Leaderboard

Popular Content

Showing content with the highest reputation since 07/08/26 in Posts

-

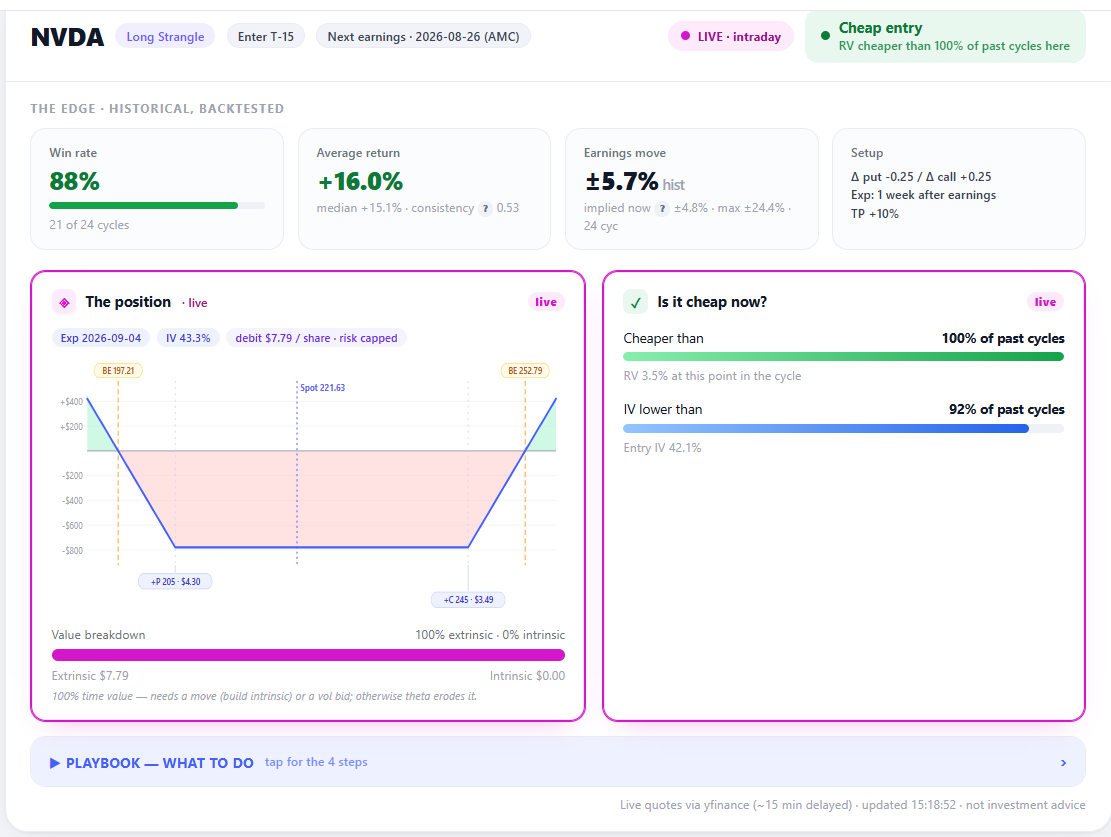

Update — at the open Markets opened, and here's AMD live: the strangle re-priced from $38.69 to $37.79, AMD gapped up to $512, and entry IV eased from ~87% to 84.6%. Marginally cheaper — but the verdict didn't budge: still "Rich entry," still richer than 100% of past cycles, still flagged for crush risk. On the charts, the live-value diamonds sit at the very top of every panel — value, relative value, and IV. Translation: the setup got a little bit cheaper, not cheap. It never dropped into its normal P25–P75 band, so the disciplined read is unchanged. Personnally I would pass, and let the backtest stay a backtest for this cycle. That's the tool doing its job: a 95% historical win rate is only worth having if you don't overpay to get in, from my POV. Romuald - OptionBench

