Leaderboard

Popular Content

Showing content with the highest reputation on 03/09/18 in Posts

-

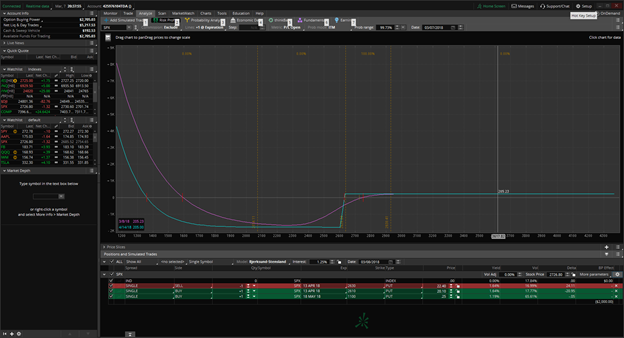

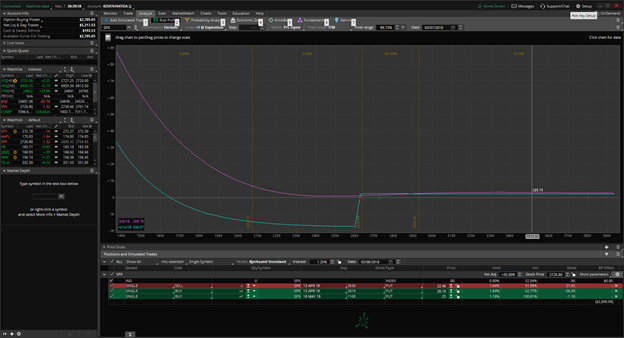

I attended a webinar based on an invite and saw a system of incorporating credit spreads including some protection in case of large moves to the downside. Basically, if there is a spike up in volatility due to a market meltdown, the system may even generate a modest profit or allow for exit with a small loss. The system is designed for the SPX but I will be testing it on SPY for a few weeks to see if I want to jump into SPX with it. Also, for the SPY, I won’t include the downside protection because the exposure will be small in absolute dollar terms and the commissions will be large compared to the cost of the protection. I am assuming everything is SPY will be 1/10 of SPX. Here are the rules: 1. If this is the first trade then determine if the SPX is in an uptrend or downtrend. Nothing fancy, just look at the chart and see. From what I see, the SPX is in an uptrend (There you go, I have called the top 😊). 2. Sell a 20-point credit Spread on SPX (2 point for SPY). Sell put spread for bullish case, call spread for bearish case. 3. Make sure you get at least a credit of 2.20 for SPX. The distance of the short strike will be determined here. Try to maximize it from current price but ensure that you get at least 2.20 credit for a 20-point spread. From empirical observations, it appears that these are about 75-80 deltas or something near there. Do not try to get too much more than this credit as it will move you to a closer strike than the system anticipated. 4. Use options with expiration ideally around 35 days. 5. The profit target is entire credit collected as the spread expires OTM. 6. Stop Loss is when the debit to close the spread has increased to 6.00 (based on bid). That means the loss is 3.80 for the SPX. 7. Place trades every two weeks. If the latest spread is making money then place trade in the same direction. If it is underwater, then place the trade in the opposite direction. If you exited the last trade due to a stop loss then you need to use some judgement. If you believe the market will move up, then sell a put spread, if not, then go with a call spread. 8. For SPX put credit spreads, buy a long Put for 0.20 with 60-75 days to expiration. Basically, this is insurance and will expire worthless most of the times. However, during large spikes downwards, there is Vega inversion and these will help to mitigate the losses as the markets won’t honor the stop loss during those times. According to the webinar presenter, the win rate was around 80%. Thus, expectation is 0.8*(2.2-0.2) – 0.2*3.80 = +0.84. If, I use 0.75 as the win rate, then expectation is +0.55. For options with the deltas mentioned in the rules, a 0.75 win rate appears reasonable. For SPY, sometimes corresponding strikes may not be available. In some cases, the SPY options for the required dates have strikes with 2.50 separation. For practice purposes, I am thinking of locating the short at the SPX or near there and the long will be the nearest strike 2 or 2.5 away. For this example, it will be 257.5/255 instead of 2580/2560 for SPX. The purpose is to get a feel for the market. The transaction costs for the SPY will end up being higher than the SPX any way and can't be traded on a regular basis unless you have a free or a very low commission deal. Maybe someone can back test the system and let me know. My Scottrade account recently got transferred to TDA and now I have access to TOS platform. I am not familiar with it but I was able to simulate the trade and then spiked up the volatility and it showed how the curve moved up with the increase in volatility allowing us to probably close the trade at breakeven or smaller loss in case of those large moves. The screenshots for the PnL for two cases are shown below. The first one is with the volatility at the current level. In the second case, the volatility is bumped up by 35%. You can see that the magenta line moves up the zero line, showing that we may be able to liquidate the spread for a breakeven or maybe for a small loss. For normal down moves, the stop loss can be honored but for the catastrophic down moves, we need this kind of protection. Also, if you have any comments please post here. I am not sure if I can answer all your questions but I am hoping to learn and add another system to our arsenal.

2 points

2 points -

That and volatility is down significantly today across the board. Some of our SO straddles are struggling too.1 point

This leaderboard is set to New York/GMT-04:00