In this article, we will take a look at four of my go to options strategies when I have a directional bias in the market.

Generally, I want to be a seller of options, but there will be times when it makes sense to buy options. There are four primary trading strategies that I like to employ in the options market when I have a conviction about the directional price move for a stock. These include Deep in the Money (DITM) Calls or Puts, Debit Spreads, Credit Spreads, and the Diagonal Spread.

Deep In the Money Calls and Puts (DITM)

As you may be aware, many less experienced Options Traders tend to use a straight long call or long put strategy when they want to play a long or short position on a stock or index. Typically, they will buy out of the money options, as they tend to be the cheapest. This type of strategy however offers the lowest edge in the options market, and the vast majority of these option contracts expire worthless.

Instead of the far out of the money options, I prefer to buy Deep In the Money Options with a Delta between 90-95. These contracts will typically offer lower capital requirements than a margined stock trading account, and more importantly, they tend to move almost lockstep with their underlying. This is due to the high Delta component associated with buying DITM options. DITM options typically have very little extrinsic value which can weigh on an option’s price.

Have you ever wondered why your options contract hasn't moved even when the underlying stock has moved in your intended direction? It’s likely because the extrinsic value makes up a large percentage of the value of the contract. Well, with DITM options this is not a concern. As such, it is a great vehicle for taking advantage of a directional position without giving up too much of an edge. DITM options do tend to be priced much richer than ATM or Slightly ITM options, but the advantages they offer over straight long calls and puts is undeniable.

Debit Spreads

Debits spreads are classified into two different categories. Bull Debit Spread and Bear Debit Spread. You would use a Bull Debit Spread when you have a bullish bias in a stock, and you would use a Bear Debit Spread when you have a bearish assumption about a stock.

With a Debit Spread you will pay a “Debit” to get into the trade. In addition, this is a limited risk strategy, so you can only lose the amount that you initially put us as the Debit. The strategy also has a limited profit potential. I like to use Debit Spreads when the stock is within its lower range of Implied Volatility and when I have moderate directional outlook on a trade. It is less aggressive than a straight buy call or buy put strategy. Essentially, I expect prices to move in a certain direction within the expiration time window but I am not expecting a huge move.

A Bullish Debit Spread consists of the following:

- Buy 1 Call

- Sell 1 Call further away above the long Call

With a Bull Debit Spread you are less prone to time decay and sudden volatility changes, because the structure has one Long Call and one Short call.

A Bearish Put Spread consists of the following:

- Buy 1 Put

- Sell 1 Put further away below the long Put

Similar to a Bullish Debit Spread, a Bearish Debit Spread is less prone to time decay and sudden volatility shifts, because the structure has one Long Put and one Short Put.

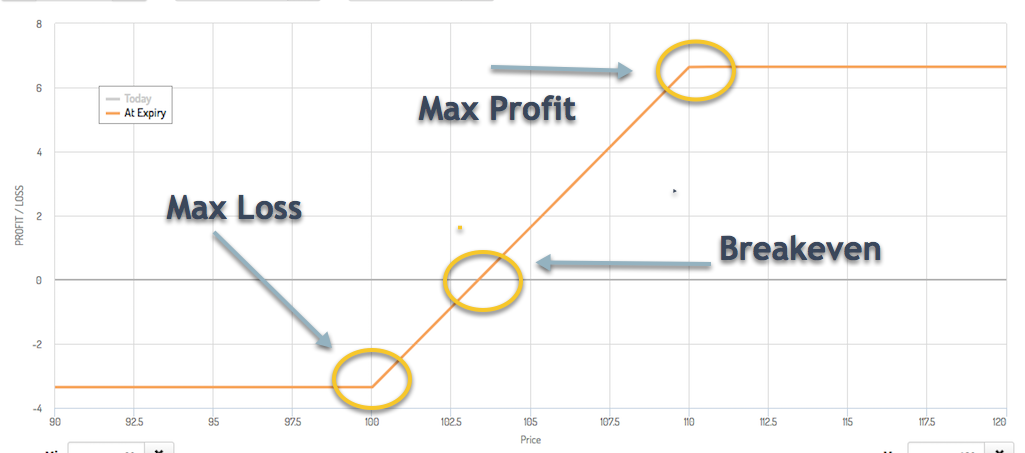

Below you will find the Profit Loss Diagram for a Bull Credit Spread ( Buy Call at 100, Sell Call at 110)

