if VIX is under 16 but to use an Iron Condor instead. Note that this requires a stock that has a high price – around $300+ although a high beta-stock will also work. Finally, if within 30minutes of opening the trade there are few crosses you should consider that the position might migrate to a mid pin. Change your position in function of that. Finding what works Without boring everyone with the various back-tests that were carried out, analysing stocks with rather different characteristics in the manner described above yielded an interesting playbook of strategies to play. Check the VIX. If it is printing above 20.0, walk away. Institutional fear is too high for pinning to work. If trading a High-Priced Mega-Cap (e.g., MSFT): Check the morning session's realized volatility proxy. If it passes your 17% VIX floor, deploy an OTM Iron Condor (Short Put / Short Call). It provides an airtight, 100% historical safety net. If trading a Mid-Priced, Low-Beta Tech Asset (e.g., AAPL): Completely avoid the OTM layout—the market won't pay you enough to justify the margin. Instead, deploy the ATM Iron Fly to harvest a premium cushion that neutralizes the mid-pin traps. If trading a High-Beta Volatility Outlier (e.g., FDX): Again deploy the OTM Iron Condor. The asset's native whipping action guarantees a good premium payout to sit safely behind a wide strike wide protective boundary. Remember also that the cross-count is a key indicator whether things are going as you expected or not. This is not a fire and forget kind of strategy but one where you sit behind your computer and watch the skies err... the market. Conclusions Pinning is alive and well and there are opportunities for retail traders for the very good reason that institutionals cannot profitably trade such tiny volumes easily. Whether it is a good strategy does depend on the environment and low VIX at the minimum is required or it becomes too risky. Oddly, another factor that is important is the high prices of current high liquidity stocks – this facilitates the use of Iron Condors or Iron Flies which can show excellent outcomes based on holding a position for just a few hours or less. As usual, you do have your eggs in one basket so you’d better watch that basket. In 2019 we estimated a 6% per month return was possible taking into account inevitable losses. With the refinement and encompassing of mid-pin outcomes which enables us to be >60% in having a pin, mid-pin or mid-day gravity outcome, we should have better results than before.

Why new developments call for a fresh look at pinning Here are, however, specific reasons to revisit pinning as a retail option investor strategy and the first and foremost of this was the announcement on April 16 by the SEC as reported (in this case) by Schwab: "...Under the new rules, traders will no longer be required to maintain a minimum account balance of $25,000 to engage in frequent margin day trading. Instead, eligible margin accounts of more than $2,000 will gain access to intraday margin buying power set by individual brokerages based on current positions and maintenance margin requirements. Currently, under the old rules, four or more day trades in five business days triggers a "pattern day trader" designation and the $25,000 requirement. Under the new framework, the pattern day trader designation will be eliminated, and day trades will no longer be counted...." (or see this video) 1) The biggest limitation to use pinning or expiry strike price effects was the pattern day trader issue. Inevitably strike price effects whilst usable from the Thursday before expiry to the Friday concentrated on the last trading day. Relatively complex positions are required with three or more legs and therefore pattern day trading was unavoidable. This in turn meant that $25,000 had to be in your account and yada yada. Well this is no longer the case and we can trade freely with most brokers; 2) The advent of 0DTE options has contributed massively to an increase in strike price effects. Older research attributed strike price effects to market makers unwinding massive static open positions built up over month at the crunch time of the 3rd Friday expiry. The effects being strongest at the so called ‘triple witching hour’ when stock index futures, stock index options and stock options would expire (3rd Friday of March, June, September and December respectively). With the multiplication of expiries this has decreased dramatically but the advent of shorter options drives market maker gamma hedging. Positive gamma (net long options) forces market makers to buy shares when a stock drops and the reverse if it rises. This creates a mean-reversion mechanism that drives stocks towards strike price levels. 