Search the Community

Showing results for tags 'aapl'.

Found 13 results

-

.jpg.4dd0dce727c44ef6a3145d6746e2c2bb.jpg) That's great, because it means there is discord, and discord, especially for Apple ahead of earnings has meant a repeating pattern for the clever trader to take advantage of. One week before Apple's earnings would be January 25th, 2018. Apple's Disagreement Sometimes a bullish momentum bet works great -- and in fact, for Apple that has been a strong pattern ahead of earnings. But with a toppy market, sometimes a different approach can work as well. It turns out, over the long-run, for stocks with certain tendencies like Apple Inc, there is a clever way to trade market anxiety or market optimism before earnings announcements with options. This approach has returned 189% with 10 wins and 2 losses over the last 3-years. The Trade Before Earnings What a trader wants to do is to see the results of buying a slightly out of the money strangle one-week before earnings, and then sell that strangle just before earnings. Here is the setup: We are testing opening the position 7 calendar days before earnings and then closing the position 1 day before earnings. This is not making any earnings bet. This is not making any stock direction bet. Once we apply that simple rule to our back-test, we run it on a 40-delta strangle, which is a fancy of saying, buying both the 40-delta call and 40-delta put, for a non-directional bet on volatility. Returns If we did this long strangle in Apple Inc (NASDAQ:AAPL) over the last three-years, but only held it before earnings, using the options closest to 14 days from expiration, we get these results: AAPL Long 40 Delta Strangle % Wins: 83.3% Wins: 10 Losses: 2 % Return: 189% Tap Here to See the Back-test The mechanics of the TradeMachine™ are that it uses end of day prices for every back-test entry and exit (every trigger). We see a 189% return, testing this over the last 12 earnings dates in Apple Inc. We can also see that this strategy hasn't been a winner all the time, rather it has won 10 times and lost 2 times, for a 83.3% win-rate on an one-week trade. Setting Expectations While this strategy has an overall return of 189%, the trade details keep us in bounds with expectations: ➡ The average percent return per trade was 16.9% over 7-days. ➡ The average percent return per winning trade was 21.8% over 7-days. ➡ The average percent return per losing trade was -7.6% over 7-days. We like the comfort of a trade that, when it loses, it isn't a disaster -- at least not historically. Option Trading in the Last Year We can also look at the last year of earnings releases and examine the results: AAPL Long 40 Delta Strangle % Wins: 100% Wins: 4 Losses: 0 % Return: 98.2% Tap Here to See the Back-test In the latest year this pre-earnings option trade has 4 wins and lost 0 times and returned 98.2%. ➡ Over just the last year, the average percent return per trade was 22.3% over 7-days. WHAT HAPPENED We don't always have to look at bullish back-tests in a bull market -- sometimes a straight down the middle volatility pattern pops up. This is it -- this is how people profit from the option market -- finding trading opportunities that avoid earnings risk and work equally well during a bull or bear market. To see how to do this for any stock we welcome you to watch this quick demonstration video: Tap Here to See the Tools at Work Risk Disclosure You should read the Characteristics and Risks of Standardized Options. Past performance is not an indication of future results.

That's great, because it means there is discord, and discord, especially for Apple ahead of earnings has meant a repeating pattern for the clever trader to take advantage of. One week before Apple's earnings would be January 25th, 2018. Apple's Disagreement Sometimes a bullish momentum bet works great -- and in fact, for Apple that has been a strong pattern ahead of earnings. But with a toppy market, sometimes a different approach can work as well. It turns out, over the long-run, for stocks with certain tendencies like Apple Inc, there is a clever way to trade market anxiety or market optimism before earnings announcements with options. This approach has returned 189% with 10 wins and 2 losses over the last 3-years. The Trade Before Earnings What a trader wants to do is to see the results of buying a slightly out of the money strangle one-week before earnings, and then sell that strangle just before earnings. Here is the setup: We are testing opening the position 7 calendar days before earnings and then closing the position 1 day before earnings. This is not making any earnings bet. This is not making any stock direction bet. Once we apply that simple rule to our back-test, we run it on a 40-delta strangle, which is a fancy of saying, buying both the 40-delta call and 40-delta put, for a non-directional bet on volatility. Returns If we did this long strangle in Apple Inc (NASDAQ:AAPL) over the last three-years, but only held it before earnings, using the options closest to 14 days from expiration, we get these results: AAPL Long 40 Delta Strangle % Wins: 83.3% Wins: 10 Losses: 2 % Return: 189% Tap Here to See the Back-test The mechanics of the TradeMachine™ are that it uses end of day prices for every back-test entry and exit (every trigger). We see a 189% return, testing this over the last 12 earnings dates in Apple Inc. We can also see that this strategy hasn't been a winner all the time, rather it has won 10 times and lost 2 times, for a 83.3% win-rate on an one-week trade. Setting Expectations While this strategy has an overall return of 189%, the trade details keep us in bounds with expectations: ➡ The average percent return per trade was 16.9% over 7-days. ➡ The average percent return per winning trade was 21.8% over 7-days. ➡ The average percent return per losing trade was -7.6% over 7-days. We like the comfort of a trade that, when it loses, it isn't a disaster -- at least not historically. Option Trading in the Last Year We can also look at the last year of earnings releases and examine the results: AAPL Long 40 Delta Strangle % Wins: 100% Wins: 4 Losses: 0 % Return: 98.2% Tap Here to See the Back-test In the latest year this pre-earnings option trade has 4 wins and lost 0 times and returned 98.2%. ➡ Over just the last year, the average percent return per trade was 22.3% over 7-days. WHAT HAPPENED We don't always have to look at bullish back-tests in a bull market -- sometimes a straight down the middle volatility pattern pops up. This is it -- this is how people profit from the option market -- finding trading opportunities that avoid earnings risk and work equally well during a bull or bear market. To see how to do this for any stock we welcome you to watch this quick demonstration video: Tap Here to See the Tools at Work Risk Disclosure You should read the Characteristics and Risks of Standardized Options. Past performance is not an indication of future results. -