2 points

2 points -

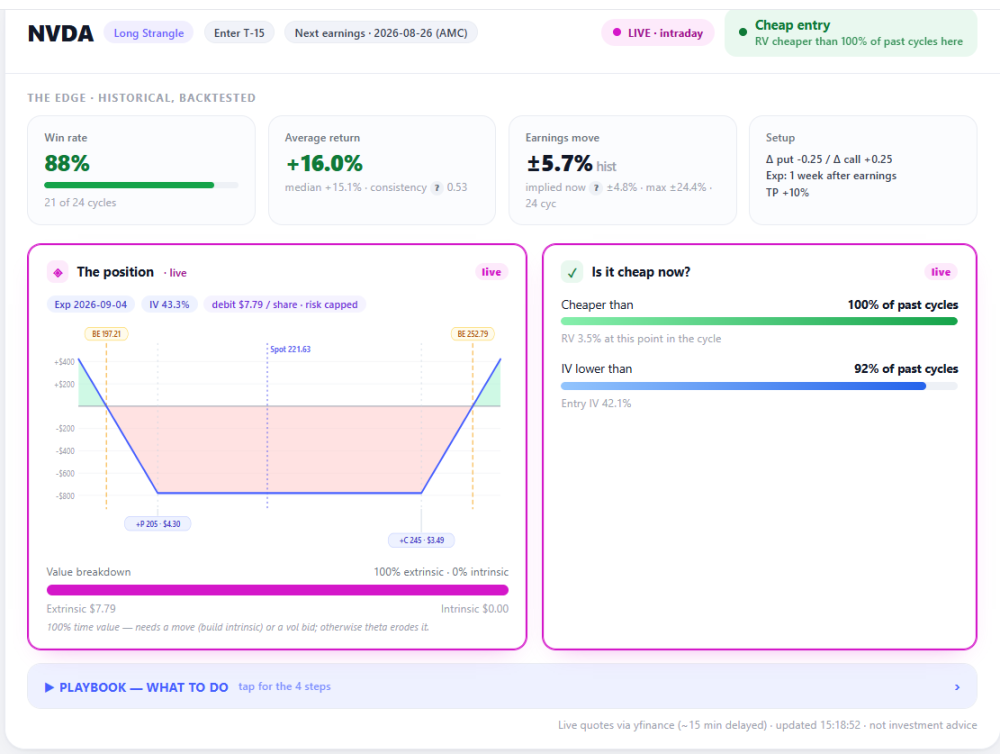

First execution report from a subscriber Canuck Dave traded a pre-earnings strangle off the scanner this week and filled at +18% on the open. That's the first live execution report I've had since launch, and it's worth more to me than any backtest figure I could post — so thanks to him for sharing it, and for letting me quote it. It also taught me something. The setup carries a +10% take-profit, but the position gapped through it overnight, so a limit order filled well above the target. That's a real execution path the backtest doesn't distinguish from an intraday touch, and I'm looking at how to model both properly. The part I want to be careful about. He mentioned going again because the next setup reads "cheap". I'd rather say that the cheapness gauge is not necessarily a green light. It tells you where today's entry sits against past entries at the same point in the cycle. That shifts the odds across many cycles — it does not pick the next one. For example, a cheap entry on a setup with four cycles of history isn't a bargain. An expensive entry on one with twenty well-behaved cycles can still be worth taking. Read it next to cycle count and the earnings-move tile, not on its own. The same applies to the win rate. 88% over 24 cycles means three of them lost, and nothing on the card tells you which three you're about to take. None of that makes the tool less useful. It just means it does something narrower than "find winners" — it tells you what a trade is worth under stated assumptions, and where the numbers disagree with your intuition. That's the whole product. Romuald https://www.optionbench.com/ The blog is now live on optionbench.com. First piece is Expensive Isn't a Veto — about a setup my own entry gauges told me to skip, which then returned 42%, and what I think that actually means. It's the long version of the point above. https://optionbench.com/blog/expensive-isnt-a-veto

1 point

1 point -

Thanks @Romuald for all your work pulling this together. I appreciated the opportunity to be a beta tester and in a small way a contributor to the shipped product. Looking forward to my first annual subscription and many more after that. Dave is1 point

-

Romuald, Sorry to keep sending messages to you. In the "Today's Briefing" page, it would be better (from my perspective), if you move the: "Lower win rate .........Higher win rate" to the top of the "Opportunity Map" Sarang1 point