3) A great deal more study was expended looking at the 0DTE options and they have validated something noted in the 2019 article: mid-strike pinning. At the time it was an empirical observation that stocks prone to pinning sometimes gravitated to the exact mid-point between strikes and pinned there instead. This phenomenon is now known as the gamma wall. Competing hedging behaviour finds an exact equilibrium which causes a pin at the mid-level as every hedge needs to be either over or under the current stock price. As the market is a random phenomenon market, makers cannot choose altogether to go for the one or the other. The stock then becomes stuck in a liquidity pocket halfway between strikes. In other words pinning and strike price effects are alive and well and in fact exploitable more than ever. Strike price effects: pinning, crosses, wild trading Steady Options is a unique service in that it proposes strategies that are typically appropriate for the retail investor. Most of us are unable to harness quant strategies or massive positions exploiting minute arbitrage pricing differences. Many people feel that the game is therefore rigged in favour of big money. Sure, if you go head to head with Goldman Sachs you will be crushed. What else would you expect? It’s like going head to head boxing with Mike Tyson in his prime. The retail investor benefits from his ability to trade small, which means better prices than those opening very large positions. Furthermore, there are certain phenomena like rising volatility towards earnings or the effect of additions to the S&P index that cause predictable effects on elements involved in option pricing. A retail investor can count on those and exploit them where a larger investor would find the market as a whole moving if he attempted the same. Pinning is a phenomenon that certain stocks gravitate towards the strike price of an option on the expiry of that option (generally Friday). Pinning is deemed to occur if the stock price remains (and ends) within 15% of strike spacing. This is an adaptation of Jeff Augen’s approach which used static values to determine whether pinning occurs or not. Nominal Stock Price Strike Spacing Old Static Threshold Dynamic Threshold (15% of Spacing) $40.00 $1.00 $0.40 (Too loose) $0.15 $150.00 $2.50 $0.40 (Perfect) $0.37 $350.00 $5.00 $0.40 (Too tight) $0.75 $600.00 $10.00 $0.40 (Impossible) $1.50 This simple visual from my previous article with a live example by AAPL speaks plainly enough as regards to the phenomenon of pinning itself: Figure 1: APPLE 17 March 2017 Expiry The Y-axis is in dollars representing the amount that the stock was trading away from a strike price. The X-axis represents the number of minutes since trading started (a total of 390 minutes). As noted, a stock can also pin in between strikes – a so called mid-way pin. One needs to analyze specific stocks to make a choice but the phenomenon sometimes takes the shape of the above with a sudden plunge or rise towards a strike. At other times a stock will cross a strike price over and over during the final trading day. Another known strike price effect is the sudden inflation of IV (Implied Volatility) towards the day prior to expiry (usually Thursday) around 4 p.m. and the deflation of that IV in the first half hour of trade on the Friday morning. Same as with our earnings or SPY addition trades, no effect is repeated 100% of the time, in fact even in ideal conditions the effect occurs only 50% of the time. Any strategies must therefore be combined with clear risk limitation tactics taking into account we also know that IV will rise exponentially as we near the bell for ATM strikes. Which stocks are suitable? Broad research shows all stocks are affected – oddly even ones without options – however most option strategies that can be used to exploit them require liquidity and narrow spreads. Here is a list of requirements that need to be fulfilled, ideally in all cases but in any case not massively off target: Liquid large cap optionable stocks with small spreads and a stock price over 100$ or more. The general environment must be one of low VIX – if VIX is high you will get ripped because of underlying market effects. Absence of macro catalysts, so no morning CPO, FOMC, significant earnings by market moving stocks and above all shield us from Trump tweets. Check open interest on the day – it should be heavily stacked on a single psychological strike generally a round number or at least a multiple of 5. This should be quite asymmetric to the remainder of stock open interest at other strikes. The expiry day strike price effects occur over a slightly broader range than my original article averred. You can start looking for effects around 11 a.m. right up to even 1 p.m.. Closing always before the end of day and a minimum of 15 minutes as closing minutes get crazy. If we speak of volatility effects of the end of day before expiry the opening should be around 4 p.m. and closing maximum 30 minutes after the opening. With the proliferation of expiry dates, Friday is not necessarily the only day but liquidity remains the biggest issue. AAPL remains a pinning stalwart and before its company split FDX was the loose electron that would gravitate over and under a strike. GS, MA, NVDA and similar stocks are all worth examining for potential strike price effect opportunities. What option strategies are suitable? In options trading nothing beats being right on direction whatever that direction is, so this includes the stock being stationary. How to exploit that knowledge really has no limit due to the flexibility of options as a trading instrument. Here are just some scenarios with stocks that you