.jpg.2fd7aaa09028de5db7353f19d50eba9d.jpg) This options investment strategy involves buying "Deep In The Money" (DITM) options to limit downside risk while retaining the full benefits of the stock. The options are purchased at a lower cost than the actual stock but still receive close to a $1 increase for every favorable $1 move in the underlying security which increases the percentage return for the same dollar move. Advantages of stock replacement strategy: Keeps all benefits associated with trading the stock. Reduces costs associated with owning the stock. Offers more leverage by increasing the potential percentage return. Offers lower downside risk. Disadvantages of a stock replacement strategy: Needs good trading experience and skills to master the strategy. The strategy may fail, when the stock stays on (almost) the same price or moves sidewise. Leverage works both way - If the stock falls, the percentage loss is larger as well. Let's check how you could use this options investment strategy to reduce your cost of owning Apple. The stock closed at $174 yesterday. Experienced options traders are usually well aware of this strategy and make good use of it. Strategy No. 1: Buy 100 shares of the stock Buying 100 shares will cost you $17,400. Not cheap. If the stock rallies to $185, you have made $1,100 or 6%. Let's see how it compares with the stock replacement strategy. Strategy No. 2: Buy DITM call As an alternative to buying the stock, we can buy the AAPL July 20 2018 130 call at $45.47. The cost will be $4,547 which is about 26% of the cost of the 100 shares. The P/L graph looks like this: If the stock rallies to $185, you have made $1,030. This is slightly less than buying the stock, but percentage wise, it is a 23% gain, compared to the 6% gain when owning the stock. Of course the opposite is true as well - if the stock goes down, your percentage loss is much higher. This is called leverage. It works both ways - you increase the reward if the stock rises and increase the risk if the stock falls. However, if the stock falls, the volatility should increase which actually helps our option price because increased volatility can cause option prices to increase or not fall as fast. So basically even though we will gain $1 for every $1 the stock increases we will lose slightly less than $1 for every $1 the stock drops. You might noticed that we gained only 93 cents for every $1 movement in the stock. This is due to the fact that the delta of the 130 call is 0.93. We could choose a call which is deeper in the money - it would have a higher delta and have a better replication of the stock movement. However, it would also be more expensive and provide less leverage. 0.90-0.95 delta provides a good compromise between 1:1 movement and a reasonable price. Now let's see if we can do better. Strategy No. 3: Buy DITM call and sell OTM call against it every month Here is how it works: Buy AAPL July 20 2018 130 call at $45.47 Sell AAPL Feb 16 2018 185 call at $1.55 We reduce the cost of our trade by $155 to $4,392, but we also limited our gains. The P/L graph looks like this: As we can see, we increased the maximum gain to $1,147. This gain is not only larger than the dollar gain from owning the 100 shares of the stock, but also translates to a cool 26% in one month. If the stock is below $185 by February expiration, we can repeat the process with the March options. If it is higher, you just close the trade for a gain and can roll to higher strikes. Of course if you believe that AAPL will be higher than $185 by Feb expiration, you will be better by just buying the DITM calls. Strategy No. 4: Buy DITM call, sell OTM call and buy OTM put Here is how it works: Buy AAPL July 20 2018 130 call at $45.47 Sell AAPL Feb 16 2018 185 call at $1.55 Buy AAPL Feb 16 2018 165 put at $2.07 Our cost now is $4,599, still significantly lower than owning the stock. The P/L graph looks like this: Our gain is now limited to "only" $900 (20%), BUT we also limited our loss to ~13% in case AAPL goes down after earnings. And if the stock really crashes, the position can actually produce some gains because at some point the long put will more than offset the losses from the long call. This is a variation of collar, where we replace the long shares with DITM call. And this is the beauty of options. You have almost endless possibilities to structure your trade, based on your outlook and risk tolerance. Before investing any money, please make sure you understand what you are doing. Good luck.

This options investment strategy involves buying "Deep In The Money" (DITM) options to limit downside risk while retaining the full benefits of the stock. The options are purchased at a lower cost than the actual stock but still receive close to a $1 increase for every favorable $1 move in the underlying security which increases the percentage return for the same dollar move. Advantages of stock replacement strategy: Keeps all benefits associated with trading the stock. Reduces costs associated with owning the stock. Offers more leverage by increasing the potential percentage return. Offers lower downside risk. Disadvantages of a stock replacement strategy: Needs good trading experience and skills to master the strategy. The strategy may fail, when the stock stays on (almost) the same price or moves sidewise. Leverage works both way - If the stock falls, the percentage loss is larger as well. Let's check how you could use this options investment strategy to reduce your cost of owning Apple. The stock closed at $174 yesterday. Experienced options traders are usually well aware of this strategy and make good use of it. Strategy No. 1: Buy 100 shares of the stock Buying 100 shares will cost you $17,400. Not cheap. If the stock rallies to $185, you have made $1,100 or 6%. Let's see how it compares with the stock replacement strategy. Strategy No. 2: Buy DITM call As an alternative to buying the stock, we can buy the AAPL July 20 2018 130 call at $45.47. The cost will be $4,547 which is about 26% of the cost of the 100 shares. The P/L graph looks like this: If the stock rallies to $185, you have made $1,030. This is slightly less than buying the stock, but percentage wise, it is a 23% gain, compared to the 6% gain when owning the stock. Of course the opposite is true as well - if the stock goes down, your percentage loss is much higher. This is called leverage. It works both ways - you increase the reward if the stock rises and increase the risk if the stock falls. However, if the stock falls, the volatility should increase which actually helps our option price because increased volatility can cause option prices to increase or not fall as fast. So basically even though we will gain $1 for every $1 the stock increases we will lose slightly less than $1 for every $1 the stock drops. You might noticed that we gained only 93 cents for every $1 movement in the stock. This is due to the fact that the delta of the 130 call is 0.93. We could choose a call which is deeper in the money - it would have a higher delta and have a better replication of the stock movement. However, it would also be more expensive and provide less leverage. 0.90-0.95 delta provides a good compromise between 1:1 movement and a reasonable price. Now let's see if we can do better. Strategy No. 3: Buy DITM call and sell OTM call against it every month Here is how it works: Buy AAPL July 20 2018 130 call at $45.47 Sell AAPL Feb 16 2018 185 call at $1.55 We reduce the cost of our trade by $155 to $4,392, but we also limited our gains. The P/L graph looks like this: As we can see, we increased the maximum gain to $1,147. This gain is not only larger than the dollar gain from owning the 100 shares of the stock, but also translates to a cool 26% in one month. If the stock is below $185 by February expiration, we can repeat the process with the March options. If it is higher, you just close the trade for a gain and can roll to higher strikes. Of course if you believe that AAPL will be higher than $185 by Feb expiration, you will be better by just buying the DITM calls. Strategy No. 4: Buy DITM call, sell OTM call and buy OTM put Here is how it works: Buy AAPL July 20 2018 130 call at $45.47 Sell AAPL Feb 16 2018 185 call at $1.55 Buy AAPL Feb 16 2018 165 put at $2.07 Our cost now is $4,599, still significantly lower than owning the stock. The P/L graph looks like this: Our gain is now limited to "only" $900 (20%), BUT we also limited our loss to ~13% in case AAPL goes down after earnings. And if the stock really crashes, the position can actually produce some gains because at some point the long put will more than offset the losses from the long call. This is a variation of collar, where we replace the long shares with DITM call. And this is the beauty of options. You have almost endless possibilities to structure your trade, based on your outlook and risk tolerance. Before investing any money, please make sure you understand what you are doing. Good luck. -