-

OptionBench is live! The beta is over. Two months, seventeen testers, a lot of pointed feedback and several improvements. Thank you for that. What you get Nine tools, one subscription: • Today — daily opportunity map, ranked by historical edge • Weeks — every entry date from every scanner in one calendar • IV Scanner — where options are unusually rich or cheap versus their own history • Pre-Earnings and Pre-Events ETF — backtested win rates, average returns, and per-cycle dispersion on FOMC, CPI, NFP, ISM, PCE and earnings • Best OS ETF — option structures across 26 liquid ETFs, with the payoff and key figures laid out • Ticker-Options Ideas — pick a ticker, get what currently makes sense on it • Trade Doctor — any multi-leg position, fully diagnosed: POP, expected P&L at implied and realised vol, loss profile, liquidity • Forecast by Options — the probability distribution the market is pricing right now, straight from the chain Pricing $49/month, or $529/year — $44/month if you pay annually. 7-day free trial, cancel any time during it. Discord Every subscription includes the private server. Methodology questions, scanner discussion, bug reports, and a direct line to me. It's also where I post what I'm working on before it ships. And this is the part I mean Tell me what's missing. Every meaningful change over the last two months came from someone here saying "this is confusing" or "why isn't there a…". The intraday timing tool, the expiration fix, the calendar filters — none of that was on my roadmap. Your roadmap is better than mine. https://www.optionbench.com/ Welcome!1 point

