How Simple is a Simple Options Trade?

Like all options setups, short puts do involve risk (see risk plot below); however, I won’t spend time covering the details on how this setup works. Instead I’ll assume you have a general knowledge of how to enter and exit a short put position.

What I would like to discuss is how we enter such trades, namely, what are the tradeoffs we make in trade selection by analyzing a moderately volatile stock. Trade selection involves choosing the optimal strike price and expiration cycle relative to your trading objective. In this article, I’ll focus on strike selection with a future article looking at the various choices for expiration date.

It is interesting to compare the tradeoffs of strike selection from the standpoint of the put being in-the-money (ITM), at-the-money (ATM), out-the-money (OTM), and further OTM. This gives us a comprehensive spectrum to make comparisons, but recognize that the tradeoffs span across the entire option chain. We consciously or subconsciously evaluate tradeoffs at every strike, not only when crossing the distinct boundaries above.

The challenge to consistently evaluate and make decisions in a nearly infinite spectrum of trades with a similar objectives was the core problem we looked to solve when developing our options ranker software. Let me share with you at a high-level how this challenge is structured.

For this discussion, we will use 3M Corporation stock (MMM), a moderately volatile issue (market beta of 1.15) trading at a 52-week high-low range (as of March 1, 2019 close) of $241.35-$178.62 and a current price a closing market price of $207.39 per share.

The Dilemma of Tradeoffs in Strike Selection

MMM trading at $207 in the market presents different strike selection choices when writing a put. What drives your selection of a strike price, however, creates an interesting dilemma.

For example, if you choose an ITM setup, what is the actual goal, what are the risks relative to the moderate volatility of MMM and what do you give up in comparison to a strike selection that is ATM or OTM?