These are all trade-able events, at anytime, without concern for earnings. Today we look at exactly what has worked for Apple (AAPL). Take well bounded risk, small, and direction-less, and let a tweet, a news headline, an Apple headline, a day of pessimism or a day of optimism, whatever -- move the market, as it has so often in this new volatility regime. The Short-term Option Volatility Trade in Apple Inc We will examine the outcome of going long a short-term at-the-money (50 delta) straddle, in options that are the closest to seven-days from expiration. But we have a rule -- it's a stop and a limit of 10%, and, we back-test re-opening the position immediately, as opposed to waiting for 5-days later. Here is the stock chart for Apple since October 1st -- focus on the volatility, not the direction -- these are daily candles. Chart from CMLviz.com We can volatility and a general downtrend, in fact, a 14% drop in less than 6 weeks. But let's not worry about direction, let's try to find a back-test that benefits from that volatility that is in fact up 92% in just six-weeks and takes no stock direction risk at all. Here it is, first, we enter the long straddle. Second, we set a very specific type of stop and limit: At the end of each day, the back-tester checks to see if the long straddle is up or down 10%. If it is, it closes the position, and re-opens at the same time, another long straddle, but this one now re-adjusted for what is the newest at-the-money strike price. We have a full blown tutorial write up on this type of stop/limit behavior in the Discover Tab: Stops & Limits Roll Timing What does "open again at normal time" vs "immediately" mean? The Results We back-tested this only over the last six-weeks. We are hyper focusing not on a long drawn out pattern, but rather this time, right now, this period of volatility. AAPL: Long 50 Delta Straddle % Wins: 58.8% Wins: 10 Losses: 7 % Return: 92% Tap Here to See the Back-test The mechanics of the TradeMachine® are that it uses end of day prices for every back-test entry and exit (every trigger). Notice that this has triggered a trade 17 times in the last six-weeks and while the stock has dropped 14%, the option strategy, which takes no directional positioning, is up more than 92% in six-weeks time. This is a fast moving, re-adjusting straddle. The idea is simple: Take well bounded risk, small, and direction-less, and let a tweet, a news headline, an Apple headline, a day of pessimism or a day of optimism, whatever -- move the market, as it has so often in this new volatility regime. Setting Expectations Since we use end of day open and closes, while this strategy has an overall return of 92%, the trade details keep us in bounds with expectations: ➡ The average percent return per trade was 11%. ➡ The average percent return per winning trade was 29.9%. ➡ The percent return per losing trade was -16%. Not only are we seeing a high winning percentage, but also that the average win is twice as large as the average loss. Further, this trade takes no stock direction risk at all. WHAT HAPPENED When the market shifts, we need a minimum amount of data to adjust, and succeed. This is how people profit from the option market -- it's not luck, it's preparation. Tap Here to See the Tools at Work Risk Disclosure You should read the Characteristics and Risks of Standardized Options. Past performance is not an indication of future results. Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment. Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition. Please note that the executions and other statistics in this article are hypothetical, and do not reflect the impact, if any, of certain market factors such as liquidity and slippage. Ophir Gottlieb is the CEO & Co-founder of Capital Market Laboratories. Mr Gottlieb’s learning background stems from his graduate work in mathematics and measure theory at Stanford University and his time as an option market maker. He has been cited by Yahoo! Finance, CNNMoney, MarketWatch, Business Insider, Reuters, Bloomberg, Wall St. Journal, Dow Jones Newswire, Barron’s, Forbes, SF Chronicle, Chicago Tribune and Miami Herald. He created and authored what was believed to be the most heavily followed option trading blog in the world for three-years. Related articles: The Incredible Option Trade In VXX Earnings Momentum Trade In Oracle Post Earnings Option Trade In Facebook Option Trade After Earnings In AutoZone Pre-Earnings Momentum Trade In Netflix Microsoft Pre-Earnings Momentum Trade Post Earnings Trade In FedEx Pre Earnings Pattern In Apple Earnings Momentum Trading In Google PANW Broke The Golden Rule How To Profit From PayPal Volatility