-

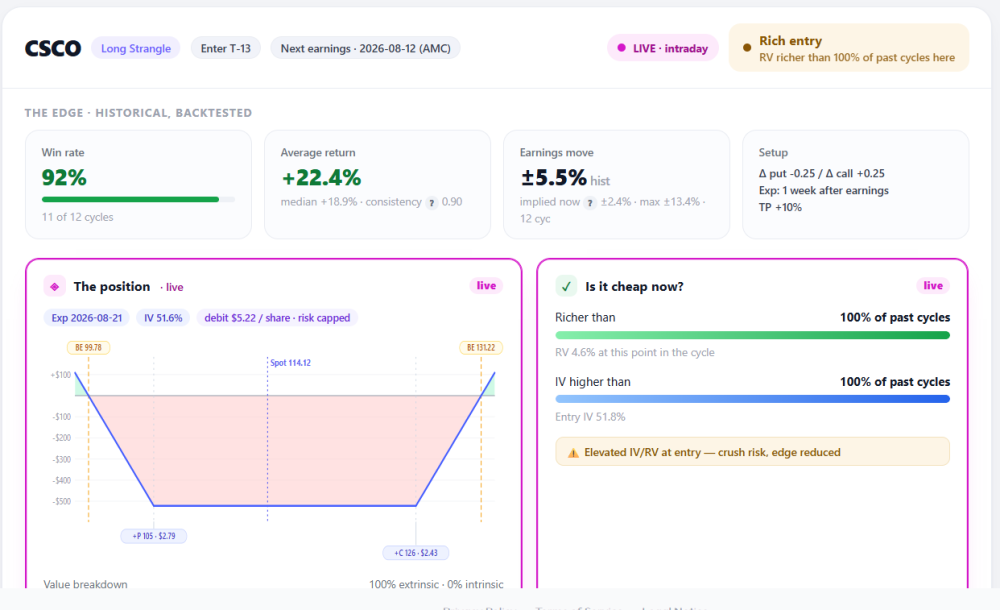

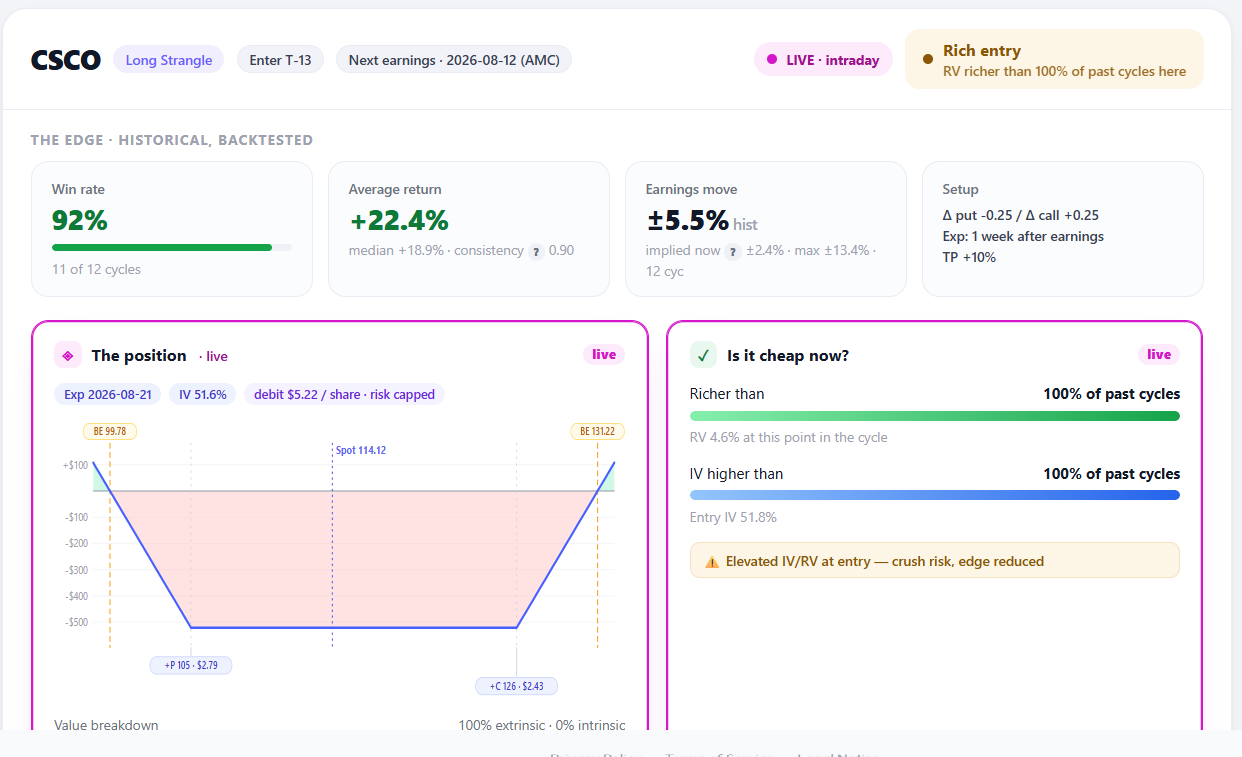

@Romuald looks like we have a similar issue in CSCO ... let's see if it goes "on sale" next week

