Leaderboard

Popular Content

Showing content with the highest reputation on 09/10/18 in Posts

-

This topic was a little more active a while back and I had intended to give an update on my results at the 1 year mark, but I've been busy with other projects the last few months. My first CML trade was June 19, 2017, so it has now been almost 15 months and so far I still am only making trades posted on the blogs and by others. Anyway, here's my results to date using CML without actually having a subscription. I think it would be worth the subscription and will likely subscribe soon. Post-earnings Short Put Spread: 50 trades / +13.7% avg Post-earnings iron condors (mix of short and long): 25 trades / -19.4% avg Straddles (mix of pre- and post-earnings): 58 trades / +8.8% avg Pre-earnings Call: 202 trades / +3.0% avg TTM Squeeze: 10 trades / +48.5% avg Other: 10 trades / -36.6% avg --------------------------------------------------- Total Trades: 355 trades / +4.0% per trade avg (The results are not normalized, but I traded the closest I could to the same dollar amount per trade. Even so, some trades were 20% higher or lower than my trade amount, so that has some small effect. I haven't analyzed it to see if the effect helps or hurts the overall numbers versus being normalized)4 points

-

In a portfolio margin account, if you qualify, you will not be penalized for short calendars. PM looks at current risk, not after expiration.2 points

-

This makes perfect sense, because if you have long calendar and a short calendar using the same expirations but different strikes, you also have (another way of looking at it) a debit/credit vertical spread in the front month and a debit/credit vertical spread in the back month.1 point

-

The margin is so beyond insane. The margin you 1- on an outright short option, and 2- you also pay the debit for the (front) long leg. So you are paying individually for both. I did find out, by accident, something interesting regarding this. I have a "regular" calendar in GS, at one strike. Just to see what the margin would be on a "reverse calendar", I setup that trade in GS at another strike, and the margin would be $500, which is not that much different than the debit on a "normal" calendar. But, then I tried the same thing with a stock that I have no position in, and it was crazy..like $4000 or something like that. The point is, if you are holding a regular calendar, at one strike , they will give you a "normal" margin on a reverse calendar on another strike. Just a fluke of margin rules.1 point

-

Yes..that's what I was looking for. I suspect that there might be some "offbeat" brokers who have created a "workaround" to this. But, even if there were, they probably have prohibitive commissions, and would be smaller, less known firms. This has to be the dumbest margin rule out of all of them. The risk is equal whether you do a "normal" calendar, or a reverse one. They create this margin under the "assumption" that the long leg WILL expire first, and you WILL be holding a short, naked option. I know in my case, and probably in the case of any "trader", they would be exiting this trade well before the expiration of any leg. As long as both legs are open, and in place, the position should be margined as such. If/when the day comes when the front leg expires, and you are holding 1 short option, THEN the margin should change to reflect that. This is the way it works with all futures options. So, ES might be a decent workaround for this. After a spike in VIX ( a sharp drop in ES), when the IV on ES has spiked as well, this might be a good time to put on a reverse calendar because you get to sell IV that has spiked, and will also benefit from movement away from the current price, which is much more likely after a sharp drop in SP's.. So you have 2 things working for you, and no margin with ES1 point

-

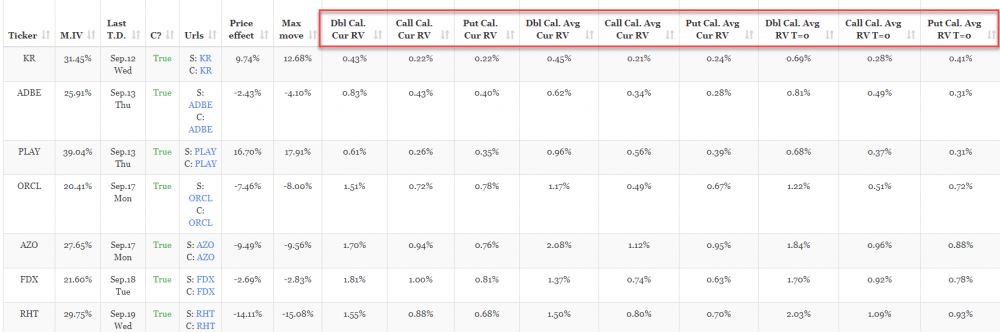

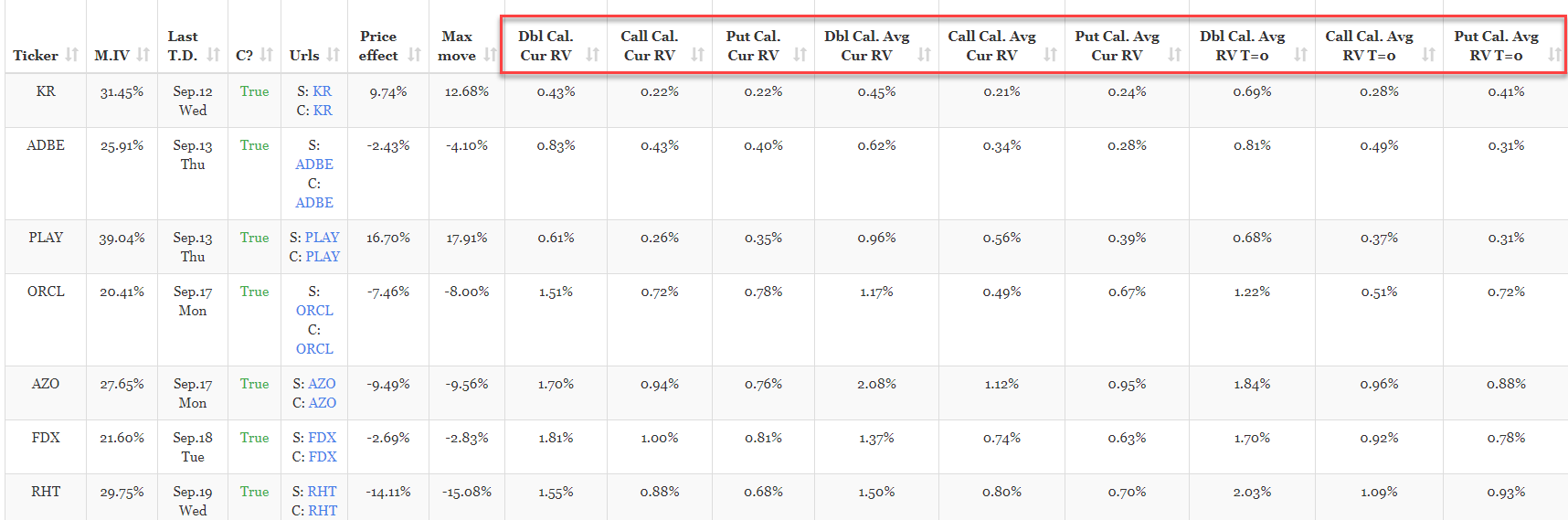

I've done some changes : There are some buttons that allow to show or hide groups of columns. The exports are now grouped under 'Export' I've added new calendar related columns, but it's not tested extensively, and doesn't address all the feedbacks i got, but it's a start. Let me know which additional columns related to calendars you would be interested in. The columns should be sortable now when you click on a column :

1 point

1 point

This leaderboard is set to New York/GMT-04:00