Davidkot81

-

Posts

52 -

Joined

-

Last visited

-

Days Won

2

Davidkot81's Achievements

Member (3/5)

11

Reputation

-

I have read about intraday testing, being a really good feature if possible. This is extraordinarily expensive to implement so feature like that would probably necessitate either a premium level of membership required to add more money per month, Ir a possible huge increase in the price for new members. Also what would be interesting to see results of the trade ideas generated emails, and see if there’s an advantage prospectively. If there is, but I think that in and of itself shows the value of the back tester.

-

Ib or tastyworks have the lowest rates ib has been doing things longer

-

It would be better to have at least 20-30 data points before concluding anything. Dustin's charts approach this, and prospectively arrived at data (5 years of forward pointing, good results) show it is a promising strategy. After several years of data, that's what brought me here. It would be interesting to do a subcategory analysis (what worked, and what didn't) here. It would be helpful for the viz software to look at randomly arrived at criteria and compare them to specified criteria for many data points. Then you would have a better idea at the validity and usefulness of the tool (also a lot of work)

-

I would be very cautious about this study. You need a number of occurences of at least 30-40 to claim any significant result. With an n of 4 your evidence to support a claim of investing right after earnings in TWTR is fair, at best

-

..

-

This is fascinating stuff Ophir, has the engine been updated to do custom strategies yet? so what i am getting here is that earnings trades done just after earnings are consistently profitable with much less risk. I have been working on manually backtesting something similar- seeing that calendar spreads expiring in 1-2 days on facebook did extremely well the next day after earnings.

-

Yes sorry I added it up incorrectly, 160 total contracts is correct $200 total commission for TOS and $120 for IB

-

Thanks for the feedback aiti Commissions are not included in my model and would be about $150 in tos with no ticket charge. Maybe about $90 in IB though. Total number of contracts is 120 round trip, corrext. I used all calls. This can bring up possible assignment issues if there is a dividend for TLT. Not aure I understand the "99 delta" issue. you need to hold the trade at least 30-40 days to realize gains. Precisely how long is still a matter of study I am worling on... correction* 160 total contracts so $120 in IB and either $200 or $160 in TOS depending if you have ticket charges

-

Doing this trade in options on bonds (/ZB) is much more favorable and you can get portfolio margining (bpr for me was $55, with true risk of $2100). Credit received was $900. also day by day there can be variation in the credit (some days terrible and not tradeable, others more generous than average)