1 point

1 point -

@Romuald these revisions are a great step forward keep them coming1 point

-

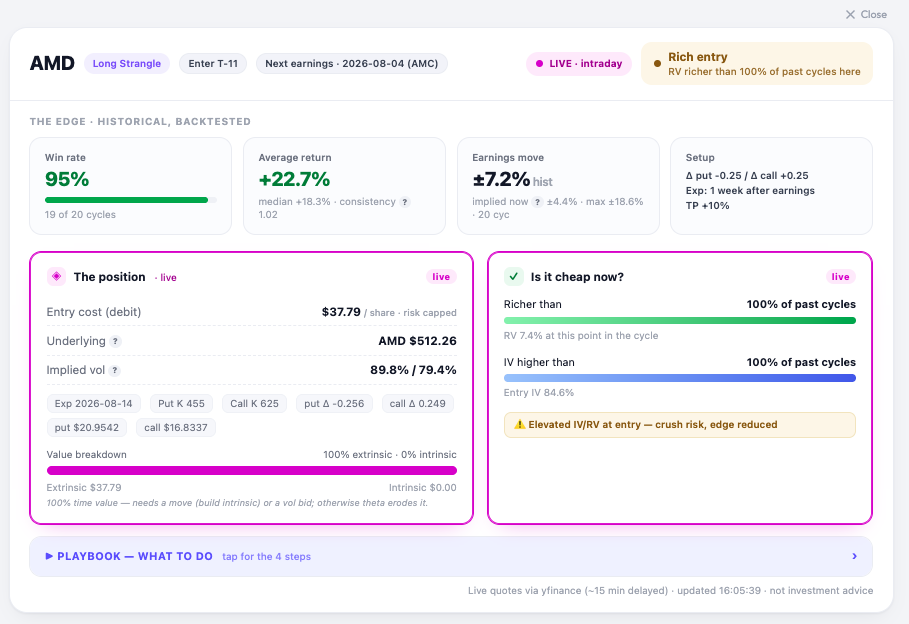

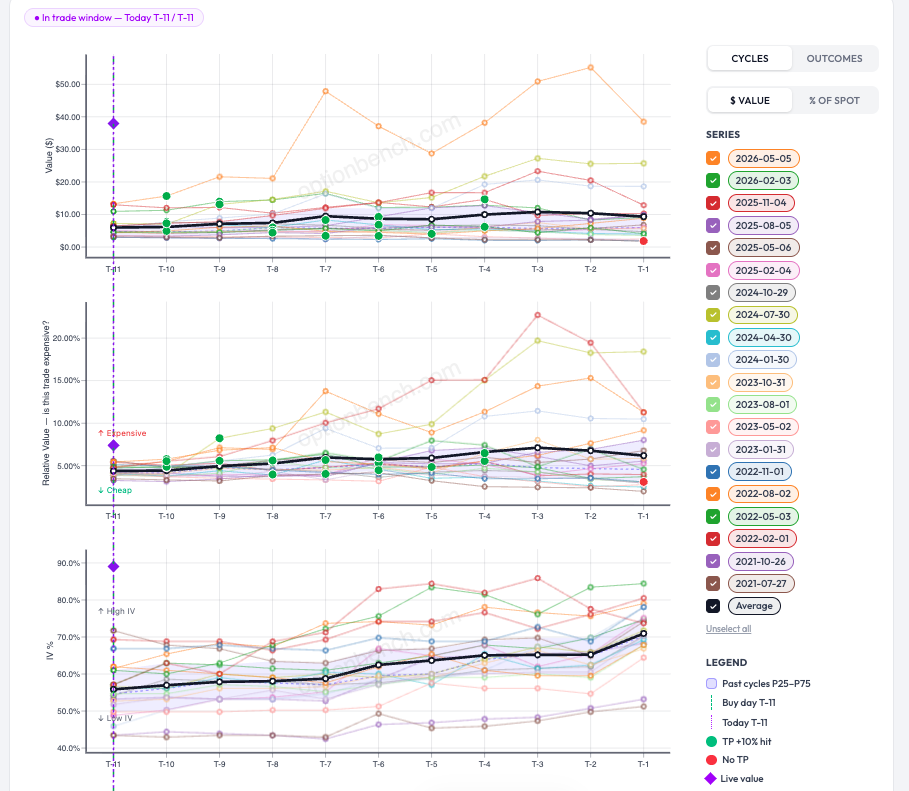

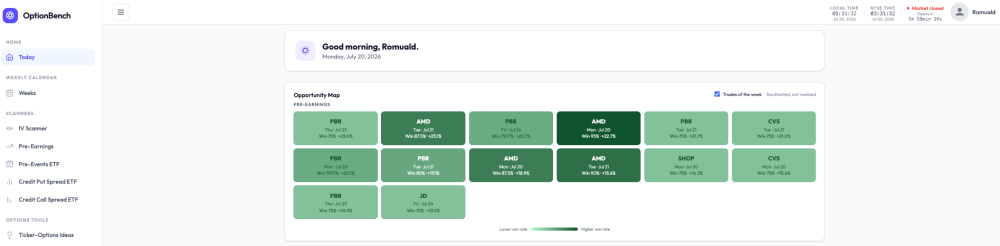

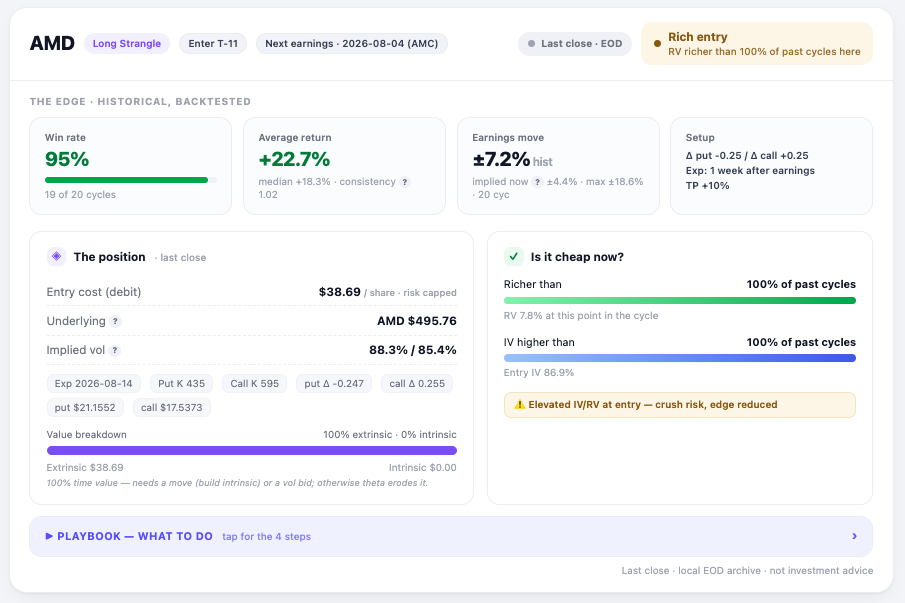

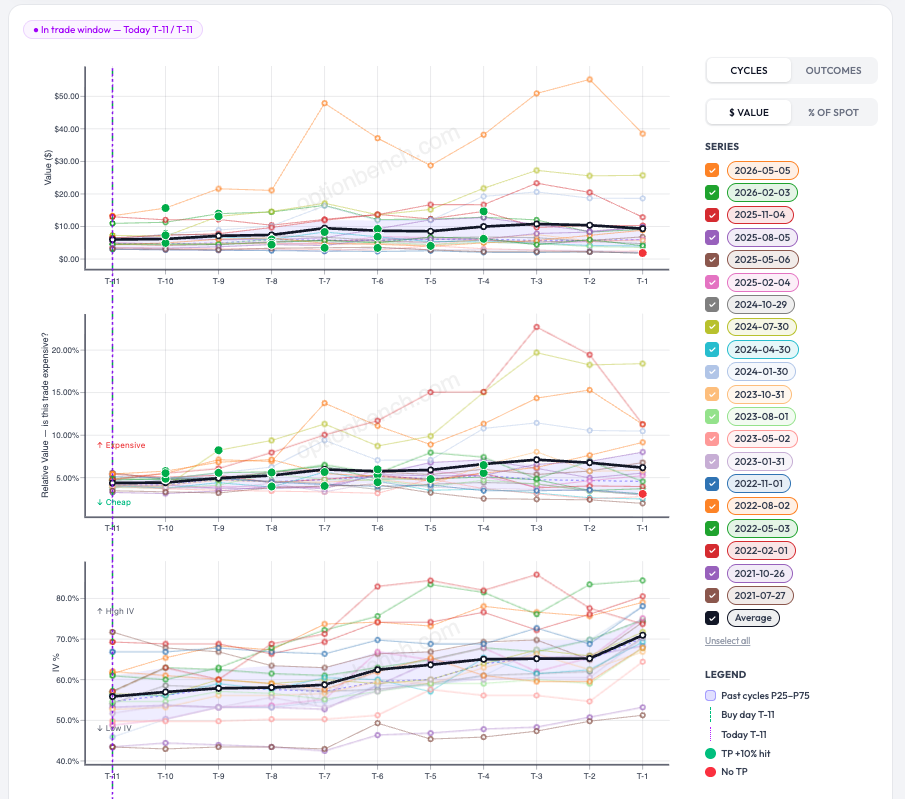

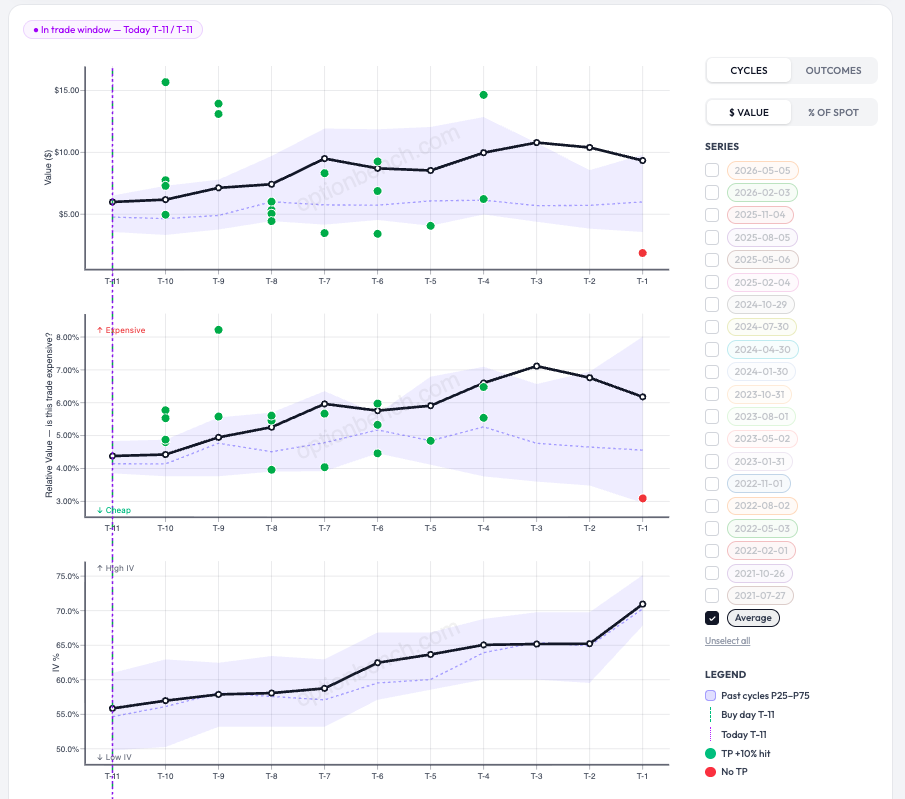

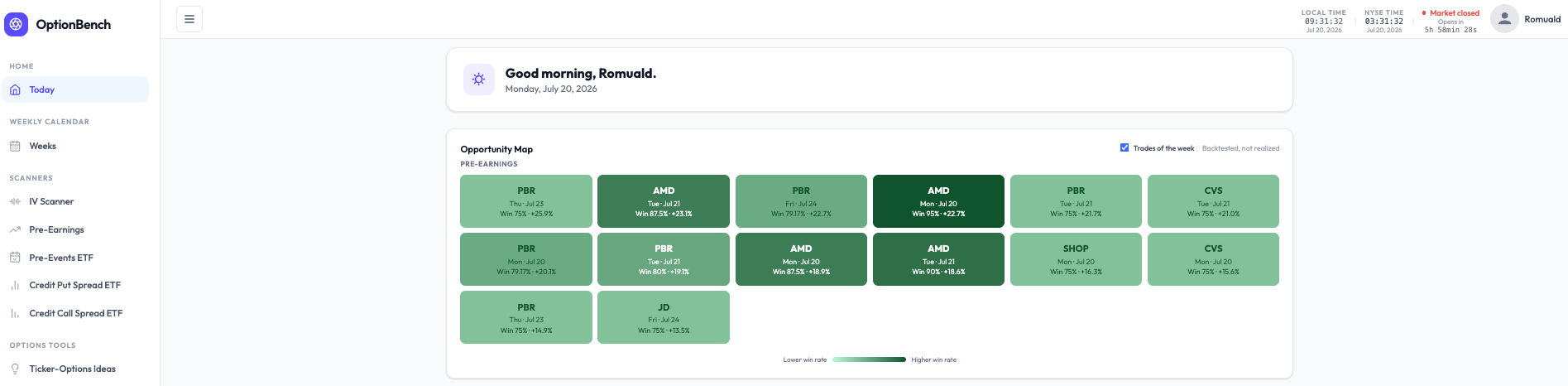

From a Green Tile to a Trade Decision: Inside OptionBench's Pre-Earnings Workflow Most screeners hand you a list. OptionBench hands you a decision — and then argues with you about it. Here's how that works, walking through a real setup on AMD. Start on the map The Today page opens on an Opportunity Map: where you can see one tile per backtested pre-earnings setup for the current week (or week ahead it it is the week-e,d). Each tile carries the ticker, the entry day, and two numbers: historical win rate and average return. The colour encodes the win rate: the darker the green, the more often the setup has worked across past earnings cycles. A "Trades of the week" toggle narrows the grid to the days just ahead, and the caption never lets you forget the key caveat: backtested, not realized. The darkest tile in this view is AMD — Mon, Jul 20 — Win 95% · +22.7%. Tempting. So we click it. One click into the analysis Clicking a tile doesn't dump you at the top of a table, it drops you straight onto that exact row in the scanner, ticker already in focus. For AMD, the setup is a long strangle entered eleven business days before the Aug 4 report and exited the latest about a week