believe will pin. The ideas can be tweaked based on the situation. Exploiting the day before expiry This builds on the brief collapse in volatility after 4 p.m. on Thursday, its reinflation on Friday morning and the fall again after 10 p.m. that day. A simple way is the ratio trade for example if the stock is between strikes S and S+1 (the +1 in this case being the next optionable strike not 1$ necessarily). The position is to be opened on Thursday around 4 p.m. if the other criteria for strike price effects (see above) have been met. Buy 10 calls of next day expiry at S Sell 30 calls of next day expiry at S+1 The position should be closed at 10a.m. on Friday and will generate substantial profits even if the stock rises to the S+1 strike price. This is due to volatility decreasing and theta decay. A heavy drop in the stock will be buffered and losses should be manageable. Likewise an unexpected strong rise of the stock is temporarily buffered by the volatility loss and the long underlying position. The position is not proof to all circumstances but simply sufficiently flexible to bail if it goes sideways. If the stock is really pinning at S+1 you should hold till the end as that will maximize profits. On the hand a massive, runaway gap up past represents a maximum risk zone, which is why a disciplined hard exit at Friday's 10 a.m. open is non-negotiable. The classic pin This strategy presumes that you see pin occurring at a particular strike S. As stated, that should become apparent between 11 a.m. to 1p.m. on the expiry day. The lull in trading caused by lunch is helpful to get good prices. Buy 10 calls at S-1 Sell 30 calls at S Buy 20 calls at S+1 or Buy 20 calls S=2 to limit margin and have an open balanced wing butterfly. This position should be closed at the latest 10-15 minutes before the bell when ideally the value of the ATM calls has been bled dry by theta. It relies fully on a real pin at a strike occurring and will lose money in free trading or mid-pin outcomes. A less trade intensive variant is to sell a call or put at S (the pinning strike) and buy the same one week out. You then wait for the short option to bleed its premium whilst the smaller amount of theta bleeding from your long still protects you in case things go sideways. The mid-way pin If you foresee the stock sticking between two strikes one can open an Iron Condor ‘Plateau’ spread (again between 11 a.m. to 1 p.m. on the expiry day). Buy 1 Put at (OR S-1) Sell 1 Put at -1 (OR S) Sell 1 Call at (OR S) Buy 1 Call at (Or S+1) Like all these strategies, you can’t afford to walk away whilst this is playing out but the set-up works in case of a mid-strike pin and if held to (near) the end even if S-1 or S+1 are reached. The biggest issue used to be that not many stocks provide sufficient premium to make it worth one’s while to open this but it is possible with some high volatility high priced stocks. With the current run of high value tech stocks, however, the story is different and IC premiums can be attractive. Utilizing crosses-gamma scalping As mentioned some stocks are known– FDX was notorious for this at least until their stock divestment – for not pinning in a fixed manner but continually crossing a pinning strike either to the upside or the downside. The idea in this case is to utilize the lull in trade as of 11am to 1pm to open a straddle at S if the stock happens to be there. If the stock moves up or down, one or the other side of the spread will make a gain. Occasionally this in itself will be enough to take a profit but usually it is not. The trick is then to delta hedge by either going long or shorting shares to neutralize your delta. Option software to know how many shares to sell is helpful here but one can eyeball it to a degree. Once the stock moves back to S one can close the stock position (or the whole position) and make small gains. Beware of attempting to sell short straddles when the stock is away from S, pinning happens tops 50% of the time so you can find yourself with a huge loss if the stock goes to S+1 or S-2 whilst the profits from all the above strategies are modest. Finding candidates As mentioned above, we need high liquidity stocks with massive option volumes and a clear indicator in the open interest that a pinning situation or crossing is on the books. With the advent of AI, things have become considerably simpler compared to 2019 when the previous article was published. At the time there was nothing for it but to laboriously download data and run analyses through excel on it (at least as a retail investor). With the help of AI we have created a number of little python scripts which can help you. They can be run from python directly if you have that installed but you can also run it in Google Colab. When you run this simple script (see file below entitled simple script), you will be asked to input a ticker, a date for which you want to run the analysis – limited in this case to the previous 4 weeks as the source is Yahoo which is free for that period – and then an entry time. You will get – for example for MSFT – an output like this: So in this example MSFT did a min pin level for most of the trading and a strategy utilizing that and closed in