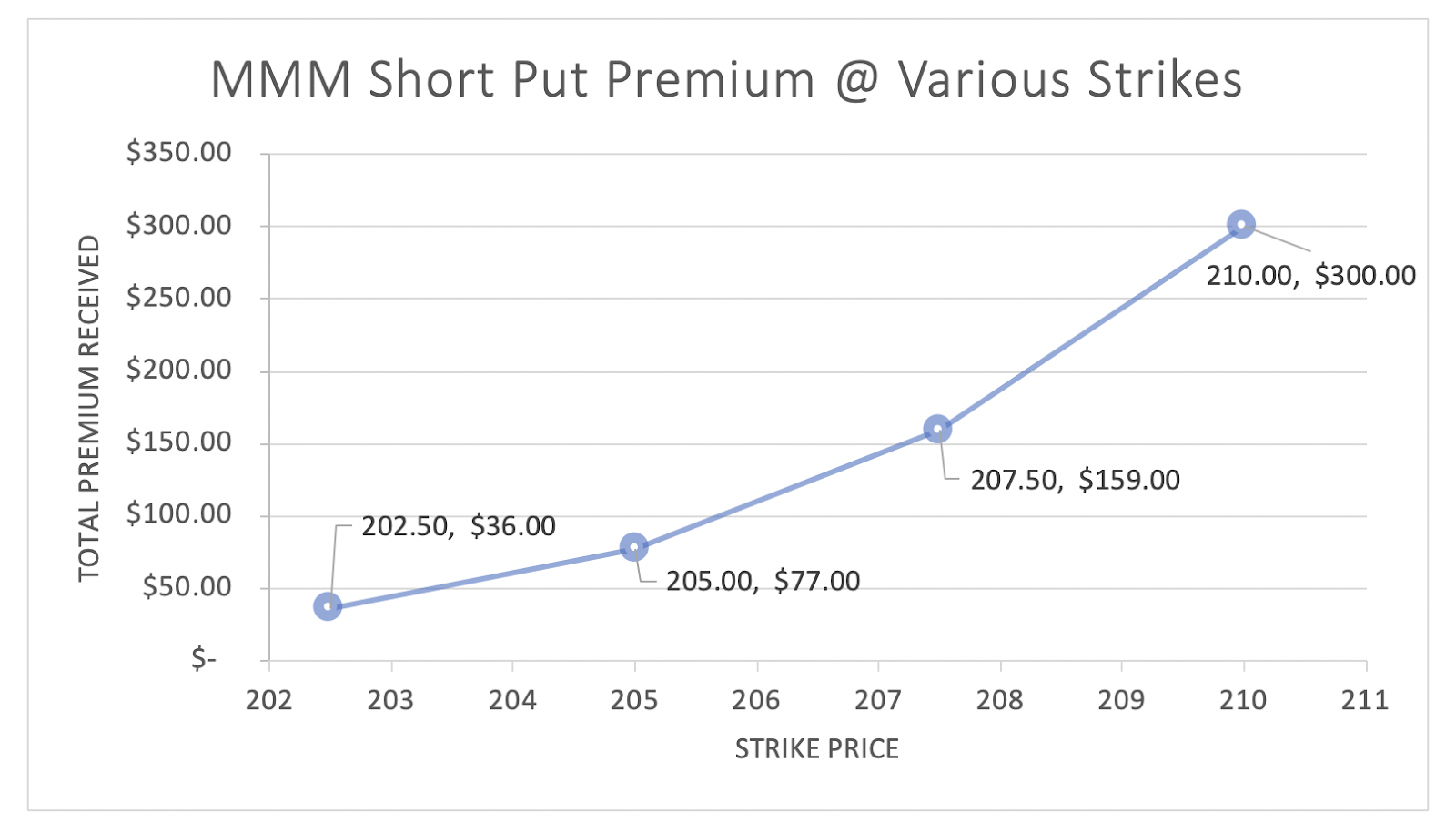

A look at the near-term puts for MMM (March 8 based on the March 1st close for the strike intervals between 202.50 (deep OTM) and 210.00 (ITM), here’s what you would have seen:

MMM Mkt$ = $207.39 (March 1, 2019)

|

Strike Price |

Premium (Bid) |

Extrinsic Value |

Position |

|

202.50 |

0.36 |

0.36 |

Deep OTM |

|

205.00 |

0.77 |

0.77 |

OTM |

|

207.50 |

1.59 |

1.48 |

ATM |

|

210.00 |

3.00 |

0.39 |

ITM |

Moving from deep OTM (202.50) to ITM (210.00) at entry, the premium received increases with each strike. This is a consequence of a bullish outlook. The higher premium for the ITM strike is a product of its extrinsic and intrinsic values.

The Curious Behavior When Shorts Puts are ITM

With MMM trading a little over $207, we could choose a strike price of $210 to put on a trade slightly ITM. We might do this if we were particularly bullish, in order to capture as much premium as possible.

However, when the short put is ITM at entry this places the you at risk of exercise and erodes the premium received from extrinsic value. This raises two interesting questions as to the relative risk of establishing a short that is approximately 2-½ points ITM vs. at or out-of-the money: First, is the higher payout worth receiving an exercise notice prior to expiration – potentially forcing you to purchase the shares? Second, is the trader’s bullishness better expressed in a complementing position or instrument considering the extrinsic value is so severely eroded?

Being ITM creates some urgency for the put writer, because the longer the position remains open, the more likely exercise by the holder will take place as the remaining extrinsic value will continue to erode. This can be exacerbated if the stock will soon go ex-dividend. In a sense, the play begins to take on characteristics of a long call vs. a short put.

This sense of urgency may be tempered somewhat with a stock of moderate volatility since breakeven (intrinsic + extrinsic) may not be breached.

Comparing Greeks Across Strike Selection

Let’s now look at the Greeks (Delta, Gamma, Theta) at trade entry for short puts on MMM that are ITM, ATM, OTM, and deep OTM to see how they compare. While the Greeks are not the only tradeoffs to consider across the strikes, it does give us a good picture on how the positions behave and differ from one another.

Before we make our high-level comparisons, let’s first define the “ideal” values for each of the Greek parameters.

“Ideal Parameters” when Shorting Puts

-

Delta (measures the price change of an option relative to a change in the price of the underlying stock) – usually as premium sellers we’re looking to minimize our delta exposure. This allows us to have less volatility in our position with small moves in the underlying. The exception to this rule is when we’re using short positions ITM or deep ITM as we’re using the position for a directional play.

-

Gamma (measures the options delta exposure to movement in the price of the underlying stock) – Similar to delta, we want the changes to delta to be minimal with small moves in the underlying. Gamma is usually described as a risk (gamma risk) for premium sellers. It is the buyer/holders friend as it provides the leverage.

-

Theta (measures the change in the option’s price relative to time) – This is our primary profitability criterion as premium sellers. We want to see as much theta decay as possible with minimal movement in the stock. Gamma and Theta are strongest pitted against each other.

Value of Greeks – Short Put ITM

Let’s now look at the Greeks (Delta, Gamma, Theta) for an ITM short put which pay $300 in premium. The values at entry are as follows:

-

Delta– the delta of an ITM short put on MMM shows –0.74 which means that as the price continues to move below the strike price by $1 the put will become $0.74 more expensive to buy back. In other words, the ITM position is closely mimicking the underlying stock and will increase to a delta of -1.0 with the effect of gamma.

-

Gamma– the gamma for the short put that is ITM should move slower than the fall in the underlying stock – somewhere about 0.09. This means a $1 drop in the price of MMM would result in a 0.09 increase in the negative delta, bringing it even closer to parity with the underlying stock.

-

Theta– theta for the ITM short put is 0.065 $/day. Therefore, with no price movement you can expect the position to make $6.50 per day. Theta only erodes the extrinsic value in the option, so we will see the greatest theta ATM and reduced theta with the ITM option here as a lot of the premium is associated with intrinsic value. Due to this, the underlying stock must increase in value above the strike of the option (210) for the option to expire with no value.