As you can see from the Profit and Loss diagram above, the Max loss is equal to the “Debit” paid. The max profit is the width of the strikes minus the Debit paid. The break-even point for a bull debit spread is equal to the premium paid added to the strike price of the long call.

Credit Spreads

Now we’ll discuss one of my favorite options trading strategies when I have a directional bias. The option strategy I am referring to is Credit Spreads. Credits Spreads are great because it allows me to be an Option seller and collect premium on the trade, while also taking advantage of the potential price move based my analysis. So, I can benefit from the time decay as well as the intended price movement.

Usually I will try to structure these trades on stocks where implied volatility for the stock is also within its upper range. Since volatility tends to be mean reverting, a high implied volatility of a stock will more than likely fall back to its mean. And since we are selling at higher volatility levels with Credit Spreads, the option would be priced richer than when it is at lower volatility levels. So, with Credit Spreads, I can have a trifecta of factors working in my favor - Time Decay, Direction, and Volatility.

There are two types of Credit Spreads - Bullish and Bearish. So, let’slook at the structure of each.

Bullish Credit Spread

- Sell 1 ITM Put

- Buy 1 OTM Put

Bearish Credit Spread

- Sell 1 ITM Call

- Buy 1 OTM Call

Credit spreads offer both limited upside potential and limited downside risk. The Breakeven Point on the trade is Strike Price of the Short Put or Short Call - Net premium collected.

Diagonal Spread

Diagonal spreads are a more advanced directional strategy. For those starting out, I would recommend mastering Debit and Credit Spreads before moving into Diagonals. The Long Diagonal is actually a variation of the Debit Spread but with a twist. This strategy works well when the implied volatility range for the stock is in the lower end of the 52-week range. In addition, it is a strategy I use when I expect a price move to occur within the next 30-60 days.

Basically, a long diagonal spread is an option strategy wherein you sell an option at a nearby month, preferably, with at least 30 days to expiration, and buy an option at a further expiration date, typically the next monthly expiration cycle. By doing so, you can reduce the negative effect of time decay because you are selling an option in the front month to help offset the purchase of the further out option contract.

We want the short option to expire worthless so that we can earn credit on that leg of the trade. In addition, since we are buying a diagonal when the volatility is relatively low, we can also benefit from an increase in volatility back to the mean along with price movement in our desired direction.

Below you will find the Payoff Diagram for a Long Diagonal with a 100 strike price (Short Call 30 DTE and Long Call 60 DTE)

Summary

In this article, we have learned about four directional option trading strategies that you can employ outside of the pure buy call or buy put strategy. Each offers a different risk and reward profile, and should be utilized at different times based on market conditions. I encourage you to do your own testing to see if they are a good fit for your portfolio.

At first, this may seem a bit overwhelming but with the proper practice and patience, you should be able to master at least one of two of these directional plays. They are a great addition to your non-directional strategies that you may have in your playbook such as Iron Condors and Iron Butterflies.

If there is one thing we know about the market, it’s that it is constantly evolving and changing. There will be periods of low volatility and high volatility. There will be periods where the markets are consolidating, and other periods where the market presents trending opportunities. The most important thing is to keep an eye out and have enough tools in your options trading toolkit so that you are able to adjust to these changing market conditions.

This article was written by Vic Patel. He has over 20 years’ experience in the Equities and Forex market. He is the head trader and founder of Forex Training Group.

There are no comments to display.

Join the conversation

You can post now and register later. If you have an account, sign in now to post with your account.

Note: Your post will require moderator approval before it will be visible.