josh8790

-

Posts

7 -

Joined

-

Last visited

josh8790's Achievements

Newbie (1/5)

0

Reputation

-

josh8790 changed their profile photo

josh8790 changed their profile photo -

You're right! This was data from Optionscast, I wonder how much of it has this error. Those of you running backtests, where are you getting your data?

-

I calculated it myself using Black-Scholes. I'm not familiar with the ONE software, but I know TradeStation uses IV number derived from all options - maybe ONE uses that as well? Maybe this wasn't a good example, Augen shows stocks that go from 90% IV to 10% after earnings. 33% isn't that high to begin with.

-

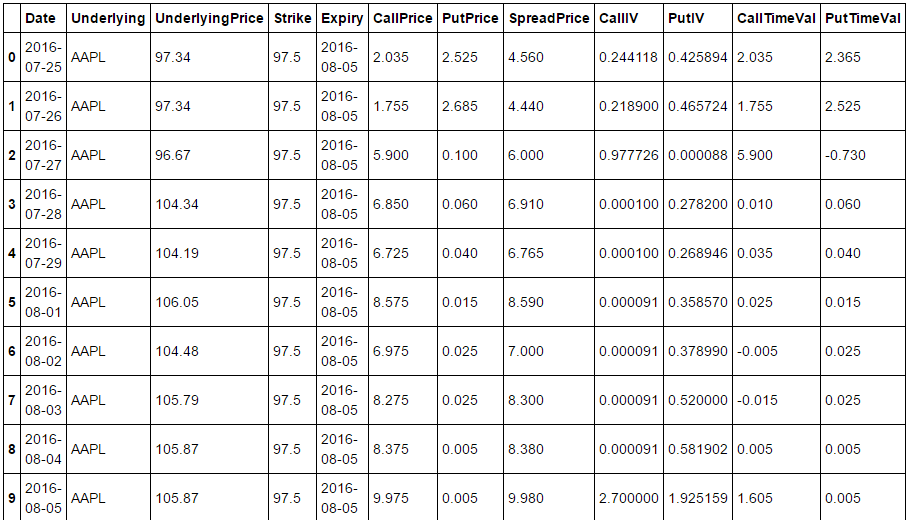

Hey guys this is my first post, I just want to say I think you have a great thing going here. I read The Volatility Edge in Options Trading a year ago and I've been back-testing strategies in my spare time since then. I want to talk to other's about Augen's strategies and that's how I ended up here. I've been looking at data centered on the IV collapse that happens after earnings announcements and I've noticed cases that occur fairly regularly where earnings have been announced but IV does not collapse the following day or at all. The AAPL announcement on 2016-07-26 (after market close) is one example. The stock does not react until 2016-07-28, which doesn't seem to make sense. The IV of a put continues to increase all the way until expiration. Any idea why IV is not collapsing like usual in this case?