Value of Greeks – Short Put ATM

At-the-money lessens exercise risk for the writer and provides the highest amount of extrinsic value received in the premium. Using the 3M option chain from above with a strike of 207.50 (sold for a premium of $1.59 or $159), the maximum profit received by the writer is $159.

The Greeks for this position are as follows:

-

Delta – the delta of an ATM short put would move about –0.491 with the market price. You may already know that absolute value of delta estimates the probability that the option expires in the money. It’s easy to understand why this approximation works in this example as the trader has approximately a 50/50 shot that the option will expire out of the money at expiration.

-

Gamma – the gamma for the short put that is ATM should decrease the delta by 0.1. For the same expiration cycle, gamma will exhibit the largest effect ATM.

-

Theta – theta for the ATM short put, as option’s remaining life decreases, is 0.10 $/d, which is the highest we see across all the strikes . Therefore, ATM short puts provide a significant theta opportunity with a tradeoff of high gamma.

Value of Greeks – Short Put OTM

For an OTM short put, with a strike of 205 and paying $77 in premium, the Greeks are as follows:

-

Delta – the delta of an OTM short put is about –0.27. As the as underlying stock increases by $1/share we’d expect the short put to lose $0.27 in value which is a unrealized profit for the short put trader. When compared with above, you can see that the trader has a higher probability that the put will expire worthless (approx.. 73%).

-

Gamma – the gamma for the short put that is OTM is 0.08. The gamma risk is reduced as we have more “downside protection” by selecting the put further out of the money.

-

Theta – theta for the OTM short put is $0.094/day, which is less than the ATM option but more than the ITM. This shows how much the extrinsic value erodes when ITM options are selected.

Value of Greeks – Short Put Far OTM

A further OTM setup makes the likelihood that an exercise will take place is next to nil. Maximum profit is significantly reduced to $36, but the probability of profit is also the highest at c.a. 85% (1 – delta).

Again, looking at the deep OTM setup for MMM (say $202.50), the Greeks for are:

-

Delta – the delta of a deep OTM short put is around –0.15, which is the lowest delta across the group giving the highest Probability of Profit and highest downside protection.

-

Gamma – the gamma for the short put that is deep OTM is 0.05, meaning that the delta will not see large swings even if the stock moves against the position gradually.

-

Theta – theta for the deep OTM short put is $0.08/day, which is the lowest profitability we’ve seen for theta decay but still greater than the ITM put which becomes a directional bet.

Conclusion

Here is a summary of the values discussed in this article according to the position of the short put relative to the underlying stock:

|

|

Strike |

Delta |

Gamma |

Theta ($/day) |

Probability of Profit |

Premium (intrinsic + extrinsic) |

Premium/Return on Capital |

|

ITM |

210 |

–0.740 |

0.087 |

–0.065 |

~26% |

$300 |

Highest ROI |

|

ATM |

207.50 |

–0.491 |

0.099 |

–0.100 |

~50% |

$160 |

Moderate ROI |

|

OTM |

205 |

–0.272 |

0.077 |

–0.094 |

~78% |

$77 |

Low ROI |

|

Further OTM |

202.50 |

–0.145 |

0.047 |

–0.075 |

~85% |

$36 |

Lowest ROI |

Strike price selection when creating a short put setup dictates potential profit and loss risk potential. In summary:

-

Short put, ITM at entry = highest risk, highest ROI, becomes a directional play

-

Short put, ATM at entry = moderate risk, moderate ROI, highest theta decay

-

Short put, OTM at entry = low risk, low ROI, maintains strong theta and tradeoff with gamma.

-

Short put, deep OTM at entry = lowest risk, lowest ROI, easy to over-leverage if notional risk not properly considered.

It’s apparent from the colors in the table, that a common “rule of thumb” for short put trading is to select strikes slightly out-of-the-money. However, I hope this article challenges you to be more scientific in your strike selection, expand your evaluation of key trading criteria, and recognize that the tradeoff of risk and reward is in continuum across the strikes. There’s no one-size-fits-all rule of thumb.

In the next article, we’ll explore the tradeoffs of expiration cycles with short puts. I would appreciate your feedback and questions on this article as it will help developing the second part.

Drew Hilleshiem is the Co-Founder and CEO of OptionAutomator, an options trading technology startup offering a free options screener that leverages Multi-Criteria Decision Making (MCDM) algorithms to force-rank relevancy of daily options opportunities against user’s individual trading criteria. He is passionate to help close the gap between Wall Street and Main Street with both technology and blogging. You can follow Drew via @OptionAutomator on Twitter.

There are no comments to display.

Join the conversation

You can post now and register later. If you have an account, sign in now to post with your account.

Note: Your post will require moderator approval before it will be visible.