after, with a +10% take-profit. The top strip is the historical, backtested edge: a 95% win rate (19 of 20 cycles), a +22.7% average return, a +18.3% median, and a typical earnings move of ±7.2% versus ±4.4% implied today. On the backtest alone, this looks like one of the strongest setups on the board. The part that keeps you honest Here's where OptionBench stops cheerleading. The right-hand verdict reads "Rich entry — RV richer than 100% of past cycles here," and the cheapness panel flags elevated IV/RV at entry — crush risk, edge reduced. In plain terms: the strangle is currently more expensive than at any comparable point in its own history, so buying it now would mean overpaying for volatility, exactly how a great backtest quietly turns into a mediocre fill. One more detail to notice: the badge says "Last close · EOD." Markets are closed right now — it's Monday morning (in France), and the NYSE opens in about six hours — so every live number on the page is the last end-of-day snapshot, not a tradeable quote. The rich-entry read is real, but it's a photograph from Friday's close. The right move isn't to trade it. It's to wait for the open and see whether the morning re-prices the strangle cheaper, or confirms it's still rich. Reading the cycle charts To judge that, we drop into the cycle charts (next Figure). Three stacked panels track the trade from T-11 to T-1 (business days before earnings): the strangle's dollar value, its relative value (RV% — "is this trade expensive?"), and its implied volatility. Every faint line is one past earnings cycle; the bold