-

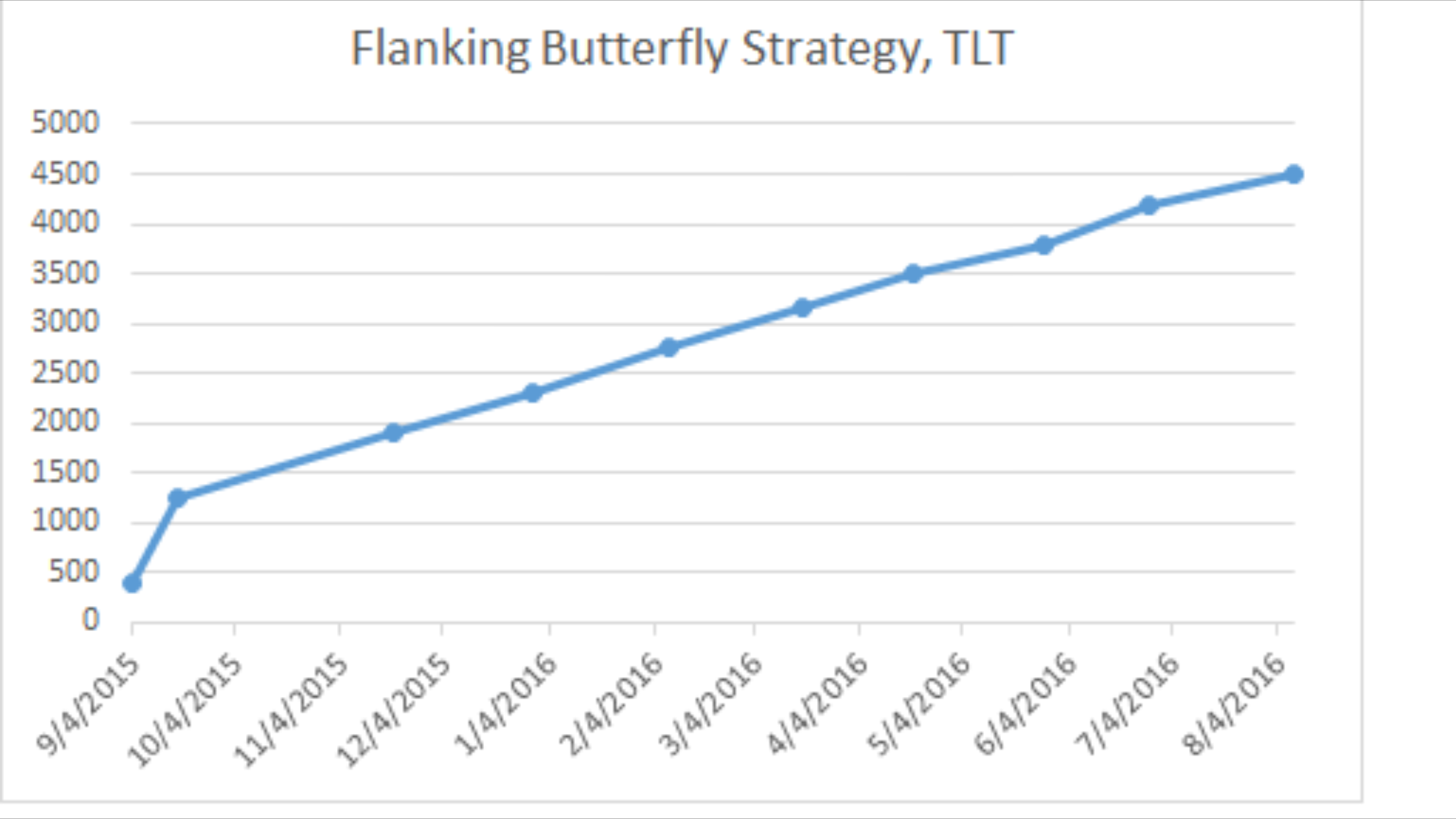

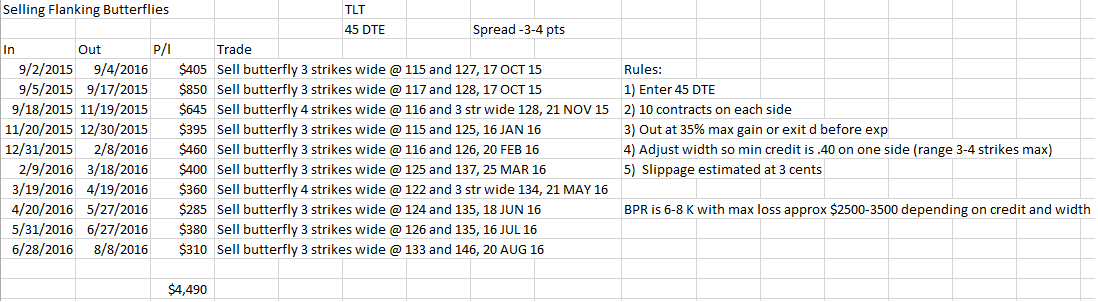

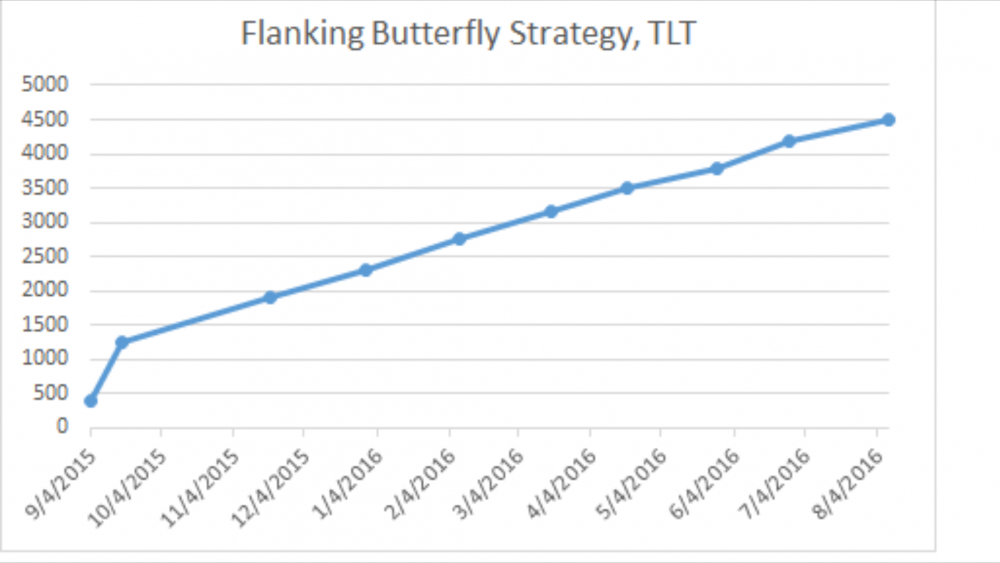

I get out if 35% of max credit. Probably better to get out if 0.5x credit loss but I need to re-backtest, since this backtest did not have a stoploss component. The credit is typically 0.8 to 1.2 or so (estimated) so approximately correct, yes that you aim for $350 for a risk of $2000 which will significantly improve the chance of success However unfortunately your buying power reduction is about $5000 because you cant send a six legged spread. Since TLT cannot be in the middle of both butterflies at expiration you get double the credit for really only the risk of one butterfly or about $2000 max loss. By looking at the deltas, the chance the price will land on the danger areas is about 35% at expiration without management. In most cases, gains are realized about 1 week before expiration. It might be also reasonable to get out the week before expiry for all occurrences, or at least look at the losers (so far none) and find and get out before a drawdown in the short butterflies. To be conservative this would give you a gain of about $375 with about $2000 of loss potential and $5000 buying power reduction or about 7.5% on your 5000 after about 40 days. Without managing at 35% Likely results in loss (chance of loss is probably about 35-40%) In other simulations, managing at 35% of profit probably cuts the risk to about 18% but more backtesting is needed.

-

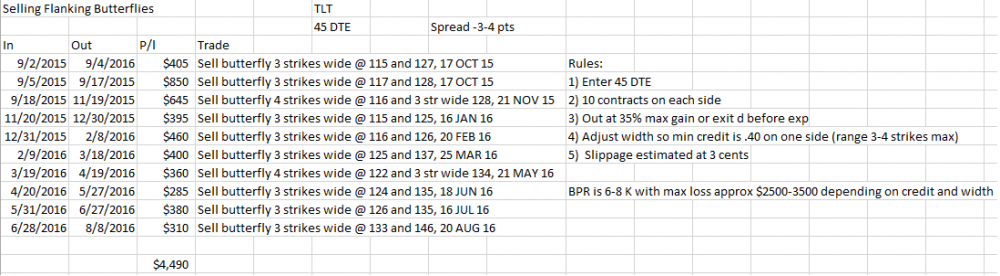

