Leaderboard

Popular Content

Showing content with the highest reputation on 08/30/21 in Posts

-

Member of the month award for August goes to @Peeyotch We all appreciate and thank them for their contributions.6 points

-

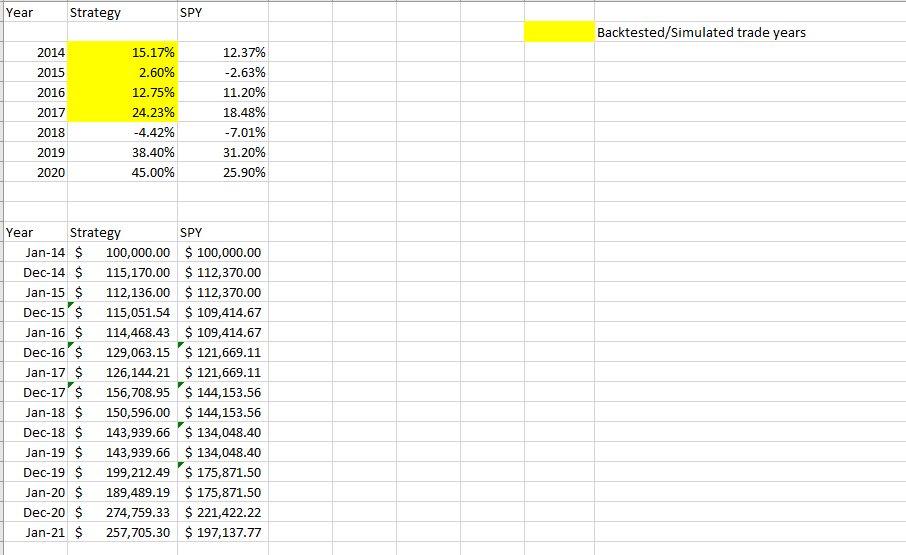

I should make an entire thread on this. The short answer is that it is more efficient than a normal high frequency trading, as we manage for long term capital gains, so higher income tax brackets hopefully won't matter as much. The bad news is that it is not as TAX efficient as long term buy and hold. However, any advisor will tell you managing for taxes is not the worlds smartest move. For example, buying a tax free muni that pays 0.02% vs. buying a just as secure taxable bond paying 5% would be a dumb decision. That said, there are situations where we do "in year" rolls on the calls -- rarely for a profit though, and if it is, then the profit likely won't be large. In-year rolls are almost always after a large market draw down. Due to the frequency of this question when I've been out marketing the new fund, I put together the following spreadsheet (NOTE THIS IS NOT TAX ADVICE, it's merely my theoretical calculations, everyone's tax situation is different). The chart assumes trading Anchor on SPY, which rolls every year vs. just holding SPY, and starting with a balance of $100,000. Every December, the end of year balance was taken in the "Strategy" column, and long term capital gains were applied. Granted this is a rough calculation, as the rolls don't happen on December 31, but it shows what I want it to fairly well. The above is reality, but I have manipulated the series of returns, and here are the general conclusions: 1. If the strategy performs as expected in large up markets, even paying taxes, you're better off; 2. If the strategy performs as expected in large down markets, even paying taxes, you're better off (often significantly); 3. If the strategy performs as expected in flat to smaller down markets, you are probably better off in SPY, but that's because the strategy under performs, NOT because of taxes (in that case, you'll actually have a taxable loss in both situations); 4. In smaller up markets, you are better off in SPY. The Anchor strategy aims for market like returns with less volatility. On a extended period of time that should lead to market outperformance, even including taxes. However if we have a "lost decade" type market, where we see 5-10 years of market returns between 5% and -5% and also low volatility, we most certainly will underperform. Provided of course that carries across everything we're diversified in. If you're looking for a "simple" rule, if both SPY and Anchor returned exactly 10% for five years and then you exited both positions, SPY would be up about 48.8% and Anchor would be up 46.9%. (That's the difference in taking 10% per year and paying your 20% taxes every year and taking 10% per year and paying your 20% taxes at the end). Obviously if you don't EVER sell the position, the difference is more dramatic.

1 point

1 point -

@mimi currently symbols are added half automatic half manual. While I cannot guarantee you will always find all symbols I do try my best. I am conscious that this may not be satisfying, adding a symbol is normally a quick small job after a heads-up via PM or email. WORK and KODK are live (WORK needs one more update run for the current cycle)1 point

This leaderboard is set to New York/GMT-04:00