black line is the average; green dots mark the cycles that hit the +10% target, red dots the ones that didn't. It's a lot to take in at once — so a single click ("unselect all," keep Average) strips it down to the essentials: the average path, the outcome dots, and a shaded band. What the shaded band means That band is the P25–P75 range — the middle 50% of past cycles at each point in the run-up. At every T-x day, we take all the historical cycles and shade from the 25th percentile up to the 75th; the dotted line running through it is the median (P50). Think of it as the setup's normal range. When today's live reading sits inside the band, the trade is priced about as usual; below it, cheaper than history; above it, richer than history. To be continued — at the open So AMD is a beautiful backtest with a currently rich entry, frozen at Friday's close. The interesting moment is only a few hours away: when the market opens, we'll watch whether the strangle cheapens back down into its normal band — and only then decide whether it's worth putting on. That's the whole idea. The map surfaces the opportunity; the analysis tells you whether today is a good day to take it. The discipline is in the gap between the two. See you at the open. Romuald - OptionBench Backtested results are historical and are not realized returns. Nothing here is investment advice. Figures: (1) Today — Opportunity Map · (2) AMD analysis header · (3) Full cycle charts · (4) Simplified view with the P25–P75 band.

1 point

1 point -

@Romuald no rush I'm sure there are other more pressing issues that need your attention ... good luck with the maintenance over the weekend1 point

-

Quick heads-up for anyone using or checking out OptionBench this weekend: app.optionbench.com will be in scheduled maintenance from this Friday 10th of July afternoon (France Time) through the weekend, back to normal Monday. We're doing a planned infrastructure migration on the backend — consolidating the data layer so the scanners run faster and cleaner as we grow. Nothing's broken; we'd just rather take it offline than serve half-migrated data. If you hit a maintenance page over the weekend, that's why — everything will be back Monday. If you were mid-analysis on something and want a hand once we're back up, just ping me and I'll help you pick it back up. Thanks for your patience — doing the plumbing properly now so the tool holds up as more of you come on board. — Romuald, OptionBench.com1 point

-

@Romuald thanks for sharing those thoughts .... I did consider both of them before jumping in .... the richness factor did concern me somewhat and I realize there may be a reduced edge due to that .... I also looked at the other cycles and well not as good as 8 cycles they were all still acceptable in my books as an aside is there anyway to pick more than one strategy in the scanner .. . it would be nice to be able to choose straddles and strangles together as they are closely related ... thanks for the words of thanks it has been a great ride thus far in being able to play a small role in the development of OB

1 point

1 point

This leaderboard is set to New York/GMT-04:00