time would have yielded a good result. Historical outcomes do not guarantee a repeated pattern but the idea is to visualize for you how you can identify what the potential pinning level might be and see where trades might have been successful. This can then help you to open positions. The second script (see file below called complex script) is a little more involved, it requires you to have a polygon.io account (free) so that the minute by minute stock data can be downloaded. If you register, your dashboard will give you an API Key that you need to paste in to run it. The script requires 10 minutes+ to run because there is a limit on the amount of data you may download. It gives the following output for, again, MSFT in this case: Note that the values for the option spreads are based on Black & Scholes and not downloaded data. They are not going to be identical to what’s in the market but not a million miles away either. In this case we asked the script to determine the best entry price rather than asking it to pick one as that wouldn’t make sense during a whole year. The outcome is that actually the midday lull – after major morning institutional activity is over – remains the best time to take the jump to open a position. Waiting until at least 12 noon reduces the number of Free Trading outcomes – that is where no perceptible pinning occurred – to 25% or less. What is also clear is that when VIX is higher – i.e. over 16 – more free trading failures occur, whereas below this the number of successful trades is almost double. The cross count column is a powerful indicator of market maker positioning. The distributions across your 39 weeks reveal a stark reality: Intraday Gravity Days: Feature a massive average of 20.2 strike crosses. Classic Pin Days: Feature a clean average of 7.3 strike crosses. Mid-Pin Trap Days: Feature a low average of just 4.4 strike crosses. If you enter a trade during the midday lull and the stock begins to continuously slice back and forth across your target strike, market-maker gamma walls are actively trapping the asset. The heavy volume is forcing a tight mean-reversion around that strike pivot. However, if you establish a position and the stock drifts away without crossing your strike at least twice within the first 30 minutes, the gravity is absent. Given the low cross average on trap days, the asset is likely locked into a clean, low-friction trajectory straight toward a mid-pin hit. For MSFT – based on the last year – a good guide seems to be to open after 12 noon, to avoid ratio strategies if VIX is under 16 but to use an Iron Condor instead. Note that this requires a stock that has a high price – around $300+ although a high beta-stock will also work. Finally, if within 30minutes of opening the trade there are few crosses you should consider that the position might migrate to a mid pin. Change your position in function of that. Finding what works Without boring everyone with the various back-tests that were carried out, analysing stocks with rather different characteristics in the manner described above yielded an interesting playbook of strategies to play. Check the VIX. If it is printing above 20.0, walk away. Institutional fear is too high for pinning to work. If trading a High-Priced Mega-Cap (e.g., MSFT): Check the morning session's realized volatility proxy. If it passes your 17% VIX floor, deploy an OTM Iron Condor (Short Put / Short Call). It provides an airtight, 100% historical safety net. If trading a Mid-Priced, Low-Beta Tech Asset (e.g., AAPL): Completely avoid the OTM layout—the market won't pay you enough to justify the margin. Instead, deploy the ATM Iron Fly to harvest a premium cushion that neutralizes the mid-pin traps. If trading a High-Beta Volatility Outlier (e.g., FDX): Again deploy the OTM Iron Condor. The asset's native whipping action guarantees a good premium payout to sit safely behind a wide strike wide protective boundary. Remember also that the cross-count is a key indicator whether things are going as you expected or not. This is not a fire and forget kind of strategy but one where you sit behind your computer and watch the skies err... the market. Conclusions Pinning is alive and well and there are opportunities for retail traders for the very good reason that institutionals cannot profitably trade such tiny volumes easily. Whether it is a good strategy does depend on the environment and low VIX at the minimum is required or it becomes too risky. Oddly, another factor that is important is the high prices of current high liquidity stocks – this facilitates the use of Iron Condors or Iron Flies which can show excellent outcomes based on holding a position for just a few hours or less. As usual, you do have your eggs in one basket so you’d better watch that basket. In 2019 we estimated a 6% per month return was possible taking into account inevitable losses. With the refinement and encompassing of mid-pin outcomes which enables us to be >60% in having a pin, mid-pin or mid-day gravity outcome, we should have better results than before. -

Good morning Romauld, Great Analysis and discussion! Thank you. Sarang

Good morning Romauld, Great Analysis and discussion! Thank you. Sarang -