These are all trade-able events, at anytime, without concern for earnings. Today we look at exactly what has worked for Apple (AAPL). Take well bounded risk, small, and direction-less, and let a tweet, a news headline, an Apple headline, a day of pessimism or a day of optimism, whatever -- move the market, as it has so often in this new volatility regime. The Short-term Option Volatility Trade in Apple Inc We will examine the outcome of going long a short-term at-the-money (50 delta) straddle, in options that are the closest to seven-days from expiration. But we have a rule -- it's a stop and a limit of 10%, and, we back-test re-opening the position immediately, as opposed to waiting for 5-days later. Here is the stock chart for Apple since October 1st -- focus on the volatility, not the direction -- these are daily candles. Chart from CMLviz.com We can volatility and a general downtrend, in fact, a 14% drop in less than 6 weeks. But let's not worry about direction, let's try to find a back-test that benefits from that volatility that is in fact up 92% in just six-weeks and takes no stock direction risk at all. Here it is, first, we enter the long straddle. Second, we set a very specific type of stop and limit: At the end of each day, the back-tester checks to see if the long straddle is up or down 10%. If it is, it closes the position, and re-opens at the same time, another long straddle, but this one now re-adjusted for what is the newest at-the-money strike price. We have a full blown tutorial write up on this type of stop/limit behavior in the Discover Tab: Stops & Limits Roll Timing What does "open again at normal time" vs "immediately" mean? The Results We back-tested this only over the last six-weeks. We are hyper focusing not on a long drawn out pattern, but rather this time, right now, this period of volatility. AAPL: Long 50 Delta Straddle % Wins: 58.8% Wins: 10 Losses: 7 % Return: 92% Tap Here to See the Back-test The mechanics of the TradeMachine® are that it uses end of day prices for every back-test entry and exit (every trigger). Notice that this has triggered a trade 17 times in the last six-weeks and while the stock has dropped 14%, the option strategy, which takes no directional positioning, is up more than 92% in six-weeks time. This is a fast moving, re-adjusting straddle. The idea is simple: Take well bounded risk, small, and direction-less, and let a tweet, a news headline, an Apple headline, a day of pessimism or a day of optimism, whatever -- move the market, as it has so often in this new volatility regime. Setting Expectations Since we use end of day open and closes, while this strategy has an overall return of 92%, the trade details keep us in bounds with expectations: ➡ The average percent return per trade was 11%. ➡ The average percent return per winning trade was 29.9%. ➡ The percent return per losing trade was -16%. Not only are we seeing a high winning percentage, but also that the average win is twice as large as the average loss. Further, this trade takes no stock direction risk at all. WHAT HAPPENED When the market shifts, we need a minimum amount of data to adjust, and succeed. This is how people profit from the option market -- it's not luck, it's preparation. Tap Here to See the Tools at Work Risk Disclosure You should read the Characteristics and Risks of Standardized Options. Past performance is not an indication of future results. Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment. Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition. Please note that the executions and other statistics in this article are hypothetical, and do not reflect the impact, if any, of certain market factors such as liquidity and slippage. Ophir Gottlieb is the CEO & Co-founder of Capital Market Laboratories. Mr Gottlieb’s learning background stems from his graduate work in mathematics and measure theory at Stanford University and his time as an option market maker. He has been cited by Yahoo! Finance, CNNMoney, MarketWatch, Business Insider, Reuters, Bloomberg, Wall St. Journal, Dow Jones Newswire, Barron’s, Forbes, SF Chronicle, Chicago Tribune and Miami Herald. He created and authored what was believed to be the most heavily followed option trading blog in the world for three-years. Related articles: The Incredible Option Trade In VXX Earnings Momentum Trade In Oracle Post Earnings Option Trade In Facebook Option Trade After Earnings In AutoZone Pre-Earnings Momentum Trade In Netflix Microsoft Pre-Earnings Momentum Trade Post Earnings Trade In FedEx Pre Earnings Pattern In Apple Earnings Momentum Trading In Google PANW Broke The Golden Rule How To Profit From PayPal Volatility -