Hi Kim Sure- so six strikes wide would be for example: sell 1 lot of the 127 strike buy 2 lots of the 130 srike sell 1 lot of the 133 strike Two flanking butterflies are sold so a credit is received (no debit) My goal was to exit the trade once 35% of the credit received as attained In this backtest there is no stoploss. You could consider a 1.5x credit received stoploss, or increased duration of trade to say 90 dte, and I will work on backtesting these. as an example take the May 31 trade, where a six wide butterfly was sold around the 126 strike and the second butterfly was sold at the 135 strike. Therefore you would for example sell one lot of the 123 strike, 2 lots of the 126 strike would be bought, and one lot of the 129 strike would be sold. A second similar butterfly centered at the 135 strike would also be sold (sell 132 strike x1, buy 135 strike x2 and sell 138 strike x1). For this backtest all options traded were calls.

-

New Analysis: Flanking butterflies. In this environment, with low IV pervasively affecting all of us, there is low volatility generally in the index funds and in the bonds. For TLT, I hypothesized that selling flanking butterflies (c. 1 standard deviation from current price), 6 or so strikes wide, might be profitable. There is more risk here than other trades, since if the price falls exactly in the middle of the sold butterfly in one of the spreads, the max loss is 3-4 K minus the credit received (usually about 1 K). This though hasn't happened yet. To further minimize the risk, can see what happens with longer duration and also tighter spreads, for a future analysis. Recommend at least 20K if trying this strategy, and again just for learning, not a recommendation.

