DubMcDub

-

Posts

203 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

SteadyOptions Trading Blog

Forums

Everything posted by DubMcDub

-

Yeah, that makes it pretty clear that they're not furloughing frontline ICU people, which is exactly what I thought. So I'm not sure what your point is. Empty hospital wings for elective surgeries and ambulatory care (meaning outpatient care) does not mean we "flattened the curve too much." It means the hospitals reallocated resources toward ICU and patients most likely to die in the short term.

-

Are you sure you're not thinking of hospital support staff and non-frontline ICU positions being furloughed? I have not seen any evidence that frontline ICU workers are getting furloughed, and I find that very hard to believe. If you some some evidence of that, please post it. There's certainly evidence that plenty of healthcare workers are having to miss work because they're sick with COVID. I have four different friends who are nurses in four different major cities, and they've all caught the virus.

-

Option Alpha's Post/Backtest on Earnings Trades

DubMcDub replied to FrankTheTank's topic in General Board

My basic thought on that article is that it didn't test SO's strategies or really anything all that close to them. Systematically and indiscriminately buying straddles on a predetermined universe of stocks X days before earnings and selling them Y day before earnings (or after earnings) is not what we do here. -

@Kim (or any other ONE user): I keep having an issue with certain positions where the PnL in the risk chart shows 0 (with "NaN%" below it), despite the fact that I have committed the trade, the trade analysis shows my correct cost basis, and am getting live streaming data via IB. I've tried restarting the software and refreshing the live data, to no avail. Have any of you had this issue? Obviously I'll contact ONE support if needed, but I thought it'd be easier to just ask the brain trust first.

-

Ah, it makes sense now. Thanks much on both counts.