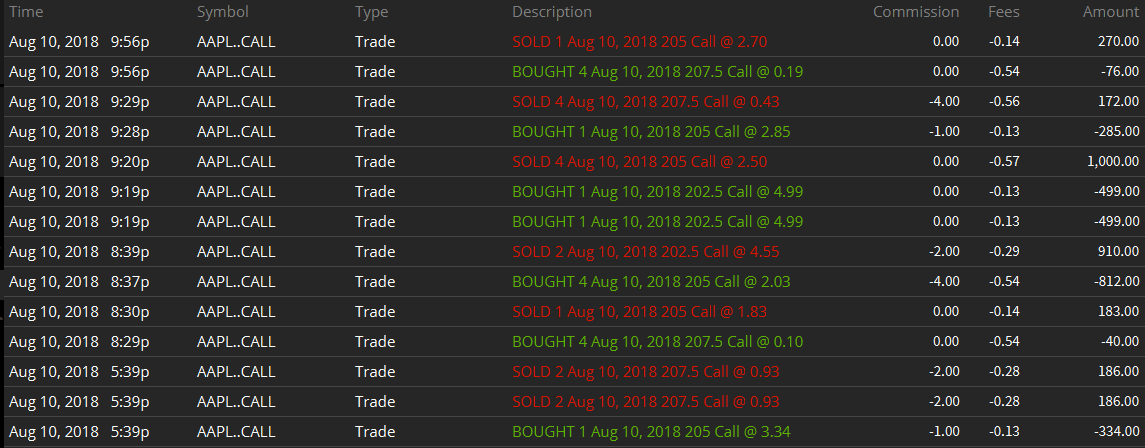

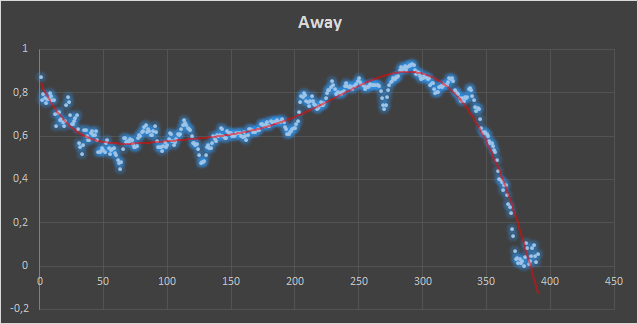

What drew me to this site was Kim professing to apply strategies or trading philosophies as set out in Jeff Augen's books. Besides many things posted on here he also devoted some chapters to stock pinning, i.e. on expiration some stocks tend to gravitate towards a particular strike price. AAPL was and is an example of a stock that often pins to a strike. Jeff did his research on 3rd Friday expiries but I thought to test his theory today for a bit of fun. The actual pinning effect is something I verified by charting minute by minute quotes for AAPL over two years. You get charts like these: Here you see the stock quote from March last year with the Y axis showing how far ($) away from the closest option strike the stock was and the X axis the number of minutes since trading started that day. This plunging chart is very frequent with AAPL as - from the stocks I was able to acquire minute by minute data from - it is the stock that most consistently shows this behaviour - it only failed twice in two years roughly (based on 3rd Friday expiries). Anyway I could never make use of this with my European broker because profits are small and trading is frequent - with minimum 36$ to open and close a position this wasnt feasible. Now I switched to a US broker this became a possibility. So for fun I tried this today on a non 3rd Friday expiry and I can say AAPL duly obliged: I picked up the trading at 11.40 AM EST - you can start earlier but this is usually a midday lull that creates a stable time to open your position. The strategy is to use ratio trades to make profits on low capital investment. The stock was around 208.40$ and in line with the strategy we guessed that 207.50$ mark would be the close hence OB 1 C 205 @ 3.34$ and OS 4 C 202.50 @ 0.93$ for a net credit. The stock duly obliged and tumbled; in fact below 207.50$ to 206.80$ or so by which time I closed the trade. Now we retained the theory that at close it would be 207.50 so this time we did a different ratio and sold the 2 C 202.50 @ 4.55$ and bought 4 C 205 @ 2.03 again for a net credit. AAPL proved particularly tractable and by 4.20 PM EST it was trading around 207.85$ so we closed. The 0.40$ credit on the 207.50$ calls beckoned again. Therefore we repeated the setup of the morning except this time of course the trade was a net debit. I watched smugly as AAPL duly converged back down to the strike price - with 9 minutes till session close I was reckoning to close at the last minute. Except... my internet went down at that moment with 4 ITM shorts! Slight panic - router reboot and thank goodness Internet worked again (ouf!) I closed out immediately just in case another gremlin would be thrown up. In doing so I gave up a little profit as AAPL closed at 207.53 $ like a champ of pinning. Profit from all this excitement: $ 362 after commissions - the capital outlay was never more than 2K (but this is a slight cheat because I have an AAPL long position in my portfolio) - anyway 18% in the day and a good bit of fun with a slightly unpleasant bit of excitement toward the end!

-

Apple Options Trade After an Earnings Beat

Ophir Gottlieb posted a article in SteadyOptions Trading Blog

.jpg.20ae6b78978aba7c963801d659caf403.jpg) There is a bullish momentum pattern in Apple Inc (NASDAQ:AAPL) stock 2 calendar days after earnings, if and only if the stock showed a large gap up after the actual earnings announcement. This is a conditional entry -- the company reports earnings and if the stock move off of that report is a 3% gain or larger, then a bullish position is back-tested looking for continuing momentum. The event is rare, but when it has occurred, the back-test results are noteworthy. Apple Inc (NASDAQ:AAPL) Earnings In Apple Inc, if the stock move immediately following an earnings result was large (3% or more to the upside), if we test waiting two-days after that earnings announcement and then bought a three-week at the money (50 delta) call, the results were quite strong. This back-test opens two-days after earnings were announced to try to find a stock that continues an upward trajectory after an earnings rally. Simply owning options after earnings, blindly, is likely not a good trade, but hand-picking the times and the stocks to do it in can be useful. We can test this approach without bias with a custom option back-test. Here is the timing set-up around earnings: Rules Condition: Wait for the one-day stock move off of earnings, and if it shows a 3% gain or more in the underlying, then, follow these rules: Open the long at-the-money call two-calendar days after earnings. Close the long call 14 calendar days after earnings. Use the options closest to 21 days from expiration (but more than 14 days). This is a straight down the middle direction trade -- this trade wins if the stock is continues on an upward trajectory after a large earnings move the two-weeks following earnings and it will stand to lose if the stock does not rise. This is not a silver bullet -- it's a trade that needs to be carefully examined. But, this is a conditional back-test, which is to say, it only triggers if an event before it occurs. RISK CONTROL Since blindly owning calls can be a quick way to lose in the option market, we will apply a tight risk control to this analysis as well. We will add a 40% stop loss and a 40% limit gain. In English, at the close of every trading day, if the call is up 40% from the price at the start of the trade, it gets sold for a profit. If it is down 40%, it gets sold for a loss. This also has the benefit of taking profits if there is a stock rally early in the two-week period rather than waiting to close 14-days later. Another risk reducing move we made was to use 21-day options and only hold them for 14-days so the trade doesn't suffer from total premium decay. RESULTS If we bought the at-the-money call in Apple Inc (NASDAQ:AAPL) over the last three-years but only held it after earnings and after an earnings pop higher, we get these results: AAPL Long 50 Delta Call % Wins: 80% Wins: 4 Losses: 1 % Return: 151.9% Tap Here to See the Back-test The mechanics of the TradeMachine® are that it uses end of day prices for every back-test entry and exit (every trigger). Looking at Averages The overall return was 151.9%; but the trade statistics tell us more with average trade results: ➡ The average return per trade was 46.54% over each 12-day period. ➡ The average return per winning trade was 76.92% over each 12-day period. ➡ The average return per losing trade was -75% over each 12-day period. WHAT HAPPENED Bullish momentum and sentiment after of earnings can be quite powerful with the tailwind of an earnings beat. This is just one example of what has become a tradable phenomenon in Apple. To identify patterns that have repeated over and over again, empirically, we welcome you to watch this quick demonstration video: Tap Here to See the Tools at Work Risk Disclosure You should read the Characteristics and Risks of Standardized Options. Ophir Gottlieb is the CEO & Co-founder of Capital Market Laboratories. Mr Gottlieb’s learning background stems from his graduate work in mathematics and measure theory at Stanford University and his time as an option market maker on the NYSE and CBOE exchange floors. He has been cited by Yahoo! Finance, CNNMoney, MarketWatch, Business Insider, Reuters, Bloomberg, Wall St. Journal, Dow Jones Newswire, Barron’s, Forbes, SF Chronicle, Chicago Tribune and Miami Herald and is often seen on financial television. He created and authored what was believed to be the most heavily followed option trading blog in the world for three-years.This article is used here with permission and originally appeared here.