-

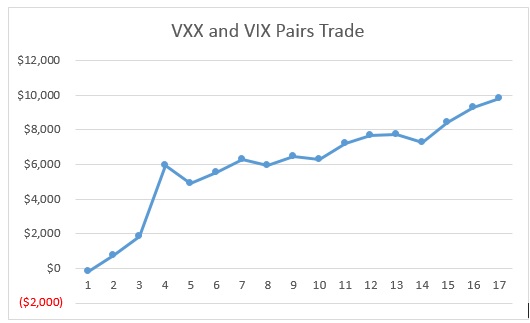

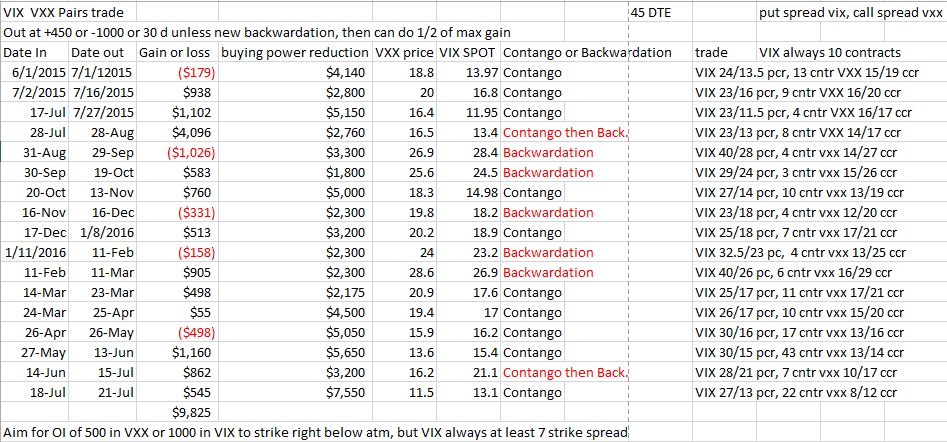

That's right. I was aiming to look at OIs so they would be more liquid. OI of 1000 in VIX and 500 in VXX were my goal OIs but not always achievable in VIX so I set a minimum of 7 strikes ITM for short leg and 1 strike OTM for long leg. This was violated one time in the excel data above so will need to redo to check (one trade had vix at a tighter spread than 7 strikes). when I redo the analysis I will also try to expand the VXX to two strikes more in the money prior to an OI of 500. This strategy has to be replicated in real life to see if the liquity holds up. Edwin- I believe we are on the same page.. Nice! My only caution would be to avoid VIX calendars at all costs... Tastytrade calls this the "death trade" as the losses can greatly exceed the debit paid. For VXX not an issue.

-

Hi Edwin, thanks for the reply. I use a larger spread because it improves the risk/reward for each instrument. The downside is if there are losses due to illiquidity and slippage. Because TOS was not working properly last night I couldn't factor slippage. Real trading will be needed to see if these fill, and I've started trying to do this with 1 contract each. For VXX I used a call credit spread which is neutral to bearish. You're exaxtly right- that such a strategy should be able to help capture some of the contango loss and also the fees charged by the ETN holder. I could buy a put in VXX and a call in VIX but this would lead to losses due to time decay and also lose money in neutral conditions. Selling a spread can be profitable in neutral conditions and has minimal time decay or volatility effects.

-

Possible VIX VXX pairs trade idea Using options -- aim for PUT credit spreads for VIX 45 DTE, with the short ITM leg being at when OI of 1000 or more ideally but minimum of 7 strikes away from ATM, with long leg being 1 strike OTM. For VXX, CALL credit spreads 45 DTE, with the short ITM leg ideally being at when OI at 500 or more, and also long leg 1 strike OTM. Close out when +$450 or lose $1000 or more, or at 30 days. Exception: when in VX futures contango, and this shifts to backwardation, take advantage buy closing out 50%of max gains (which is about $5000 or so). VIX always 10 contracts, make VXX notionally equivalent. ( I wanted to fix the buying power reduction total to $2400 but TOS is fritzing and making all prices NA when I try to change the # of contracts in VIX in think back for some reason... which is beyond frustrating!) I have backtested and am attaching some data, with specific trades if you want to check my work. Not 100% error free but tried to keep the strategy consistent.