-

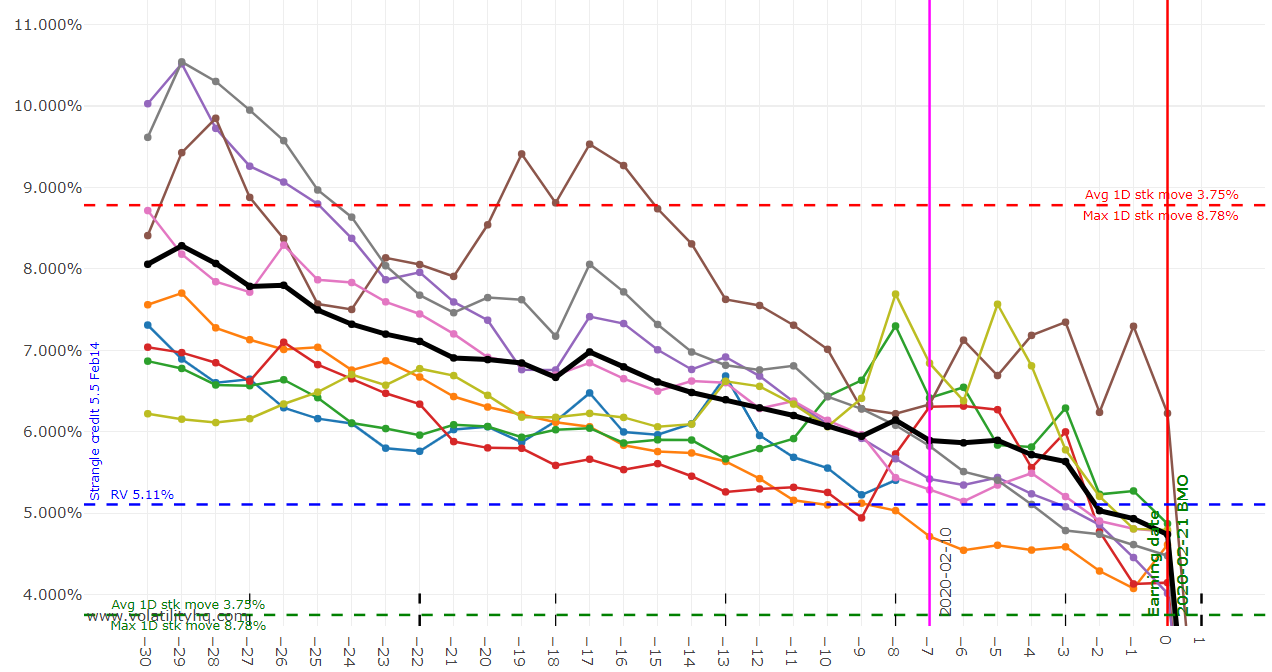

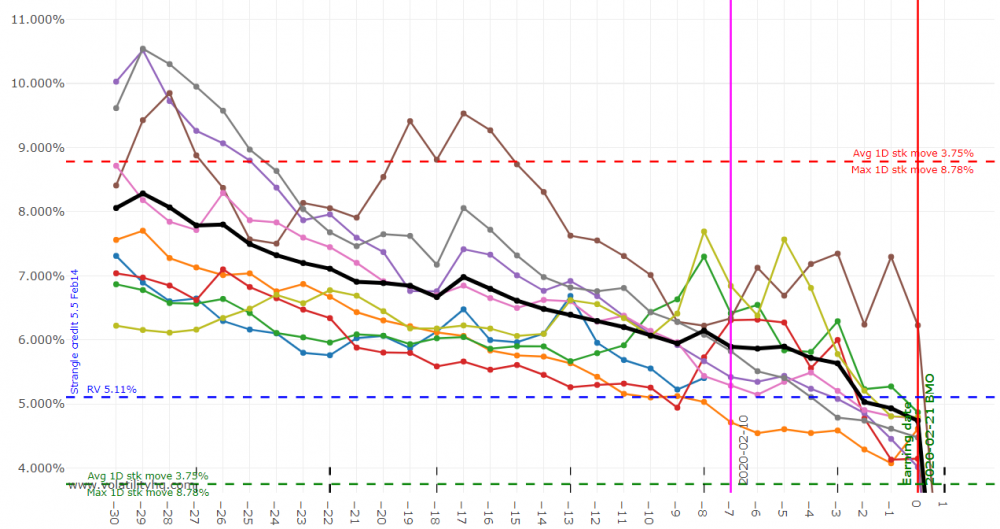

One question and one feature suggestion/request for @Djtux: 1) Can someone explain to me how to interpret the two red and green dotted lines on the straddle RV chart? I assume the text next to these lines is indicating the average and max 1-day move of the stock after the earnings announcement for the last ___ cycles (correct me if I'm wrong about that). But I don't understand exactly what the placement of the dotted line signifies. Perhaps it is very obvious and I'm just stupid. Also, apologies if this has been answered elsewhere. 2) Would it be possible to add the company name somewhere to the charts and tables? Most of the symbols are familiar and well-known, but every now and then I encounter one that I'm not familiar with. It would be nice to be able to see the name right there on the chart as a reminder.

-

Time decay can occur both during trading hours and overnight. You probably know this, but keep in mind that Black-Scholes (and other options pricing models) are just models.There is no way to perfectly, or even near perfectly, calculate time decay with precision, because the only thing that actually affects an option's price is the order flow. For example, if buyers suddenly decide they're willing to pay more for an option near expiration, the option could stay the same price (or even increase) despite what should be strong time decay. This can happen even if the stock price hasn't moved. The options pricing model would explain this phenomenon by increasing the option's IV (i.e., the IV increase offsets the theta). Not sure if this fully answered your question, but hope it helps somewhat.

-

Thanks, @CJ912 and @agsb. Very helpful. I do travel and trade mobile a lot, so it sounds like this may not be the best option for me. That is one area where IB really stands out positively (I personally do not like TW's mobile app as much, but it may be that I just don't have the hang of it fully yet). @agsb, does Tradier run fairly well in a browser on your phone?

-

How is everyone liking the Tradier/Tradehawk combo? I'm a long-time IB customer, and I really like IB in almost all respects, but I must admit that the prospect of saving so much on commissions is tantalizing. At the same time, I'm willing to pay more in commissions for a better product. So I'd be curious to hear the thoughts of folks who are currently using Tradier, especially if you've also used IB at some point and can compare the two.

-

Likewise, @CJ912.

-

Thanks, @Christof+. Appreciate the offer. PM sent.

-

From what I can tell, these two services appear to be what most SO traders use for RV charting. Both seem to be good in quality. Does anyone have thoughts about how the two stack up against each other? Any key features in one but not the other? Any reason to subscribe to both? I may end up just sampling both for awhile, but I would love to get some input from the rest of you first. No reason to spend money unnecessarily if one would better suit my needs.

-

New to SO and to the board (hi, everyone), but just wanted to throw my hat in and say I'd also be in to negotiate a better deal with TW as a group.