There is a bullish momentum pattern in Apple Inc (NASDAQ:AAPL) stock 2 calendar days after earnings, if and only if the stock showed a large gap up after the actual earnings announcement. This is a conditional entry -- the company reports earnings and if the stock move off of that report is a 3% gain or larger, then a bullish position is back-tested looking for continuing momentum. The event is rare, but when it has occurred, the back-test results are noteworthy. Apple Inc (NASDAQ:AAPL) Earnings In Apple Inc, if the stock move immediately following an earnings result was large (3% or more to the upside), if we test waiting two-days after that earnings announcement and then bought a three-week at the money (50 delta) call, the results were quite strong. This back-test opens two-days after earnings were announced to try to find a stock that continues an upward trajectory after an earnings rally. Simply owning options after earnings, blindly, is likely not a good trade, but hand-picking the times and the stocks to do it in can be useful. We can test this approach without bias with a custom option back-test. Here is the timing set-up around earnings: Rules Condition: Wait for the one-day stock move off of earnings, and if it shows a 3% gain or more in the underlying, then, follow these rules: Open the long at-the-money call two-calendar days after earnings. Close the long call 14 calendar days after earnings. Use the options closest to 21 days from expiration (but more than 14 days). This is a straight down the middle direction trade -- this trade wins if the stock is continues on an upward trajectory after a large earnings move the two-weeks following earnings and it will stand to lose if the stock does not rise. This is not a silver bullet -- it's a trade that needs to be carefully examined. But, this is a conditional back-test, which is to say, it only triggers if an event before it occurs. RISK CONTROL Since blindly owning calls can be a quick way to lose in the option market, we will apply a tight risk control to this analysis as well. We will add a 40% stop loss and a 40% limit gain. In English, at the close of every trading day, if the call is up 40% from the price at the start of the trade, it gets sold for a profit. If it is down 40%, it gets sold for a loss. This also has the benefit of taking profits if there is a stock rally early in the two-week period rather than waiting to close 14-days later. Another risk reducing move we made was to use 21-day options and only hold them for 14-days so the trade doesn't suffer from total premium decay. RESULTS If we bought the at-the-money call in Apple Inc (NASDAQ:AAPL) over the last three-years but only held it after earnings and after an earnings pop higher, we get these results: AAPL Long 50 Delta Call % Wins: 80% Wins: 4 Losses: 1 % Return: 151.9% Tap Here to See the Back-test The mechanics of the TradeMachine® are that it uses end of day prices for every back-test entry and exit (every trigger). Looking at Averages The overall return was 151.9%; but the trade statistics tell us more with average trade results: ➡ The average return per trade was 46.54% over each 12-day period. ➡ The average return per winning trade was 76.92% over each 12-day period. ➡ The average return per losing trade was -75% over each 12-day period. WHAT HAPPENED Bullish momentum and sentiment after of earnings can be quite powerful with the tailwind of an earnings beat. This is just one example of what has become a tradable phenomenon in Apple. To identify patterns that have repeated over and over again, empirically, we welcome you to watch this quick demonstration video: Tap Here to See the Tools at Work Risk Disclosure You should read the Characteristics and Risks of Standardized Options. Ophir Gottlieb is the CEO & Co-founder of Capital Market Laboratories. Mr Gottlieb’s learning background stems from his graduate work in mathematics and measure theory at Stanford University and his time as an option market maker on the NYSE and CBOE exchange floors. He has been cited by Yahoo! Finance, CNNMoney, MarketWatch, Business Insider, Reuters, Bloomberg, Wall St. Journal, Dow Jones Newswire, Barron’s, Forbes, SF Chronicle, Chicago Tribune and Miami Herald and is often seen on financial television. He created and authored what was believed to be the most heavily followed option trading blog in the world for three-years.This article is used here with permission and originally appeared here. -

Given the power of stock options to leverage your investment dollars, you might be tempted to bet on the AAPL earnings report coming out today by buying Apple calls (if you think the stock is going up) or Apple puts (if you want to bet that it will go down). That bet paid off handsomely in July 2016 when Apple reported earnings. The stock rose 6.5% the next day and the value of Apple’s weekly calls increased dramatically. But that’s the exception, not the rule. As I showed in one of my Seeking Alpha articles, buying either puts or calls just before Apple’s earnings report is, on average, a losing proposition. When you look at longer timeframe, AAPL tends to move less than expected. Take a look at the screenshot from optionslam.com, showing the post earnings movement of the stock in the last 10 cycles: The explanation for those numbers is simple. Over time, the options tend to overprice the potential post-earnings move. Those options experience huge volatility drop the day after the earnings are announced. In most cases, this drop erases most of the gains, even if the stock had a substantial move. The last column shows the one day post earnings performance of the weekly straddle. As we can see, it has lost money 8 out of 10 times. Which means that 8 out of 10 times the stock moved less than expected. If I had to choose, I would take the other side of the trade (selling those options). Jeff Augen, a successful options trader and author of six books, agrees: "Trying to predict the future is like driving down a country road at night with no headlights on and looking out the back window." - Peter Drucker Related articles: Is Your Risk Worth The Reward? Why We Sell Our Straddles Before Earnings Risk Reward Or Probability Of Success? Whatever You Do, Don't Do This Before Apple's Earnings How NOT To Gamble On AAPL Earnings Want to learn how to trade options in a less risky way? Start Your Free Trial

Given the power of stock options to leverage your investment dollars, you might be tempted to bet on the AAPL earnings report coming out today by buying Apple calls (if you think the stock is going up) or Apple puts (if you want to bet that it will go down). That bet paid off handsomely in July 2016 when Apple reported earnings. The stock rose 6.5% the next day and the value of Apple’s weekly calls increased dramatically. But that’s the exception, not the rule. As I showed in one of my Seeking Alpha articles, buying either puts or calls just before Apple’s earnings report is, on average, a losing proposition. When you look at longer timeframe, AAPL tends to move less than expected. Take a look at the screenshot from optionslam.com, showing the post earnings movement of the stock in the last 10 cycles: The explanation for those numbers is simple. Over time, the options tend to overprice the potential post-earnings move. Those options experience huge volatility drop the day after the earnings are announced. In most cases, this drop erases most of the gains, even if the stock had a substantial move. The last column shows the one day post earnings performance of the weekly straddle. As we can see, it has lost money 8 out of 10 times. Which means that 8 out of 10 times the stock moved less than expected. If I had to choose, I would take the other side of the trade (selling those options). Jeff Augen, a successful options trader and author of six books, agrees: "Trying to predict the future is like driving down a country road at night with no headlights on and looking out the back window." - Peter Drucker Related articles: Is Your Risk Worth The Reward? Why We Sell Our Straddles Before Earnings Risk Reward Or Probability Of Success? Whatever You Do, Don't Do This Before Apple's Earnings How NOT To Gamble On AAPL Earnings Want to learn how to trade options in a less risky way? Start Your Free Trial -

Here it is -- a portfolio of FAANG stocks using pre-earnings trading. A 3:30 video that is staggering and includes some robustness testing. Reminder that you can sign up for Trade Machine as a Steady Options member here: https://cmlviz.com/register/cml-trademachine-49-mo-promotion-so/

-

Trading options pre-earnings -- 1 minute 25 second video. (example: $AAPL) As a Steady Options member, you can get a promotional price, here: Try the Back-tester

-

In one of my previous articles I described a study done by tastytrade, claiming that buying premium before earnings does not work. The title of the study was "We Put The Nail In The Coffin On "Buying Premium Prior To Earnings". I demonstrated that their study was highly flawed, for several reasons (strikes selection, stocks selection, timing etc.) It seems that they did now another study, claiming to get similar results. Click here to view the article

-

I'm looking to add some positive theta to the portfolio. Looking at AAPL, we can see that it is stuck in the 430-470 range in the last few weeks. I don't see any catalyst that will take it much higher or much lower before the next earnings. I'm looking to enter the August/July 450 call calendar, currently trading around 5.50. This is a trade that will do best if there is not much movement between now and July expiry. Since August captures earnings, the options will hold value much better than July as time goes by in the next month. The IV of August options is still pretty low at 28% and it expected to increase as we get closer to earnings. VXAPL which is AAPL volatility index is at 27.30 which is very low compared to historical levels. The time frame for this trade is around 2-4 weeks and the profit target is 20-30%. I'm planning entering in the next few days. We did a similar trade 3 months ago and closed it for 25.7% gain. This time the IV is even lower and it should benefit the trade. P/L chart is attached.

-

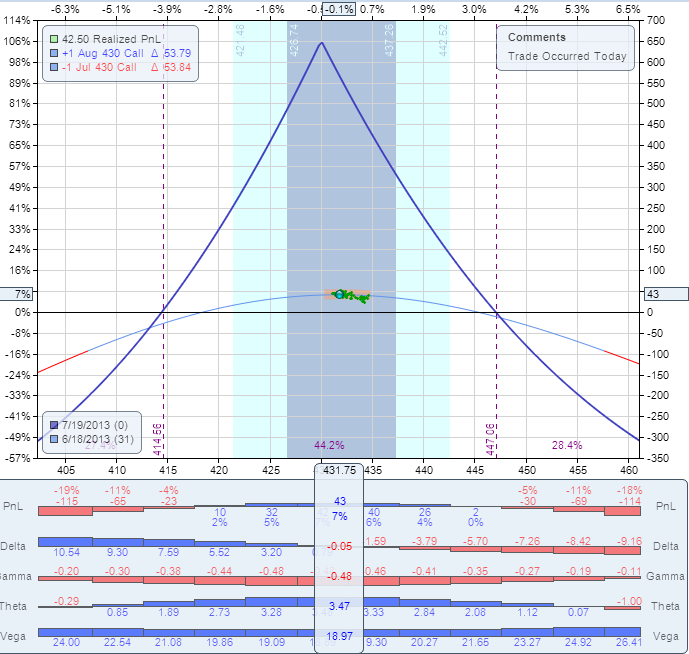

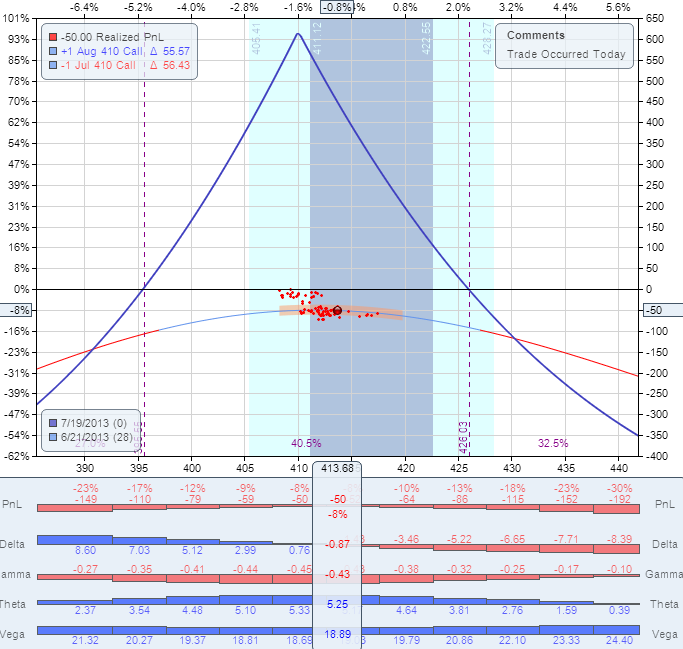

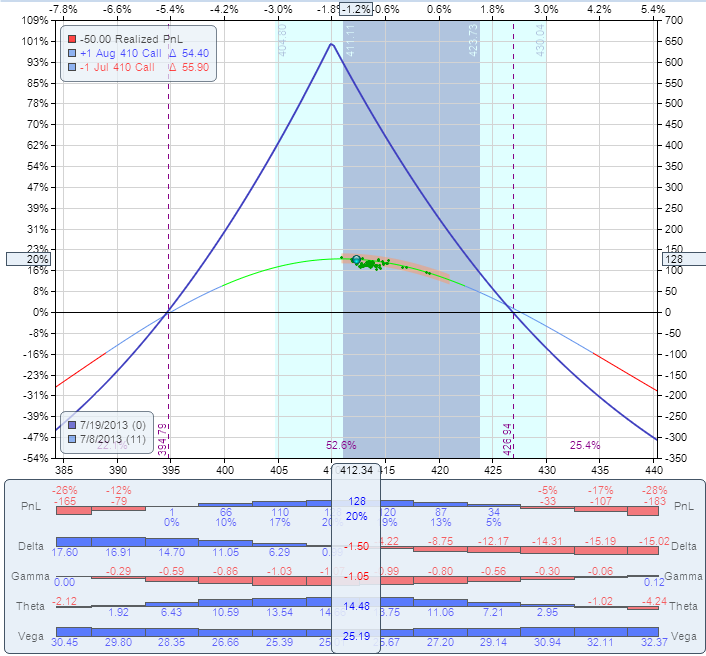

I usually don't do post-mortem on our trades - most of them are short term, we are in the trade just few days, close them and move on. However, this trade is worth to do a post-mortem so we all can learn from it. Background: When we trade a calendar spread, we have two Greeks working for us: the Theta (time decay) and the Vega (IV). We have one Greek working against us: the Gamma (stock movement). The trade makes money if the stock stays in the range and IV does not decline. It can lose if the stock moves, but even if the stock doesn't move, IV decline can kill the trade. The AAPL trade was opened on May 31 and structured in the following way: Buy to open AAPL August 16 2013 450 call Sell to open AAPL July 19 450 call Price: $5.50 debit. The P/L chart looked like this: Since AAPL is scheduled to report earnings on July 23, the long options expire after earnings and they were expected to hold value. The IV of August options was around 27% which is pretty low. It was expected to rise as we get closer to earnings. Fast forward to June 18. The stock is trading slightly below 430. The trade was up ~6% at this point. This is our adjustment point. The correct action was to roll the trade to 430 strike, by selling the 450 calendar and buying the 430 calendar, same expiration. The roll would cost $0.75. The new P/L chart would look like this: Fast forward to June 21. The stock is trading around 413. The trade was down ~8% at this point. This is our second adjustment point. The correct action was to roll the trade to 410 strike, by selling the 430 calendar and buying the 410 calendar, same expiration. The roll would cost $0.30. The new P/L chart would look like this: The stock continued drifting lower, but it did not reach the next adjustment point. After briefly going below $400, it reversed and came back to $412 on July 8 and could be closed for 20% gain: Why didn't we do it and what can be learned here? When the stock reached $425, I estimated that it is oversold and is not going much lower. The IV of August options was still at very low levels. I expected it to start rising as we get closer to earnings. The IV rise would at least partially offset the gamma losses. It did not happen. In fact, today the IV of August options is still around 29% which never happened. The IV of the monthly options before earnings was never below 35%, usually closer to 40%. To add insult to injury, when the stock reached $410, I added a "hedge" by opening a short term 410 calendar. This calendar has lost another $0.60, adding to the overall loss. It also increased the overall investment by almost 40%. This was throwing good money after bad. After the stock recovered to $430, I had a chance to close it for breakeven, but I left it open - again, due to the expectation that IV of the August options just cannot remain that low. The trade was finally closed today for 35% loss. Few things contributed to the big loss: 1. The stock moved more than 50 points at some point which is almost 2 SD (Standard Deviations). 2. The IV of the long options was almost unchanged before earnings which is extremely unusual. 3. The "hedge" added to the loss". 4. The trade was not adjusted in time. Expecting the IV to rise was a reasonable expectation. It did not happen, but there was a high probability that it will. We trade probabilities. There is a big difference between probability and certainty. There was a high probability that IV will not stay that low, based on historical patterns. However, high probability is still not certainty, and IV did not rise as I expected. When something happens few cycles in a row, we have a reasonable expectation that it will happen again. We trade based on those expectations, but we know that patterns not always repeat. In this trade, the main mistake was not expecting the IV rise - the main mistake was not to adjust when the price got to the adjustment point. The trade was actually up 12% after few days, and some members closed it for a gain. My original profit target was 20-25%. I don't think it was a mistake not to take profits at 12%. While there is nothing wrong to set a 10% target on those trades, I like to set higher profit targets, based on my experience with those trades. The bottom line is that despite the unfavorable conditions, with proper management we could still make 15-20% on this trade. The main lesson from this trade: When trading non-directional strategies, never let your opinion affect the trade. Always follow the rules, adjust in time, no matter how oversold or overbought the stock looks.

-

In the realm of sounding like a complete hypocrite -- I just entered an AAPL calendar. With the lower volatility over the last 10 days, it actually fit my model perfectly. The trade: Bought July 21 560 Call @34.83 Sold May 19 560 Call @12.98 I particularly like this trade as it has so much time left in it and stands a very real chance of paying for itself in the next two weeks. AAPL is consolidating around 560, and with the trend down, I moved down 2 strikes to give me some flex room on the declining price. However, even with a 20pt jump up, I can still expect to be getting close to $2.00 per week. With 10 weeks left in the trade (I DONT plan on holding that long), that would still make it worth it. However, a word of caution, AAPL is a MUCH more volatile stock at heart, and this one bears close watching. It is a higher risk trade and should be treated as such. (I weight high risk trades differently than lower risk trades -- one half a position size). The other trade I'm going to look at over the weekend is the AAPL DITM leap trade. I'll post a full anlaysis of this calendar over the weekend.

-

I just entered a weekly IC on AAPL: AAPL @ 567 560/565/570/575 IC filled at $4.10 Maximum profit, 21.95% on AAPL moving $7.00 or more. Busy getting weekly trades in, will fill in with more detail later.